Introduction and summary

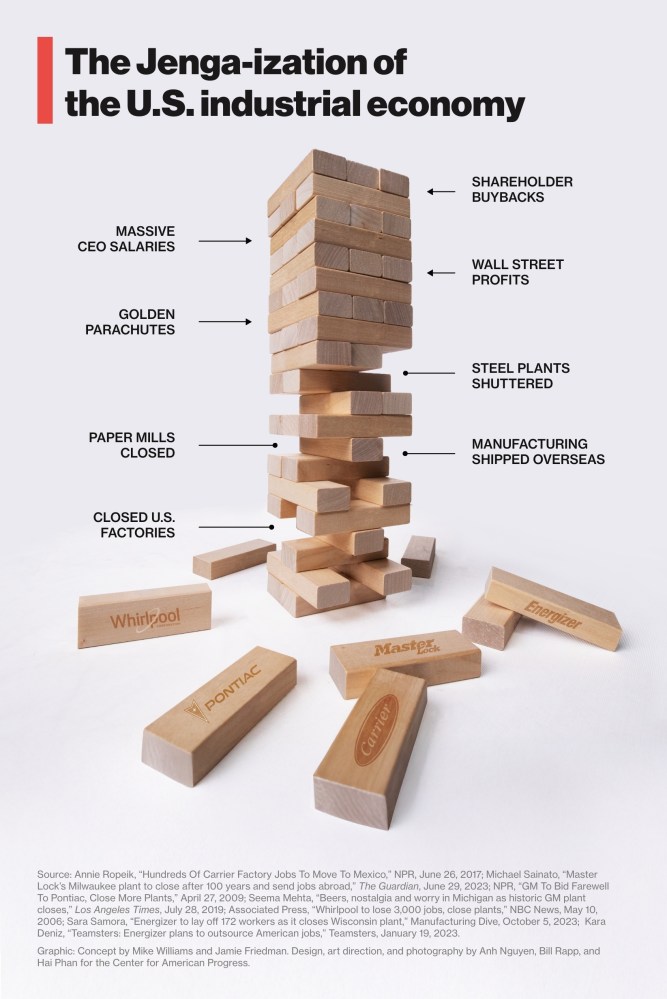

The era of supposed free trade—from the implementation of the North American Free Trade Agreement (NAFTA) to China’s accession to the World Trade Organization and multiple other examples during the late 20th and early 21st centuries—turned the U.S. industrial economy into a game of Jenga. Studs of wealth and opportunity have been ripped out of the middle and the bottom and then stacked on top. As with the game, however, such an arrangement is not only unbalanced; it also all inevitably falls apart. In the past few years, the United States has started to build a more solid foundation with better trade enforcement and the beginning of a concerted industrial policy. But to truly change the game in favor of stable economic growth and shared prosperity, the United States needs a comprehensive industrial strategy focused on domestic manufacturing that puts the United States at the forefront of the global economic transition and leaves American workers better off.

![A Jenga-style block tower that is full and solid on the top half, labeled “massive CEO salaries, shareholder buybacks, and Wall Street profits” and missing many blocks in the lower half, labeled “steel plants shuttered, closed U.S. factories, and manufacturing shipped overseas. Loose blocks scattered below have company logos including Pontiac, Master Lock, and Carrier.]()

That comprehensive strategy must include a robust and consistent research and development apparatus that is coordinated across the federal government and the private sector along with targeted economic planning; expansive public investment in support of both the production and demand of goods; standards to mandate high-quality job creation; and, yes, a muscular trade enforcement regime. Moreover, it should prioritize industries critical to the U.S. economy as well as other key factors such as national defense.

Background

Tariffs are useful but insufficient

Trade enforcement alone cannot stop the Jenga-ization of the economy. Tariffs are necessary to counteract the negative impact of predatory imports and protect nascent industries. In fact, when used strategically and thoughtfully, tariffs can succeed in supporting existing manufacturing. Yet tariffs alone cannot catalyze growth or foster investment at the scale needed to rebuild American industry. That requires tariffs to be used in concert with other tools of economic statecraft, including regulation, procurement, research and development, and—perhaps most importantly—actual investment in U.S. manufacturing.1 Additionally, tariffs can have adverse impacts when used solely as a blunt force instrument, potentially harming workers and disabling key global alliances.

The climate crisis demands sound green industrial policy

The United States now sits in a wobbly economic situation amid the ever-worsening climate crisis, in which heavy industry plays a massive role. Direct CO2 emissions from heavy industry—notably steel, cement, and chemicals—account for roughly 25 percent of emissions globally.2 Steel production is responsible for about 7 percent of greenhouse gas (GHG) emissions globally and 1 percent in the United States.3 Yet the build-out of a clean energy economy—wind turbines, electric vehicles, grid systems—cannot go forward without steel, nor cement or aluminum, for that matter.

As pointed out in an analysis by the Roosevelt Institute, everything is related to climate now4—or at least it should be, if the United States wants to avoid a $38 trillion global price tag from climate change impacts and prevent imposing an additional $500,000 to $1 million over the lifetime of an American child born today.5 The world has recognized the climate crisis, and while action continues to fall short, there is a movement growing toward cleaner industrial processes.6 The future competitiveness of these industries—on which all economies rely—hinges on who can best supply the best clean materials. This is where green industrial policy enters the conversation.

Read more on the climate impact of heavy industry

The United States must prioritize planning and action

The United States needs to identify and wisely prioritize where to dedicate its resources. It should be accepted that it is functionally impossible to build everything within U.S. borders. But it is politically, morally, and economically foolish to think that the United States can do without robust industrial sectors. The solution is to figure out the industries and/or parts of supply chains where the United States wants to have a foothold. The Biden-Harris administration instituted this level of thinking and planning in response to the COVID-19 pandemic. Additionally, the development and passage of the Inflation Reduction Act (IRA), Infrastructure Investment and Jobs Act (IIJA), and the CHIPS and Science Act (CHIPS) resulted from years of planning and analysis on the need for and impact of specific policies and investments. Relying on intermittent actions of good governance is insufficient to drive economic growth that is inclusive and sustainable. The nation needs forward-looking and continual analysis and planning to ensure that its domestic manufacturing base can compete in and lead the current and future clean economy.

The economic necessity for domestic clean steel

The United States should focus next on steel. The world is moving toward a cleaner future, for climate considerations but also because of economics. To start, the U.S. Energy Information Administration projects that the price of coal—the traditional, but dirty, feedstock to steel production—will increase year over year through 2050.7 Moreover, the country has seen growing utilization of the direct reduced iron (DRI) process, a cleaner process that relies on hydrogen and natural gas instead of coal. While this currently makes up a small proportion of total iron made, it is important to consider where DRI usage is on the rise. First, it is being utilized as a climate-conscious strategy by companies and countries across the world, as further detailed below.8 Second, and perhaps most telling, it is the predominant process used where natural gas is cheap and major hydrogen investments are underway—for instance, in the Middle East.9

In a world where coal costs are increasing and investments in natural gas and green hydrogen are growing exponentially, the economic future of steelmaking seems almost foretold.

In a world where coal costs are increasing and investments in natural gas and green hydrogen are growing exponentially, the economic future of steelmaking seems almost foretold. The cleaner the production, the more profitable steel will be.

America’s foundation: The steel industry

The future of the domestic steel industry hangs in the balance of politics, investment, and innovation. For the roughly 131,000 people who work in the industry in dozens of communities across the country, as well as for the builders of cars, buildings, bridges, energy, and water supply systems, the success of the domestic industry is almost existential.10 The world is moving toward cleaner—and eventually decarbonized—iron and steelmaking. The domestic industry received an injection of support from the IRA, which, combined with private investments, has positioned it not only to weather the global transition to decarbonized iron and steelmaking but also, potentially, to thrive.

However, that will not happen without more investment, better trade policies, and direct support for the production of truly clean steel. Much like the United States did with semiconductors in CHIPS or with electric vehicles in the IRA and subsequent trade actions, it should make the steel industry its next frontier of industrial policy.

The reemergence of an American industrial policy

It is important to delineate between industrial policy and industrial decarbonization. The former applies to a method of policymaking that utilizes the public sector to directly support specific industries. The latter is an effort, either through public policy and/or private investment, to eradicate emissions from heavy industry. Work at the federal level has happened on both industrial policy and industrial decarbonization, but they have yet to truly overlap and create synergy. This gap can and should be bridged.

Recent federal actions have stimulated a manufacturing renaissance in the United States

In recent years, industrial policy has focused on semiconductors and key industries in the clean economy—notably, electric vehicles, hydrogen, and industries and their supply chains associated with clean energy production. CHIPS is the clearest example, with dedicated grants going to companies to build semiconductor manufacturing facilities in the United States alongside public investment in research and development and the creation of tax subsidies to support continued production of domestically made semiconductors.11

This has resulted in the United States reemerging in the global supply chain for semiconductors and, most importantly, now having the capacity to at least partially supply itself, so it can avoid another supply chain disaster like the one seen during the COVID-19 pandemic.12 From 2020 to the end of 2023, 80 new semiconductor manufacturing projects were announced in the United States. This led to a tripling of domestic semiconductor production and a massive increase in domestic capital expenditures, with the United States securing more than 28 percent of global capital expenditures, an estimated $646 billion.13 All of this occurred within an industry that had gone from 100 percent market share in the 1970s to a low point of 8 percent recently—and it would have declined even further if not for the passage of CHIPS.14

Now, the United States is set to grow its share of global capacity to 14 percent by 2032 and will see the biggest increase in semiconductor capacity of any region in the world, with a 203 percent increase.15 The policies and investment of CHIPS were successful in directly reviving a domestic industry critical to the future of the global economy. The domestic steel industry is in need of a similar strategy.

Initial investments have begun incentivizing heavy industry to decarbonize

The IIJA and IRA, likewise, have sparked a boom in manufacturing and clean energy through several policies to decarbonize heavy industry. In March 2024, The U.S. Department of Energy’s Office of Clean Energy Demonstrations (OCED) awarded $1.5 billion for six iron and steel decarbonization projects funded by the IRA and IIJA. Together, the projects will avoid 2.5 million metric tons of carbon dioxide emissions annually, which is equivalent to more than 747 wind turbines running for a year or about 4 percent of domestic iron and steel emissions.16

The IRA provided grants to manufacturing facilities to decarbonize, tax incentives to support the production of key goods across the clean tech supply chain, and tax credits to support the consumption of those products. Alongside this, the IIJA’s $1 trillion investment in America’s infrastructure included a significant expansion of “Buy America,” which directed agencies to prioritize domestically produced materials for federally funded projects.17 These policies are already showing a major impact. Manufacturing construction spending is at its highest point in U.S. history, hovering near $240 billion, when it was just $80 billion three years ago.18 New facilities building electric vehicle batteries and solar cells, processing critical minerals, and electrolyzing green hydrogen have taken shape across the country.19 This is already remaking the economy, establishing the United States as a leader in the clean energy global supply chains, and rebuilding a sputtering manufacturing sector. It has created a foundation to ensure lasting U.S. industrial competitiveness for decades.

The Biden-Harris administration also invested significantly in public procurement of building materials that have low embodied carbon emissions and are produced in the United States, and it launched the Federal Buy Clean Initiative in 2021.20 The IRA then provided $4.5 billion to the General Services Administration (GSA), the Environmental Protection Agency, and the Department of Transportation to identify and procure clean construction materials for federally funded construction projects. Combined, these efforts led to the federal government’s first “Buy Clean” standard for low-carbon iron and steel. Several states have also implemented Buy Clean programs, and in 2023, the Biden-Harris administration launched the Federal-State Buy Clean Partnership, in which 13 states committed to prioritize efforts that support the procurement of low-carbon construction materials.21

See more

What is ‘clean steel’?

Traditional iron and steel manufacturing is an extremely emission-intensive process, but there are now several ways to produce iron and make iron into steel without any fossil fuel combustion or greenhouse gas emissions. While definitions of “green” or “clean” steel differ in standards and scope, the basic goal of near-zero-emissions iron and steel production is clear and should shape investment decisions and industrial policy.22

There are several steelmaking methods, the most emissive of which—blast furnace-basic oxygen furnace (BF-BOF)—is also the most widely used globally, accounting for 70 percent of steel worldwide.23 The process relies on metallurgical coal, turned into coke, to turn iron ore into iron in the blast furnace, before turning iron to steel in the basic oxygen furnace.24 Carbon capture has the potential to significantly reduce emissions from the BF-BOF process—up to 50 percent capture for a retrofit and 90 percent capture for new builds. Yet even these efforts alone cannot achieve the deep decarbonization needed to be compatible with still critically important Paris Agreement goals.25

An alternative process, the electric arc furnace (EAF), is both less emission intensive and responsible for most steel production in the United States (70 percent). An EAF can create steel with the feedstock of recycled steel scrap or with direct reduced iron, iron produced from a direct reduction furnace.26 The DRI process usually relies on natural gas but can also use hydrogen. If the DRI process uses green hydrogen—produced via electrolysis using renewable energy sources—and the EAF uses electricity from renewable sources, the raw iron can be made into crude steel without any carbon emissions.27 While this is not the only process with the potential to be labeled truly green steel, the Department of Energy predicts it to be the most effective approach for the United States to reach near-zero GHG emissions by 2050.28

There are also innovative, not yet fully commercialized, processes that can achieve ironmaking entirely without fossil fuels. These include Boston Metal, which directly reduces and melts iron ore with electricity, and Electra, which relies on a chemical process to make emission-free iron.29

Now is the time to decarbonize the steel industry

The steel industry, which supports thousands of jobs across the country, is also core to the identity of many communities in the United States, having supported generations of well-paying union jobs.30 However, too many communities felt the pain of being left behind after companies abandoned union-built towns, fleeing to right-to-work states in order to temporarily crush worker wages, only to still lose out to Chinese industrial overproduction.31

Starting in the 1970s, large American steel companies stopped building new plants in major industrial cities, partially because of foreign competition, and any increase in domestic steel production came from smaller companies building EAFs and DRIs far from metropolitan areas and in the South to minimize the chance of being organized by a union. Additionally, domestic integrated steel producers failed to adopt new and updated technologies.32 As a result, throughout the American “industrial heartland”—the region bordering the Great Lakes that once dominated heavy industry—there was a steep decline in production and manufacturing jobs.33 At the same time, unionization rates in the private sector began to decrease, as a weak labor law regime gave corporations room to prevent union organizing and erode bargaining power.

This should not be attributed to a lack of union interest by workers but rather to a concerted effort from large corporations—including U.S. Steel—in the 1960s and 1970s to influence the weakening of labor laws.34 Then, in the 1990s and 2000s, the introduction of disastrous trade policies along with companies’ single-minded focus on quarterly earnings and shareholder value opened them up to the China shock.35 The results for many cities were hallmarks of deindustrialized communities: increased poverty, increased crime, and loss of public services alongside the basic identity of the community.

Lessons from Buffalo: The decline of Buffalo’s steel industry

Until the late 20th century, Buffalo was a manufacturing center and home to a thriving steelmaking industry.36 The area’s two largest steel plants, Bethlehem Steel and Republic Steel, employed thousands of workers and had a significant impact on Western New York’s economy. At its peak, Bethlehem Steel Corp. employed 70 percent of adults in the Buffalo suburb where the mill was located.37 But by the 1970s and 1980s, as steel mills closed, the Buffalo area saw a dramatic decline in manufacturing jobs, leading to an economic downturn.

Bethlehem Steel, for example, laid off 10,000 workers at once when it started closing operations in 1982.38 Not wanting to pay the high tax rates in New York or spend the millions of dollars on air and pollution abatement that were required, the company instead opened a new facility in Indiana.39 As jobs—many of which were relatively high paying—disappeared, the local economy suffered and the population declined.40 The closure left behind a Superfund site, which will cost the state about $69 million to clean up.41

Now, the United States has a once-in-history opportunity to recreate the U.S. steel industry as a driving force of the domestic clean energy economy, while breaking the antiworker paradigm and giving workers the tools they need to build a future for their communities. Taking on this opportunity will also aid in the fight against another China shock due to overcapacity.42

The shift to cleaner steelmaking—while not moving fast enough—has already begun around the world, and the United States is best suited to lead that transition. Already, the United States is second only to China in EAF capacity but with a higher proportion of EAF to BOF usage (70 percent compared with 14 percent in China).43 The technical solutions to get to net-zero GHG emissions are available and being further developed, but they will require significant investments, smarts, and prompt attention. In steelmaking, the United States has the perfect opportunity to turn domestic investment and innovation into solutions that will work at a global scale and transform the market.

In steelmaking, the United States has the perfect opportunity to turn domestic investment and innovation into solutions that will work at a global scale and transform the market.

In addition to the ticking clock on addressing climate pollution, traditional steel production is harming the health of workers and neighboring communities every day by emitting toxic air pollutants. Steelmaking emits criteria air pollutants such as particulate matter and sulfur dioxide, as well as arsenic, lead, asbestos, and other carcinogens.44 Due to this exposure, steelworkers face higher rates of respiratory illnesses such as asthma, and lung cancer is 500 percent more common among retired iron and steelworkers than it is among other retirees.45 An analysis by the Sierra Club estimates that reducing emissions of particulate matter and its precursors from iron and steel production could avoid nearly 2,000 deaths per year in the United States.46 And the impacts are not spread equitably, as nearly all steel and coke plants in the United States are located in communities that are low income, have high unemployment rates, and have lower education levels than the national average.47

While clean steel is not currently cheaper or more competitive than traditionally made steel, the day that flips is fast approaching. Due to growing demand from buyers, evolving trade dynamics, and expanded investments, policies, and mandates from governments around the world, the pivot to clean steel has already begun:

- Sweden has led the charge with its major federal investment in HYBRIT—a joint effort from SSAB, LKAB, and Vattenfall to produce fossil-free steel—and through the growing private sector investment in Swedish company Stegra (formerly H2 Green Steel).48

- Canada is investing heavily, as ArcelorMittal is transforming its blast furnace steelmaking in Hamilton into a DRI-EAF production process by 2028.49

- Namibia is launching Africa’s foray into green iron, as it broke ground on a fully decarbonized ironmaking facility at the end of 2023.50

- Australia is making moves to be the world’s major green iron producer.51

- Even China may be making major changes to its massive steelmaking industry, as new steelmaking capacity halted for much of 2024 and a pivot to EAFs and low-carbon iron may be underway.52

Perhaps most poignantly for domestic steelmakers, the costs for making cleaner and eventually green steel are closely associated with the costs of producing natural gas currently and green hydrogen in the near-term future. Notably, these costs are projected to fall to effectively eliminate a green premium in many countries, including the United States.53

Right now, the United States’ domestic steel industry has a moment where it can either emerge as a leader in the global competition to be a clean steel producer or risk getting passed by and sacrificing not only future competitive advantage but also its existing market share. Research from RMI shows that the United States is well positioned to be a major producer of green iron, but achieving this will require a significant near-term investment that includes direct subsidies for domestic green ironmaking.54 However, this change is so massive it cannot be done with just private investment; it must involve a comprehensive slate of public policies—including direct investment, trade policies, and market supports.

Recommendations: A green industrial policy package for the steel industry

As described above, a comprehensive industrial policy should include planning, research and development, direct investment, job quality standards, and trade enforcement. Many of the recommendations listed below are included in Rep. Ro Khanna’s (D-CA) Modern Steel Act.55 Additionally, the United States has the potential benefit of learning from an allied nation—Sweden—as it embarks on a version of steel decarbonization through industrial policy.56

A future green industrial policy package should build on those efforts by taking the following steps.

Planning, research, and development

- Establish an Office of Critical Industries within the White House, supporting the Made in America Office that was established by the Infrastructure Investment and Jobs Act:

- The charge of this office would be to harness the capabilities of the federal government to analyze current economic needs and capacity and examine future trends to then offer recommendations on how to support key existing industries and to gain a foothold in new and budding ones. The office should begin its focus on a few select industries—steel, semiconductors, artificial intelligence, and electric vehicles—but also be supported to look beyond those first few.

- The office can and should utilize the Defense Production Act’s authorities to obtain information in order to produce reports critical to the nation’s defense. This legal authority would compel firms to share necessary information with the federal government to inform these reports.

- Develop a definition of “clean steel.” The development of a common definition of clean steel would be a significant driver of better policymaking, allowing for clear standards to be made and setting a direction for the market. The federal government, through a collaborative process led by the Department of Energy, should define clean steel to mean that the direct emissions in the production process—not counting upstream emissions indirectly caused by hydrogen or electricity production—are at or near zero. The definition should be applied separately to iron and steel, ensuring proper accounting for the upstream emissions from inputs. Utilization of the definition in standard-making should incorporate a sliding scale, as described by Responsible Steel, to ensure that the United States steadily works to decarbonize all its steelmaking capacity without causing the closure of plants.57

- Utilize the Defense Production Act’s authority to establish voluntary agreements to explore and create public-private collaborations for key emerging sectors, as thoughtfully described by Evergreen Collaborative.58

- Expand the research and development budget. The federal government provides support for innovative technologies in manufacturing, notably through the work of the Department of Energy’s Advanced Materials and Manufacturing Technologies Office and Industrial Efficiency and Decarbonization Office. But this number should be increased from the roughly $500 million fiscal year 2025 request. Additionally, the Office of Clean Energy Demonstrations’ appropriations should be increased beyond its $180 million FY 2025 request, and the Office of Manufacturing and Energy Supply Chains should be increased beyond its $113 million request to ensure that deployment of the federal government’s innovative research keeps pace.59

Public investments

- Expand the Industrial Demonstrations Program to provide grants to deploy multiple 100 percent clean steel plants and 100 percent clean iron plants built in legacy communities with unions.

- Cover the “green premium” by creating a tax structure to support the production of clean iron and steel and to spur demand for the products. Under the Inflation Reduction Act, a tax credit was created to offer subsidies for the production of goods core to the build-out of a clean economy. The so-called 45X credit provides a production tax credit (PTC) for the building of such materials as solar panels and electric vehicle batteries and subsequent components.60 This concept can and should be extended to the production of clean iron and steel. To do so would entail:

- An investment tax credit (ITC) for new or rebuilt iron and steel facilities that are all electric or all hydrogen ready.

- A PTC for up to $100 per ton of union-made, domestic, all-electric, or all-hydrogen clean iron.

- A PTC for $100 per ton of union-made, domestic, all-electric, or all-hydrogen clean steel.

- Both PTCs to increase if the electricity or hydrogen involved is 100 percent zero emission.

- The ITCs for newly and reconstructed facilities to phase out after the sector first reaches 80 percent clean.

- The PTCs to phase out after the sector reaches 100 percent clean.

Standards and mandates

- Utilize the expanded nature of Buy America, as passed in the IIJA, and associate it with the green steel market supported by these policies.61 Specifically, such policy must require infrastructure projects funded with federal dollars to eventually prioritize buying domestically produced 100 percent clean steel, following Buy America rules for waivers related to cost and availability. This would ensure that all new clean iron and steel has a guaranteed market.

- Develop and initiate Buy Clean standards for steel, utilizing a sliding scale to ensure appropriate timing and application to the industry as it incorporates decarbonization investments.

- Attach high-quality job standards to all investments, notably by mandating that any company that receives funding sign a community benefits agreement that includes:

- A project labor agreement for the construction of any new or significantly renovated facilities.

- A neutrality agreement on organizing and a commitment to reaching a collective bargaining agreement in the case of a successful organizing drive with the ongoing production and maintenance workers.

- Provisions to support the hiring of people local to the community.

- Monitoring of harmful pollution and assurances that local environmental impact will be minimized and, preferably, eliminated.

Trade enforcement and multilateral collaboratives

- Establish a multipronged tariff-based trade enforcement regime focused on eradicating carbon-intensive imports of steel or iron, which would:

- Initiate a carbon border adjustment mechanism (CBAM) to impose tariffs—which would never phase out—on the import of any steel or iron that is not 100 percent clean, ratcheting the level of the tariff up over time to become coercive. The implementation of a CBAM should not deter existing Section 232 tariffs on steel and iron, and if a CBAM is not an option, then an alternative that should be considered is to incorporate embodied carbon into existing 232 tariffs on steel and aluminum.

- Extend the reach of tariffs on steel-heavy goods, such as electric vehicles, to also focus on the carbon intensity of the steel within the goods.62

- Utilize revenues to help pay for the major investments listed above.63

- Utilize diplomatic engagement to enter into multilateral collaboratives on carbon-based trade enforcement and harmonized green procurement standards. This could be done by: 1) entering into sectoral-based tariff coordination, similar to the proposed Global Arrangement on Sustainable Steel and Aluminum, with like-minded nations to harmonize carbon-based tariffs and collectively eradicate dumping by nonmarket economies;64 and 2) coordinating on Buy Clean-like policies with like-minded nations through multilateral mechanisms such as the Industrial Deep Decarbonization Initiative, where governments can center harmonization efforts on definitions, standards, transparency, and requirements.65

Read more

Conclusion

The success of the Biden-Harris administration’s industrial policy provides clear evidence to keep using this method of policymaking and to identify and implement it for the next industries the nation deems critical to the economy, culture, and politics. It is, in effect, rebuilding the tower, but this time without the wobbliness of Jenga, establishing a broader foundation with fewer holes. The steel industry is perhaps the quintessential choice for the next big industrial policy, but given the climate crisis, direct source pollution, and fast-approaching heavy competition, it only makes sense if the investments point toward a domestic decarbonized steel future.

Acknowledgments

The author would like to thank Trevor Higgins, Shannon Baker-Branstetter, Ryan Mulholland, and Jasia Smith of the Center for American Progress; Yong Kwon of Sierra Club; Hilary Lewis of Industrious Labs; and Anna Fendley of the United Steelworkers for their review of and input on this report. The views expressed in this report are solely attributable to the authors.