Rather than recommending a specific proposed option, this report offers a combination of both commonly proposed ideas and new ones generated by the Center for American Progress and Generation Progress staff.

It is also worth noting that these options are intended to be one-time solutions that could pair with a larger plan for tackling affordability going forward, such as CAP’s Beyond Tuition. Combining a prospective affordability plan with this relief should cut down on the number of future loan borrowers and lessen the need for subsequent large-scale relief policies.

1. Forgive all federal student loan debt

Under this proposal, the federal government would forgive all outstanding federal student loans. This option would also require waiving taxation of any forgiven amounts.

Estimated cost: $1.5 trillion in cancellation plus an unknown amount of anticipated interest payments, both of which would be adjusted by whether Education Department already expected it to be repaid. For example, a $10,000 loan that the agency did not expect to be repaid at all would not cost $10,000 in forgiven principal. There would also be costs associated with not taxing forgiven amounts, which also must be part of the policy.

Estimated effects: It would eliminate debt for all 43 million federal student loan borrowers.27

Considerations

Does it address equity? Forgiving all debt would get rid of loans for all the populations identified in the equity goal outlined above. That said, by helping every student loan borrower, it will also end up providing relief to some individuals who are otherwise not struggling or constrained by their loans. In other words, while helping eliminate loans for all single parents, it will also provide a windfall for borrowers with higher balances who are having no trouble with repayment.

How simple is it from a borrower standpoint? This policy should be easy to implement for borrowers, since it should not require any opting in or paperwork.

How broad is its impact? This policy would help all 43 million federal student loan borrowers.

Will it feel like relief? Yes—borrowers will not have to make any payments, so they will feel the change.

Who are the greatest beneficiaries? From a dollar standpoint, the highest-balance borrowers have the most to gain from this proposal—especially those who also have higher salaries. They would experience the greatest relief in terms of reduction of monthly payments while also having the wages to otherwise pay back the debt. This is because undergraduate borrowing is capped in law at $31,000 or $57,500, depending on if they are a dependent or independent student, whereas there is no limit on borrowing for graduate school.28 Those who have higher incomes would also feel larger benefits by freeing up more of their earnings to put toward other purposes. Therefore, those with debt from graduate education, especially for high-paying professions such as doctors, lawyers, and business, would significantly benefit. That said, this proposal would help anyone who is particularly worrying about or struggling with their student loans—whether they are in or nearing default. In addition, research suggests loan cancellation would help stimulate national gross domestic product, which has broad-based societal benefits.29

What is the biggest advantage? The policy is universal, and it could be implemented without the need of action on the part of borrowers as long as there are no tax implications for forgiveness.

What is the biggest challenge? This option carries the largest price tag by far. It also would result in forgiving a substantial amount of loan debt of individuals who have the means to repay their debt. This includes borrowers with graduate degrees and potentially high salaries in law, medicine, or business.

How could this option be made more targeted? Limiting forgiveness to only undergraduate loans would help target the plan’s benefits, because there are many graduate students studying in fields linked to high incomes who have no undergraduate loan debt.30 The Education Department unfortunately does not provide a breakdown of the amount of outstanding undergraduate student loan debt; thus, it is not possible to know the cost of this policy tweak.

2. Forgive up to a set dollar amount for all students

This option forgives the lesser of a borrower’s student loan balance or a set dollar amount, such as $10,000, $25,000, $50,000, or some other amount. It would also require waiving any required taxes on the forgiven amounts. Doing so provides a universal benefit that ensures loan debt will be completely wiped away for borrowers who have a balance below the specified level, while those with higher debts also get some relief.

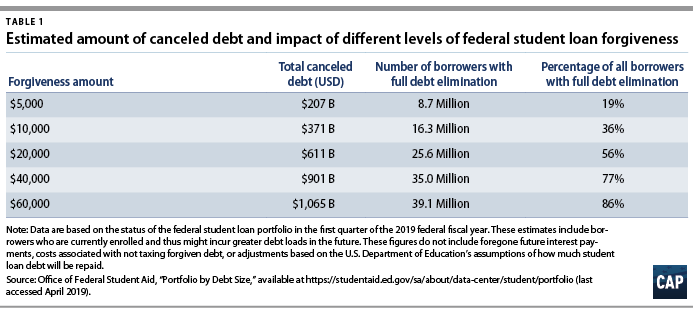

Estimated cost: The total cost varies depending on the dollar level chosen. For example, forgiveness of up to $40,000 for all borrowers would result in canceling $901.2 billion, while forgiveness of up to $10,000 would cancel $370.5 billion. Both cases would also have additional costs in the form of expected future interest payments, but it is not possible to calculate this amount with current Education Department data. These amounts would also be adjusted by the Education Department’s existing expectations around which loans would be repaid. Finally, there would be costs associated with not taxing forgiven amounts.

Estimated effects: Effects vary by dollar amount chosen. Forgiveness of up to $10,000 would eliminate all student loan debt for an estimated 16.3 million borrowers, or 36 percent of all borrowers, and reduce by half balances for another 9.3 million, or 20 percent of all borrowers.31 Forgiveness of up to $40,000 would wipe out debt for 35 million borrowers—about 77 percent of borrowers. The number of borrowers who would have all their debt canceled under this plan might be a bit lower, depending on the dollar amount, because some individuals who currently appear to have low debt levels are in school and are thus likely to end up with higher loan balances as they continue their studies. Table 1 shows the estimated effects and costs across a range of maximum forgiveness amounts.

Considerations

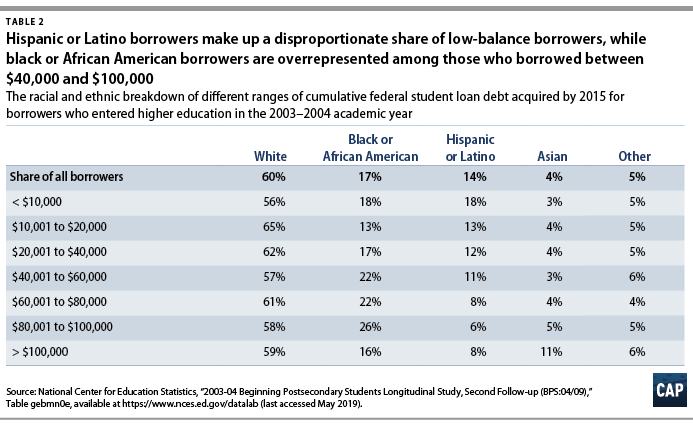

Does it address equity? Yes, though the exact equity implications will vary somewhat based on the level chosen. Table 2 breaks down the percentage of borrowers in a given racial/ethnic category based upon the cumulative amount of federal loans borrowed. Table 3 flips this analysis to show the distribution of debts within a given racial or ethnic category. Both tables are based on borrowers who entered higher education in the 2003-04 academic year and their cumulative federal loan amounts within 12 years. While this is the best picture of longitudinal student loan situations by race and ethnicity, the fact that these figures represent students who first enrolled prior to the Great Recession means it is possible that, were they available, newer numbers might show different results. In considering these tables, it is important to recognize that higher amounts of forgiveness would still provide benefits for everyone at the lower levels of debt as well. That means increasing forgiveness by no means leaves those with lesser balances worse off.

Hispanic or Latino borrowers, for example, will disproportionately benefit from a forgiveness policy that picks a smaller dollar amount, because this group makes up an outsize share of borrowers with $20,000 or less in student debt.32 These same individuals would still benefit from forgiveness at higher dollar amounts, but their concentration among lower-balance borrowers means the marginal benefits of forgiving greater dollar amounts is smaller.

The story is different for black or African American borrowers. They make up a roughly proportional share of low-balance borrowers but a disproportionate share of those who took out between $40,000 and $100,000.33 That means the marginal effect on black or African American borrowers will be greater for higher dollar amounts.

Looking at borrowers based on Pell Grant receipt tells a slightly different story. Individuals who have received a Pell Grant are proportionately represented among lower-balance borrowers and underrepresented among those with the highest balances. But they are most overrepresented among those who took out between $20,000 and $60,000.34

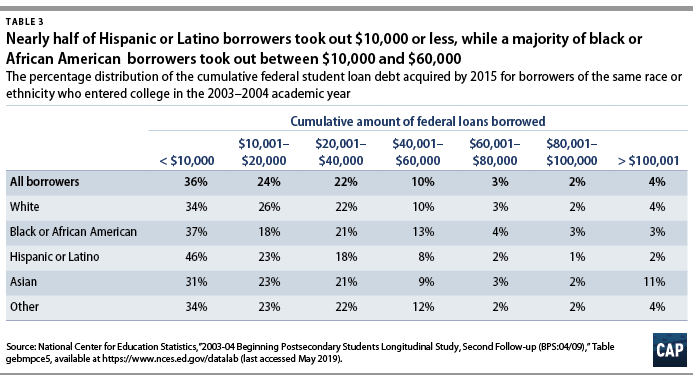

Table 3 presents a different way of considering this issue by showing the distribution of debts within a given racial or ethnic category. For example, though black or African American borrowers make up a disproportionate share of borrowers with balances between $40,000 and $100,000, 77 percent of these individuals had debt balances below this amount. This highlights the importance of considering not just the marginal effects of different forgiveness plans on equity, but also how many individuals within a given group might benefit at varying benefit levels.

Looking at the effects of cancellation only from a distributional standpoint can, however, miss other dimensions of equity that merit consideration. For example, borrowers at the same indebtedness level may be in quite different circumstances. Discrimination in housing and employment, a lack of familial wealth, or other conditions could mean that a borrower who otherwise might seem less in need of assistance would still benefit in a meaningful way that could spur wealth building and address generational asset gaps.

How simple is it from a borrower standpoint? This option is fairly simple and could be implemented administratively with no affirmative work required from borrowers as long as there are no tax consequences for forgiveness.

How broad is its impact? This policy would provide at least partial relief for all federal student loan borrowers.

Will it feel like relief? Yes, borrowers would see a reduction in their balances and payments, though that relief would be proportional to their outstanding balances.

Who are the greatest beneficiaries? At lower dollar amounts, the biggest beneficiaries are smaller-balance borrowers who are more likely to have all their debt wiped away. As the amount of forgiveness rises, those individuals will already have no balance and thus have no additional debt to forgive. This means that those who have the full dollar amount forgiven will increasingly be borrowers with higher balances.

What is the biggest advantage? This is a way to hit a target level of relief that could wipe away debt for those in the greatest distress, while providing a more universal benefit. There may also be benefits for the overall economy, allowing people to purchase homes, save for retirement, and attain the traditional middle-class staples that may be harder for borrowers with student loan debt to obtain.

What is the biggest challenge? Because the benefit is universal, it will end up providing partial relief to a large number of individuals who may not need assistance, unless other elements are added to the policy to target it as described below. Those receiving relief would include individuals with graduate loans working in the areas of finance, law, business, and medicine.

How could this option be more targeted? In addition to varying the dollar amount forgiven, there are a few ways to improve targeting and reduce costs, although these approaches would add some complexity to the overall plan and its administration. One way would be to apply the policy only to undergraduate loans. Another would be to tie the forgiveness amount to a borrower’s earnings so that higher-income individuals receive less forgiveness.

3. Forgive debt held by former Pell recipients

Pell Grant recipients are college students determined by the federal government to be sufficiently low income to qualify for financial help that does not have to be repaid. In the case of students receiving the maximum award, there is an understanding that their family should not be asked to contribute anything for the price of college. As first proposed by Temple University professor Sara Goldrick-Rab in 2015, this option would cancel all student loans held by individuals who previously received a Pell Grant.35 The rationale is that Pell students were never supposed to borrow; loans were for financially better-situated upper- or middle-income students. As a result, the presence of debt among these individuals is a policy failure of the college financing system.

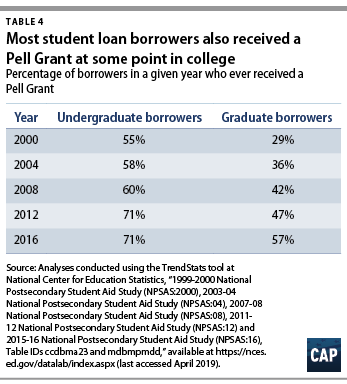

Estimated cost: The Education Department unfortunately does not break down the share of outstanding loan dollars held by Pell Grant recipients. However, these individuals do represent a majority of undergraduate borrowers, as well as of graduate borrowers in recent years.36 There would also be costs associated with not taxing forgiven amounts.

Table 4 shows the share of borrowers in a given year who ever received a Pell Grant, reported separately for graduate and undergraduate borrowers.

These figures suggest that a conservative estimate of loan forgiveness for Pell Grant recipients should be somewhere around half the cost of forgiveness for the full population. In reality, the cost might be a bit lower than half, because Pell recipients’ debt loads tend to be a bit below the debt amounts of those who did not receive the grant. For example, Pell recipients represent 68 percent of all students who entered college in the 2003-04 academic year and borrowed a loan by 2015 but just 43 percent of those who took out loans of at least $100,000.37 Unfortunately, existing data are not good enough to calculate more precise estimates of how much outstanding debt is held by Pell recipients.

Estimated effects: The exact number of students helped is not completely clear, but a look at the number of Pell recipients each year and their borrowing rate suggests it would be millions of students. The number of annual Pell recipients has gone from about 5.3 million in the early 2000s to a high of 9.4 million during the Great Recession. And about 55 to 60 percent of these students borrow.

Considerations

Does it address equity? Yes—Pell recipients are disproportionately concentrated among borrowers with student loan struggles. Nearly 90 percent of students who defaulted on a loan within 12 years of starting college received a Pell Grant. Substantial shares of undergraduate borrowers of color also received Pell Grants, meaning they would be in line for forgiveness. For example, 78 percent of black or African American borrowers in the 2015-16 academic year received a Pell Grant, as did 71 percent of Hispanic or Latino borrowers, 61 percent of Asian borrowers, and 78 percent of American Indian or Alaska natives who borrowed.38

How simple is it from a borrower standpoint? Operationally, the process should be straightforward as long as records still exist that a student received a Pell Grant. There might be some confusion for borrowers who incorrectly think that they are eligible.

How broad is its impact? Though this policy would not affect every borrower, as discussed above, a significant share of student loan holders received a Pell Grant at some point.

Will it feel like relief? Yes, former Pell recipients would no longer have to repay their loans.

Who are the greatest beneficiaries? Students who were lower income while they were in college would benefit greatly from this policy.

What is the biggest advantage? This is an easy way to target relief in a way that uses income to address equity issues.

What is the biggest challenge? Forgiving debt only held by former Pell Grant recipients can create a cliff effect where individuals who just missed the award get no relief. This could include those who might have received a Pell Grant had the maximum award been higher during the years they were enrolled in college. In addition, income alone does not capture generational wealth disparities that may still be present, meaning that there may be individuals who did not qualify for Pell who would otherwise fall in the group of people this policy wants to serve. Finally, some analysts have pointed out that using Pell is not a perfect proxy for income, because it may miss some low-income students and captures some middle-income individuals.39

How could this option be more targeted? Forgiving only undergraduate loans would not necessarily increase the proposal’s targeting, but it would bring down the expense of the option.

4. Reform IDR to tackle interest growth and provide quicker paths to forgiveness

Twelve years ago, Congress created the income-based repayment plan as its answer to unaffordable student loans.40 With the creation of additional plans, there is now a suite of income-driven repayment options available to borrowers. The exact terms vary, but the basic idea is to connect monthly payments to how much money borrowers earn and provide forgiveness after some set period of time in repayment.

Though IDR plans are increasingly popular, there’s also a sense among some policymakers that in their current form, they do not fully provide relief for borrowers. Part of this is due to the complex and clunky program structure. Borrowers must fill out paperwork to get on the plan and then reapply each year. Failure to do so can kick them off the plan, leading to capitalized interest, delayed forgiveness, and a larger balance.41

But IDR’s other major problem relates to accumulating interest. While borrowers can lower their monthly payments on IDR, even paying nothing each month if they are earning little to no income, interest continues to accrue. The result is that borrowers can feel like they are trapped with their loans and with a balance that keeps growing even as they make payments—the only way out being forgiveness that is potentially two decades down the line.

This option would make IDR more attractive by changing the terms so that borrowers no longer have any interest accumulate on their debt. Borrowers would make a monthly payment equal to 10 percent of their discretionary income, even if that would result in repayment taking longer than the 10-year standard repayment plan. Borrowers with no discretionary income would not have to make monthly payments, just as in the past. However, any interest not covered by that payment would be forgiven, ensuring that borrowers’ balances never increase. Undergraduate debts would be forgiven after 15 years, while graduate borrowers would have to wait five years longer—20 years.

Forgiving all interest would be an expansion of some benefits that currently exist. For instance, the federal government covers all unpaid interest on subsidized Stafford loans for the first three years of repayment on most IDR plans.42 And on the Revised Pay As You Earn plan, the federal government also covers half of unpaid interest for the duration of repayment for all loan types. This includes interest on subsidized loans beyond the three-year period.43

Estimated cost: Unfortunately, there are not enough available data to get a sense of the overall cost of this proposal. Costing out the option would require at least knowing more information about the distribution of borrowers using IDR in terms of their income and debts. Currently, the Education Department only provides information on the distribution of debt balances in IDR. Without better data, it is not possible to know what share of borrowers on IDR make payments below the rate at which interest accumulates and would benefit from a greater subsidy. Moreover, the costs of this change are also affected by the amount of subsidized loans a borrower has, because those carry different interest accumulation rules. The net result is that there is no clean way to get an accurate cost estimate.

Estimated effects: There are currently about 7.7 million borrowers using an IDR plan to repay $456 billion.44 It is unfortunately not clear what share of these individuals would benefit from these suggested changes.

Considerations

Does it address equity? Available data are insufficient to fully answer this question, because there is no information on the usage of IDR by the groups described in the equity goal section. However, the answer at least partly depends on what is done to make the plans more attractive for lower-balance borrowers; that group includes nearly half of Hispanic or Latino borrowers as well as large numbers of individuals who have debt but did not finish college and are at significant risk of defaulting. Meanwhile, current IDR plans might be beneficial for black or African American borrowers on paper just by looking at where they are disproportionately represented on an analysis of debt levels. But that presumes payments viewed as affordable through the formula are actually feasible.

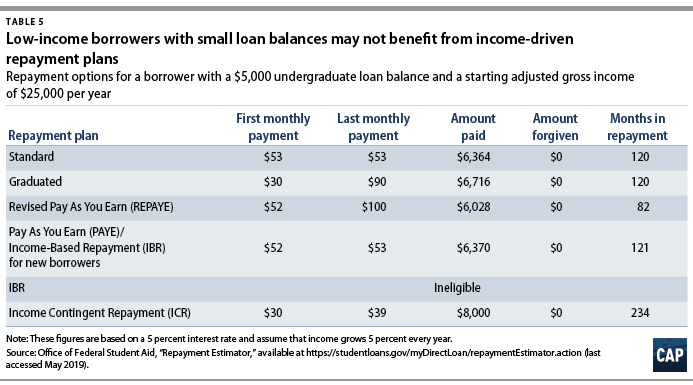

Table 5 illustrates the challenge of making IDR work for borrowers who have a low balance and a low income by showing their repayment plan options. Under the current options for these borrowers, the graduated plan combines the most initial monthly payment relief with the shortest repayment term. Of the four IDR plans, these borrowers are not eligible for one because of their debt and income levels; two plans offer a monthly payment amount that is just a dollar less than the standard plan; and one has the same initial monthly payment as the graduated plan but has them in repayment for almost 20 years.

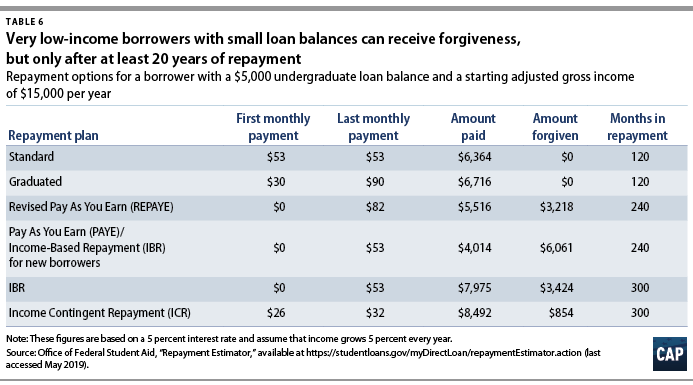

Even if the borrower had a lower income, and therefore a lower monthly IDR payment, the plans would not provide a great deal. (see Table 6) Instead of seeing a decreasing balance, the borrower will instead see it balloon, because she is not able to pay down interest as fast as it is accruing. Forgiving the interest on IDR plans will make the option more attractive, but the requirement of having to wait as long as 20 years to retire a debt that came from a semester or two of school is not going to be an easy sell. This solution also still has technical and gatekeeping issues, as borrowers need to opt in to use IDR plans.

How simple is it from a borrower standpoint? It would be very simple for borrowers who are on IDR. But the paperwork complications of applying for and staying on IDR plans remain a challenge that needs to be addressed.

How broad is the impact? About one-fourth of borrowers in repayment currently use an IDR plan, thus the effect will be somewhat limited unless changes result in increased usage of these plans.45 In particular, this option would need to boost usage among borrowers who owe $20,000 or less. Currently, less than 10 percent of borrowers with debt of $20,000 or less use an IDR plan, compared with 38 percent of those with debts of $60,000 or more.46 Though this slightly understates usage of IDR by low-balance borrowers because some of these individuals are still in school, the fact remains that there are more borrowers with debts greater than $100,000 on IDR than those who owe $10,000 or less.47

Will it feel like relief? Psychologically, yes—borrowers would still be making the same monthly payment, but they would not feel like they are digging themselves into a deeper hole. Borrowers encouraged to enroll in IDR as part of this change would likely see monthly payment relief.

Who are the greatest beneficiaries? The biggest winners are individuals who make payments through IDR but who are not paying down their interest each month. Within that group, the amount of relief will be greater for those with larger debt balances, higher interest rates, or both.

What is the biggest advantage? This solution makes IDR a more viable and attractive long-term plan.

What is the biggest challenge? It may still not be enough to help borrowers with very low balances or who are likely to default, because they still need to navigate the paperwork challenges to sign up for IDR, or the timeline to pay down the debt will still be viewed as too long relative to the amount of time it took to incur the debt. It also presumes 10 percent of discretionary income is affordable, or 150 percent of the poverty level is a large enough income exemption.48

How could this idea be more targeted? Capping the maximum dollar amount of interest that can be forgiven each year would better target the benefits of the option, because it would provide less relief for borrowers with larger loan balances. Reducing forgiveness time frames for lower-balance borrowers or adding opportunities for interim forgiveness—such as $5,000 forgiven after five years on the plan—would especially help lower-balance borrowers and make IDR a more attractive option for them.

5. Provide interim principal forgiveness on IDR

IDR plans guarantee that borrowers have an eventual way out of debt by forgiving any balances remaining after a set number of years. While this is a crucial benefit, taking as long as 20 years or 25 years, depending on the plan, to get forgiveness can make the promise feel abstract and like something that might not happen. This proposal would change forgiveness terms to provide interim principal relief for borrowers. This idea is flexible: For example, all borrowers could receive $2,000 in principal forgiveness for every two years they spend on an IDR plan, or they could get a larger amount forgiven in five-year intervals. The idea is that borrowers would not be in an all-or-nothing situation where they must wait so long to get relief.

Estimated cost: Unfortunately, there are not enough available data to get a sense of the overall cost of this proposal. Costing it would require at least knowing more information about the distribution of borrowers using IDR in terms of their income and debts, as well as how long they have been on IDR.

Looking at the number of borrowers on all IDR plans might provide one way to ballpark the possible cost. For example, by the end of the 2016, 5.6 million borrowers were on an IDR plan. If they were all still on those plans by the end of 2018, it would cost $11.2 billion to forgive $2,000 for each of them.49 If those who were on IDR at the end of 2018 stayed on, the cost of forgiving $2,000 for each of them at the end of 2020 would be $14.4 billion. This assumes that the two-year clock for forgiveness would only start going forward.

Estimated effects: For most borrowers on IDR, small forgiveness would be helpful but not transformative. However, there are about 1 million borrowers on these plans who owe $10,000 or less, meaning they would receive a substantial amount of forgiveness in percentage terms. The more likely effect is that interim forgiveness could make IDR more attractive for lower-balance borrowers who may be discouraged from using it today, because waiting up to 20 years for forgiveness on small amounts of debt may not seem worth it.

Considerations

Does it address equity? There are not enough data to definitively answer this question. However, an interim relief system, if paired with other reforms to accumulating interest on IDR, would make this repayment option much more effective for lower-balance borrowers. This is particularly important for targeting help to individuals who did not finish college or Hispanic or Latino borrowers. Low-balance borrowers currently do not have much incentive to use IDR, because waiting two decades for unloading debt accumulated over a semester or a year does not seem like a good deal. Under this option, those low-balance borrowers could retire their debt much faster, while higher-balance borrowers would keep paying for longer. The data are less clear for other groups on whom policies should focus, such as black or African American borrowers. However, these solutions overall increase the generosity of IDR in a way that should make this option better for anyone who has high levels of debt relative to their income. That, in turn, should help individuals whose earnings do not match the expected return on their debt, such as due to wage discrimination.

How simple is it from a borrower standpoint? There would be some work involved to ensure that borrowers apply for IDR and are making necessary payments. But the relief itself could be handled by the Education Department and student loan servicers.

How broad is the impact? Slightly more than one-quarter of borrowers in repayment currently use an IDR plan, so the effect will be somewhat limited unless interim principal forgiveness encourages increased usage of these plans.50 As discussed in the prior option, it would particularly need to boost usage among lower-balance borrowers.

Will it feel like relief? Yes—providing help at interim periods will show that forgiveness is not an abstract concept years in the future. It will also strengthen support for IDR.

Who are the greatest beneficiaries? Though this policy targets everyone, interim relief will help borrowers with lower balances get rid of their debt faster than those who owe more.

What is the biggest advantage? Interim relief employs a universal benefit to provide more targeted relief to those who owe the least.

What is the biggest challenge? Borrowers would still have to navigate IDR, which can be time consuming and confusing.

How could this idea be more targeted? The tiered relief could be limited to undergraduate loans only.

6. Allow refinancing

This solution entails allowing federal student loan borrowers to get a lower interest rate for the duration of their repayment term. This concept comes from the mortgage market, where refinancing typically pairs a lower interest rate with a longer repayment term. Refinancing proposals for higher education, on the other hand, generally do not include a term extension. This proposal would be most effective when paired with lower caps on interest rates for all future federal student loan borrowers.

Estimated cost: There has not been a public score of a student loan refinancing proposal since 2014, when the Congressional Budget Office estimated one option would cost about $60 billion over a decade to refinance federal loans.51 It is unclear what the cost of such a proposal would be today, and it is also highly affected by the rate offered. If the rate is not too low—around 4 percent or 5 percent, for example—the cost might be a bit lower, at least relative to the amount of volume, because federal changes to student loan interest rates in 2012 led to lower rates for several years. The inclusion or exclusion of graduate and PLUS loans will also have significant cost implications.

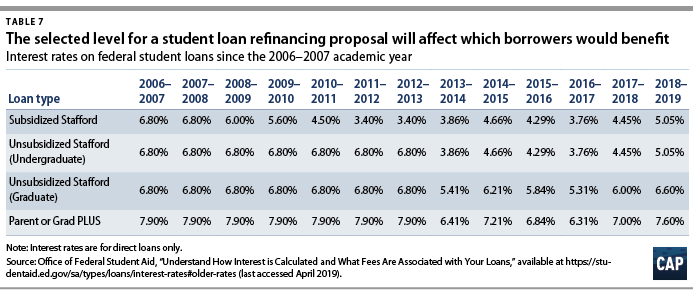

Estimated effects: One way to think about the implications of refinancing is to consider which borrowers currently have student loans with interest rates that would come down under a refinancing opportunity. For example, interest rates for PLUS loans to parents or graduate students have been at 6.31 percent or more every year dating back to at least 2006.52 That means any refinancing opportunity would likely be attractive to the roughly 3.6 million borrowers who have unconsolidated PLUS loans for parents.53 By contrast, if student loans could be refinanced at 5 percent, only some undergraduate borrowers would take advantage; from 2010 to 2018, the interest rate on subsidized loans for undergraduates was below 5 percent, as was the interest rate on unsubsidized loans from 2013 to 2018. 54 Table 7 shows the interest rates on different types of federal student loans since 2006 to show during which years borrowers might have benefited from refinancing at different new interest rates.

The range of interest rates also means the financial benefits of refinancing will vary. For example, a borrower with $30,000 in loans at 6.8 percent saves about $27 a month and $3,245 on a 10-year amortization schedule if their interest rate goes down to 5 percent. By contrast, if a borrower could take out the same amount at a rate of 5.05 percent, they would save just $0.73 a month and $88 over 10 years.

Considerations

Does it address equity? Available data make it hard to answer this question, but there are two ways to consider it. First is whether the problems facing the groups identified in the equity goal above are related to the interest rate on their loans. In some cases, the answer is probably not. For example, borrowers who did not finish college typically have balances below $10,000. That translates into about $115 a month if repaid over 10 years on a 6.8 percent interest rate. Not charging interest at all still leaves a payment of $83, which may be unaffordable for a low-income family and, therefore, may not decrease their odds of defaulting. Similarly, about half of Hispanic or Latino borrowers have low loan balances such that the relief from an interest rate cut is not going to be significant.

The story would be different for other groups. Black or African American borrowers, for example, are overrepresented among borrowers with moderate to high loan balances—between $40,000 and $100,000. At that level, a lower interest rate would provide a greater reduction in monthly payments in dollar terms. The challenge, however, is knowing whether that would be enough to address concerns such as the fact that black or African American borrowers on average make no progress retiring their debts within 12 years of entering college. A lower interest rate and monthly payments could help address that challenge, but if the reason for student loan struggles lies more with external factors, such as employment discrimination, then it may not have a significant effect on improving their outcomes.

How simple is it from a borrower standpoint? It would vary. If the interest rate is at or below the rate paid by all borrowers, it might be possible to automatically change the rates for borrowers. If the new rate is only advantageous for some borrowers, it could end up requiring an opt-in framework. Considering some borrowers have interest rates below 4 percent, any interest rate above that would require opting in.55

How broad is the impact? It depends upon the new interest rate chosen. As noted above, some interest rates will not result in much benefit for undergraduate borrowers. Thus, a new interest rate of 0 percent would affect all borrowers, but one at 5 percent would affect only some cohorts of undergraduate borrowers.

Will it feel like relief? Higher-debt or higher-interest borrowers who are not on IDR will see lower monthly payments. Borrowers on IDR may only notice the change in terms of how much their monthly payment grows if their payments are not covering accumulating interest. The psychological effect of lessening a ballooning total repayment balance is difficult to measure but not negligible.

Who are the greatest beneficiaries? Refinancing makes the biggest difference for borrowers with higher interest rates, larger balances, or both. This is most likely going to be someone who borrowed for graduate school or a parent borrower.

What is the biggest advantage? For borrowers who can largely afford their loans but just need a bit more assistance, refinancing could give them some breathing room. Lower rates may also have some public relations benefit in regard to arguments over whether the government makes money off the loan programs.

What is the biggest challenge? In many ways, this solution duplicates the relief that IDR provides, as both lower the monthly payment. The biggest difference is that refinancing can also reduce the total amount paid over the life of the loan. The trade-off is that IDR offers forgiveness for those who do not pay their loan off before the end of the repayment term but in its current form may increase the total amount paid due to accumulating interest.

How could this idea be more targeted? This option could pair refinancing with a small amount of forgiveness for low-balance borrowers who do not benefit from the policy. For example, if borrowers who owe under $10,000 each got $1,000 in forgiveness, they would likely be better off than they would be under a refinancing system.

Smaller process improvements

The ideas considered in this paper focus on bolder ways to reduce the sting of student debt. But there are smaller changes to the process and structure of repayment that could also help borrowers by making it easier to access benefits or stay on repayment plans. Some of those options are discussed below.

Allow for multiyear certification on IDR

Borrowers currently on IDR have to go through an annual paperwork process to reapply. This is an unnecessary headache for everyone involved. If borrowers are not reapproved in time, they can be kicked off IDR and have unpaid interest capitalized. Servicers, meanwhile, must spend time tracking down and verifying paperwork for borrowers whose payment situation is already addressed. That can take time away from reaching out to more distressed borrowers.

Instead of annual reapplication, borrowers should be able to authorize the IRS to automatically share their updated financial information from their tax returns each year. Doing so would allow payments to automatically adjust and avoid the need for most borrowers to reapply each year.

Automatically enroll delinquent borrowers in IDR

There are significant debates about whether defaulting all borrowers into IDR is a good idea due to concerns about forcing borrowers to pay even if they cannot afford the IDR payment, among other issues. But IDR should be more of an automatic tool for borrowers who are otherwise poised to enter default. That would involve granting the IRS the ability to share financial information on any borrower who is 180 or more days delinquent so their servicer can enroll them in IDR. This would keep borrowers with a $0 payment out of default with no work on their part, while servicers could potentially offer a reduced payment for others.

Authorize temporary verbal sign-up for IDR

One challenge with getting struggling borrowers onto IDR is that those plans are harder to sign up for than other repayment options such as a forbearance. A borrower who simply wants to pause payments on a forbearance can do so by requesting one online or over the phone. Meanwhile, a borrower who wants to use IDR has to complete paperwork and furnish income data, unless they self-certify that they do not have any income. While it is important to tie IDR payments to accurate income information, borrowers should be allowed to verbally provide these data in exchange for a temporary 60-day approval for IDR. Borrowers’ payments would be based upon that amount for two months, giving them time to provide the actual paperwork needed to stay on the plan.

Align wage garnishment with IDR payments

The student loan collections system is already quite punitive in terms of how it can garnish wages, seize tax refunds, or take a portion of Social Security checks. On top of that, the amounts taken from garnishment can also be larger than what a borrower on IDR would pay. For instance, the typical payment on IDR is set at 10 percent of discretionary income. By contrast, wage garnishment can take up to 15 percent of disposable pay.56 The wage garnishment system should become fairer to borrowers by only taking the same share of income as an IDR payment. It should also get access to tax data only to determine the size of a household for calculating this payment amount. Ideally, the system should also consider ways to allow amounts collected through garnishment to count toward forgiveness on IDR.

Allow employers to mass certify PSLF employment

Applying for and staying on Public Service Loan Forgiveness can be a time-consuming process that includes getting paperwork signed by the borrower’s employer. Instead of signing large numbers of individual PSLF forms, employers should have the ability to mass certify eligibility for their employees. For instance, once an employer has to sign a PSLF form for a borrower, they could in subsequent years just send a letter to the servicer listing all the individuals they have certified in the past who are still working at the company. This would reduce the burden on employers, since they would not have to sign individual forms, and also allow for easier processing. Similarly, the federal government could experiment with automatic employment certification of all federal employees who have a student loan.