This past December, stock market volatility and the Federal Reserve’s controversial move to slow the economy dominated U.S. economic news. As we enter a new year, it’s worth taking stock of multiple facets of the economy in wrapping up 2018 analyses. There is currently considerable uncertainty about the state of the economy, and it comes in two very different varieties.

Economic news coverage in 2018 focused on financial markets signaling some justifiable concern that the Federal Reserve risks slowing the economy to the point of possible recession as it attempts to balance the economy in the wake of the 2017 tax cuts—a proposition with significant downside risk. There is also uncertainty in regard to the labor market, mostly because while the economy continued to add jobs at a healthy clip in 2018, there is little consensus on how much longer it can keep adding jobs and growing wages without triggering higher inflation rates.

The U.S. Bureau of Labor Statistics will release its monthly report with December’s jobs numbers on Friday; this will be the last labor market report for 2018. Although the year saw some indication of economic recovery since the Great Recession—including historically low unemployment rates, continuations of job growth, and growth in gross domestic product (GDP)—other indicators suggest that there remains much to improve on and strive for in 2019.

2018 saw further decreases in unemployment, but wealth gaps remain

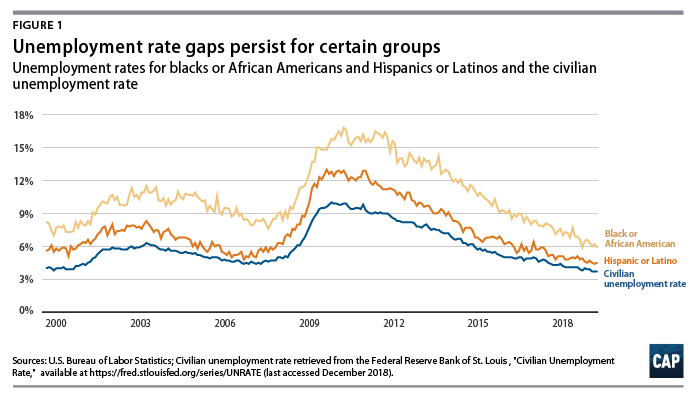

From the beginning of the year through November 2018, the unemployment rate fell 0.4 percentage points to a rate of 3.7 percent. This is the lowest overall unemployment rate in nearly 50 years and continues the steady trend of decline observed since 2009. (see Figure 1) The employment rate has also continued to inch up to almost pre-recession levels, with workers continuing to move from the sidelines into jobs at higher numbers than some predicted for yet another year.

Yet despite a more attractive labor market for some workers, unemployment rates remain disproportionately high for certain groups, particularly black and African American and Hispanic/Latinx people, who face other hurdles in the economy such as prominent wealth gaps. These gaps exist despite the fact that overall, these communities are seeing similar levels of educational attainment and are working more than their white counterparts. Moreover, although some people may have an easier time finding a job than in previous years, wider economic pressures have sparked reason for worry.

Emergency expenses, stagnant wages, and the need for economic security

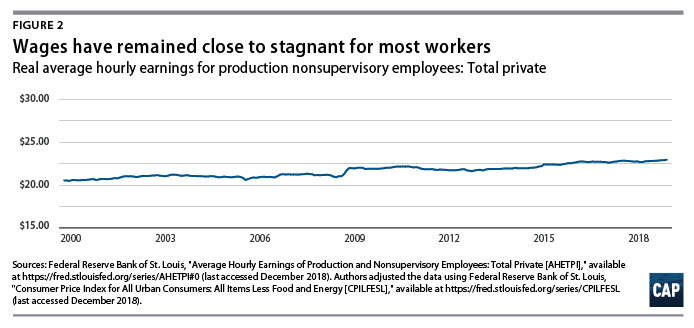

Despite possibility of last-minute spending, 40 percent of Americans are unable to cover a $400 emergency expense, while wages remain close to stagnant for most people, despite gains for top earners. New analysis from the Economic Policy Institute shows that labor income for the bottom 90 percent has shrunk by more than 10 percent since 1979—translating to about $10,800 of lost pay per household. With little sign of bipartisan cooperation on pro-worker policies, a tight labor market is the primary force that most workers can expect to reverse this trend in the coming year.

Meanwhile, wages for production and nonsupervisory workers have remained virtually stagnant for decades, increasing just $2.41 since the beginning of 2000. (see Figure 2) All the while, costs of living—including child care and education, just to name a few—have continued to rise, outpacing wage growth for most Americans.

On top of these things, a major scientific report made headlines last month. The report outlines the imminent threats of climate change for communities across the globe. The report found that unless significant steps are taken to address climate change, damage could affect as much as 10 percent of the U.S. economy. The need and opportunity for infrastructure investment is considerable, and it underscores the harmful effects of austerity over the past decade, when low interest rates would have lowered costs of inevitable investments. As shown by the flooding that U.S. communities experienced just this past year, direct impacts of climate change have already begun to amplify environmental injustices. And they will continue to impact communities across the nation for years to come. The U.S. policy response to climate change must address Americans’ great need for economic security, especially for those who face the greatest challenges in the labor market and those disproportionately hurt by climate injustices.

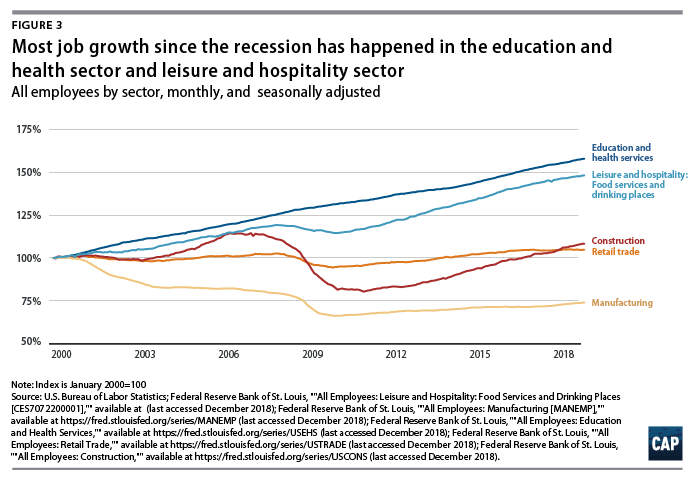

Broader economic trends that put pressure on American workers, in conjunction with the disconcerting priorities of the Trump administration, hurt working families. They also put into focus the need to highlight the true conditions and lived experiences of people across the economy. Job growth has been uneven across all sectors of employment since the Great Recession, with many only now returning to their pre-recession employment levels. A closer look at the sectors that have seen the largest growth since the recession shows that the food service and health care sectors have seen the most job growth.

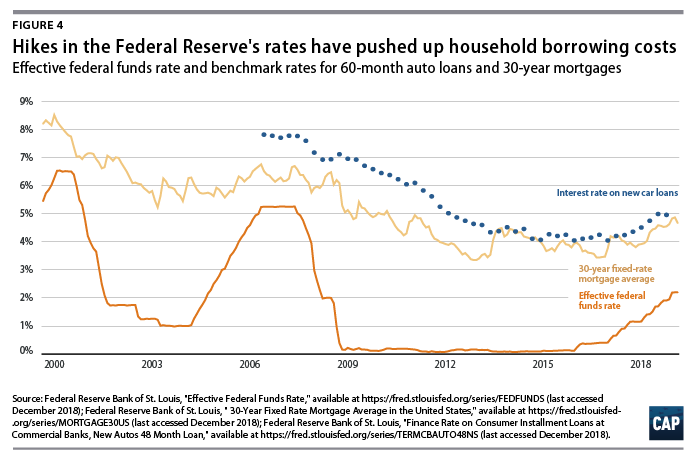

Although overall inflation has remained moderate, the sectors where costs have grown rapidly are largely those where the Fed’s decision to raise interest rates is making big-ticket purchases less affordable. Since the Fed started hiking rates two years ago, monthly payments on mortgages and car loans have increased considerably, putting pressure on households, homebuilders, and the automobile industry.

Conclusion

Despite overall low unemployment rates and a continuation of high GDP growth, the reality behind wages, as well as the disproportionate hurdles that certain groups face in the labor market, suggest that workers may not be seeing the gains and opportunities of an economy that at first glance seems to be booming when perusing headlines. There is still room for the economy to grow—and when considering economic priorities for 2019, it is essential that analysts and policymakers take a variety of indicators into account, instead of overstating the economic prosperity of the past few years.

Daniella Zessoules is a special assistant for Economic Policy at the Center for American Progress. Michael Madowitz is an economist at the Center.