Introduction and summary

Health care is a right: No American should be left to suffer without the health care they need. The United States is alone among developed countries in not guaranteeing universal health coverage.

Over the past half century, there have been several expansions of health coverage in the United States; today, it is past time to ensure that all Americans have coverage they can rely on at all times.

The most recent coverage expansion, the Affordable Care Act (ACA), was an historic accomplishment, expanding coverage to 20 million Americans—the largest expansion in 50 years.1 The law has also proved to be remarkably resilient: Despite repeated acts of overt sabotage by the Trump administration—and repeated attempts to repeal the law—enrollment has remained steady.2

Medicare Extra for All would guarantee universal coverage and eliminate underinsurance.

In the near term, there is an urgent need to resist sabotage and efforts to undermine Medicaid, to push for stabilization to mitigate coverage losses and premium increases, and to expand coverage through Medicaid expansion in all states that have not already done so. At the same time, it is imperative to chart a path forward for the long-term future of the nation’s health care system.

Costs and deductibles remain much too high: 28 percent of nonelderly adults, or 41 million Americans, remain underinsured, which means that out-of-pocket costs exceed 10 percent of income.3 In the wealthiest nation on earth, 28.8 million individuals remain uninsured.4

To address these challenges, the Center for American Progress proposes a new system—“Medicare Extra for All.” Medicare Extra would include important enhancements to the current Medicare program: an out-of-pocket limit, coverage of dental care and hearing aids, and integrated drug benefits. Medicare Extra would be available to all Americans, regardless of income, health status, age, or insurance status.

Employers would have the option to sponsor Medicare Extra and employees would have the option to choose Medicare Extra over their employer coverage. Medicare Extra would strengthen, streamline, and integrate Medicaid coverage with guaranteed quality into a national program.

The cost of coverage would be offset significantly by reducing health care costs. The payment rates for medical providers would reference current Medicare rates—and importantly, employer plans would be able to take advantage of these savings. Medicare Extra would negotiate prescription drug prices by giving preference to drugs whose prices reflect value and innovation. Medicare Extra would also implement long overdue reforms to the payment and delivery system and take advantage of Medicare’s administrative efficiencies. In this report, CAP also outlines a package of tax revenue options to finance the remaining cost.

Medicare Extra for All would guarantee universal coverage and eliminate underinsurance. It would guarantee that all Americans can enroll in the same high-quality plan, modeled after the highly popular Medicare program. At the same time, it would preserve employer-based coverage as an option for millions of Americans who are satisfied with their coverage.

Health systems in developed countries

In developed countries, health systems that guarantee universal coverage have many variations—no two countries take the exact same approach.5 In England, the National Health Service owns and runs hospitals and employs or contracts with physicians. In Denmark, regions own and run hospitals, but reimburse private physicians and charge substantial coinsurance for dental care and outpatient drugs. In Canada, each province and territory runs a public insurance plan, which most Canadians supplement with private insurance for benefits that are not covered, such as prescription drugs or vision and dental care. In Germany, more than 100 nonprofit insurers, known as “sickness funds,” are payers regulated by a global budget, and about 10 percent of Germans buy private insurance, including from for-profit insurers. Across all of these systems, the share of health spending paid for by individuals out of pocket ranges from 7 percent in France to 12 percent to 15 percent in Canada, Denmark, England, Germany, Norway, and Sweden.6 In short, health systems in developed countries use a mix of public and private payers and are financed by a mix of tax revenue and out-of-pocket spending.

In the United States, Medicare is a model of these systems for the elderly population and provides a choice of a government plan or strictly regulated plans through Medicare Advantage. Medical providers are private and are reimbursed by the government either directly or indirectly.

These various systems share two defining features. First, payment of premiums through the tax system—rather than through insurance companies—guarantees universal coverage. The reason is that eligibility is automatic because individuals have already paid their premiums. Second, these systems use their leverage to constrain provider payment rates for all payers and ensure that prices for prescription drugs reflect value and innovation. This is the main reason why per capita health care spending in the United States remains double that of other developed countries.7

Medicare Extra: Legislative specifications

Medicare Extra adopts the U.S. Medicare model and incorporates both of the common features of systems in developed countries. The following are detailed legislative specifications for the plan.

Eligibility

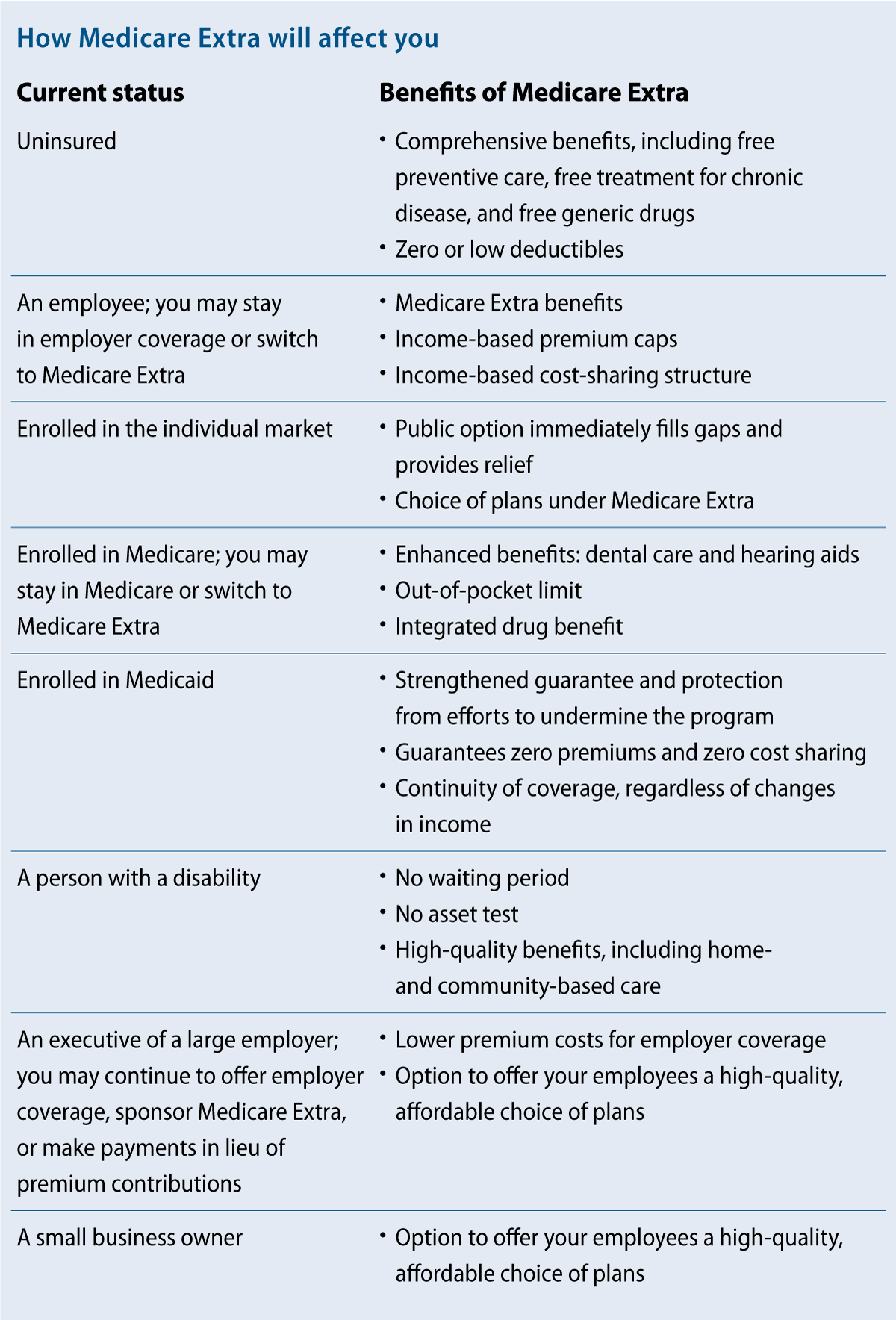

All individuals in the United States would be automatically eligible for Medicare Extra. Individuals who are currently covered by other insurance—original Medicare, Medicare Advantage, employer coverage, TRICARE (for active military), Veterans Affairs medical care, or the Federal Employees Health Benefits Program (FEHBP), all of which would remain—would have the option to enroll in Medicare Extra instead. Individuals who are eligible for the Indian Health Service could supplement those services with Medicare Extra.

Newborns and individuals turning age 65 would be automatically enrolled in Medicare Extra. This auto-enrollment ensures that Medicare Extra would continue to increase in enrollment over time.

Individuals who are not enrolled in other coverage would be automatically enrolled in Medicare Extra. Participating medical providers would facilitate this enrollment at the point of care. Premiums for individuals who are not enrolled in other coverage would be automatically collected through tax withholding and on tax returns. Individuals who are not required to file taxes would not pay any premiums.

In concert with comprehensive immigration reform, people who are lawfully residing in the United States would be eligible for Medicare Extra.

Benefits

Medicare Extra would provide comprehensive benefits, including free preventive care, free treatment for chronic disease, and free generic drugs. The plan would guarantee the following benefits:8

- Primary and preventive services

- Hospital services, including emergency services

- Ambulatory services

- Prescription drugs and medical devices

- Laboratory services

- Maternity, newborn, and reproductive health care

- Mental health and substance use disorder services

- Habilitative and rehabilitative services

- Dental, vision, and hearing services

- Early and periodic screening, diagnostic, and treatment services for children

Over time, these benefits would be updated, just as benefits are updated under Medicare, through its National Coverage Determination (NCD) process.

The Center for Medicare Extra (described below) would determine base premiums that reflect the cost of coverage only. These premiums would vary by income based on the following caps:

- For families with income up to 150 percent of the federal poverty level (FPL), premiums would be zero.9

- For families with income between 150 percent and 500 percent of FPL, caps on premiums would range from 0 percent to 10 percent of income.

- For families with income above 500 percent of FPL, premiums would be capped at 10 percent of income.

The average share of costs covered by the plan, or “actuarial value,” would also vary by income. For individuals with income below 150 percent of FPL, the actuarial value would be 100 percent—meaning these individuals would face zero out-of-pocket costs. The actuarial value would range from 100 percent to 80 percent for families with middle incomes or higher.

Consistent with these actuarial values, the Center for Medicare Extra would set deductibles, copayments, and out-of-pocket limits that would vary by income. For individuals with income below 150 percent of FPL and lower-income families with incomes above that threshold, the deductible would be set at zero. Preventive care, recommended treatment for chronic disease, and generic drugs would be free.

Enrollees would have a free choice of medical providers, which would include any provider that participates in the current Medicare program. Copayments would be lower for patients who choose centers of excellence that deliver high-quality care, as determined by such measures as the rate of hospital readmissions.

With the exception of employer-sponsored insurance, private insurance companies would be prohibited from duplicating Medicare Extra benefits, but they could offer complementary benefits during an open enrollment period. Complementary insurance would be subject to a limitation on profits and banned from denying applicants, varying premiums based on age or health status, excluding pre-existing conditions, or paying fees to brokers.

Long-term services and supports

Millions of Americans rely on long-term services and supports (LTSS) to support their daily living needs, making expansion and improvement of LTSS coverage an important part of health care reform, especially for Americans with disabilities.

Currently, individuals with disabilities who receive Social Security Disability Insurance are subject to a two-year waiting period before they are eligible for Medicare. Medicare Extra would eliminate this waiting period. In addition, individuals with disabilities can be disqualified from Medicaid coverage if their assets exceed a limit. Medicare Extra would eliminate this asset test and allow individuals with disabilities to earn and keep their savings.

Under the current Medicaid program, there is a wide variation in the benefits offered for LTSS. Medicare Extra would establish a benefit standard based on the benefits of high-quality states, as rated by access and affordability. The Medicare Extra benefit would include coverage of home and community-based services, which make it possible for seniors and people with disabilities to live independently instead of in institutions.

As discussed below, states would make maintenance-of-effort payments to Medicare Extra. States that currently provide more benefits than the Medicare Extra standard would be required to maintain those benefits, sharing the cost with the federal government as they do now. States would continue to administer the benefits that would be financed by Medicare Extra.

The Center for American Progress is developing additional LTSS policy options to supplement this new Medicare Extra benefit.

Medicare Choice

Within the current Medicare program, Medicare Advantage provides a choice of plans that deliver Medicare benefits to seniors. Currently, an estimated 20.4 million seniors are enrolled in Medicare Advantage, or 34 percent of total Medicare enrollment.10 There is evidence that these plans can provide care that is high quality.11 However, Medicare often overpays these plans compared with the traditional Medicare program.12

Medicare Extra would reform Medicare Advantage and reconstitute the program as Medicare Choice. Medicare Choice would be available as an option to all Medicare Extra enrollees. Medicare Choice would offer the same benefits as Medicare Extra and could also integrate complementary benefits for an extra premium.

To eliminate overpayments to plans, Medicare Extra would use its bargaining power to solicit bids from plans. Medicare Extra would make payments to plans that are equal to the average bid, but subject to a ceiling: Payments could be no more than 95 percent of the Medicare Extra premium. This competitive bidding structure would guarantee that plans are offering value that is comparable with Medicare Extra. If consumers choose a plan that costs less than the average bid, they would receive a rebate. If consumers choose a plan that costs more than the average bid, they would pay the difference.

Employer choice

U.S. employers currently provide coverage to 152 million Americans and contribute $485 billion toward premiums each year.13 Surveys indicate that the majority of employees are satisfied with their employer coverage.14 Medicare Extra would account for this satisfaction and preserve employer financing so that the federal government does not unnecessarily absorb this enormous cost.

At the same time, employer coverage is becoming increasingly unaffordable for many employees. Among employees with a deductible for single coverage, the average deductible has increased by 158 percent—faster than wages—from 2006 to 2017.15 The Health Care Cost Institute recently found that price growth accounts for nearly all of the growth in health care costs for employer-sponsored insurance.16

Medicare Extra balances the desire of most employees to keep their coverage with the need of many employees for a more affordable option. Employers would have four options designed to ensure that they pay no more than they currently do for coverage.

First, employers may choose to continue to sponsor their own coverage. Their coverage would need to provide an actuarial value of at least 80 percent and they would need to contribute at least 70 percent of the premium; the vast majority of employers already exceed these minimums.17 The current tax benefit for premiums for employer-sponsored insurance—which excludes premiums from income that is subject to income and payroll taxes—would continue to apply (as modified below).

Second, employers may choose to sponsor Medicare Extra for all employees as a form of employer-sponsored insurance. Employers would need to contribute at least 70 percent of the Medicare Extra premium. Under this option, employers would automatically enroll all employees into Medicare Extra. The Medicare Extra cost-sharing structure would apply and employees would pay the Medicare Extra income-based premium for their share of the premium. The tax benefit for employer-sponsored insurance would not apply to premium contributions under this option.

Third, employers may choose to make maintenance-of-effort payments, with their employees enrolling in Medicare Extra. These payments would be equal to their health spending in the year before enactment inflated by consumer medical inflation. To adjust for changes in the number of employees, health spending per full-time equivalent worker (FTE) would be multiplied by the number of current FTEs in any given year. The tax benefit for employer-sponsored insurance would not apply to employer payments under this option.

Fourth, employers may choose to make simpler aggregated payments in lieu of premium contributions. These payments would range from 0 percent to 8 percent of payroll depending on employer size—about what large employers currently spend on health insurance on average.18 The tax benefit for employer-sponsored insurance would not apply to employer payments under this option.

Small employers—71 percent of which do not currently offer coverage—would not need to make any payments at all.19 They may choose to offer no coverage, their own coverage subject to ACA rules in effect before enactment, or Medicare Extra. Small employers are defined as employers that employ fewer than 100 FTEs for purposes of the options described above.20

Employee choice

When employers choose to offer their own coverage, employees may choose to enroll in Medicare Extra instead.21 At the beginning of open enrollment, employers would notify employees of the availability of Medicare Extra and provide informational resources. If employees do not make a plan selection, employers would automatically enroll them into their own coverage.

When employees enroll in Medicare Extra, their employers would contribute the same amount to Medicare Extra that they contribute to their own coverage. The Medicare Extra income-based premium caps would apply to the employee share of the premium. Because employees would be subsidized by Medicare Extra, the tax benefit for employer-sponsored insurance would not apply to employer premium contributions under this option.

State maintenance of effort

Medicaid and the Children’s Health Insurance Program (CHIP) would be integrated into Medicare Extra with the federal government paying the costs. Given the continued refusal of many states to expand Medicaid and attempts to use federal waivers to undermine access to health care, this integration would strengthen the guarantee of health coverage for low-income individuals across the country. It would also ensure continuity of care for lower-income individuals, even when their income changes.

States would be required to make maintenance-of-effort payments to Medicare Extra equal to the amounts that they currently spend on Medicaid and CHIP.22 For states that did not expand Medicaid, these amounts would be inflated by the growth in gross domestic product (GDP) per person plus 0.7 percentage points.23 For states that did expand Medicaid, these amounts would be inflated by the growth in GDP per person plus 0.2 percentage points. After 10 years of payments, they would then increase by the growth in GDP per person plus 0.7 percentage points for all states. This structure would ensure that no state spends more than they currently spend, while giving a temporary discount to states that expanded their Medicaid programs.

States that currently provide benefits that are not offered by Medicare Extra would be required to maintain those benefits, sharing the cost with the federal government as they do now. They would provide “wraparound” coverage that would supplement Medicare Extra coverage.

Administration

Medicare Extra would be administered by a new, independent Center for Medicare Extra within the current Centers for Medicare and Medicaid Services, which would be renamed the Center for Medicare. To ensure that the Center for Medicare Extra is immune from partisan political influence within the administration, the legislative statute would leave little to no discretion to the administration on policy matters. In this respect, the administration of Medicare Extra would resemble the administration of the current Medicare program and not of the Medicaid program.

Transitioning to Medicare Extra

The transition to Medicare Extra would be staggered to ensure a smooth implementation. The steps would be sequenced based on need, fairness, and ease of implementation. Before Medicare Extra is launched, a public option would fill immediate gaps and provide immediate relief.

In the first year after enactment (Year 1), the Center for Medicare Extra would be established and would offer a public option in any counties that are not served by any insurer in the individual market. The provider payment rates of the plan would be 150 percent of Medicare rates. In Year 2, this plan could be extended to other counties in the individual market.

In Year 4, the Center would launch Medicare Extra. Auto-enrollment would begin for current enrollees in the individual market, the uninsured, newborns, and individuals turning age 65. Enrollees in the current Medicare program and employees with employer coverage would have the option to enroll in Medicare Extra instead. Small employers would have the option to sponsor Medicare Extra for all employees.

In Year 6, enrollees in Medicaid and CHIP would be auto-enrolled into Medicare Extra. In Year 8, large employers would have the option to sponsor Medicare Extra for all employees, and the tax benefit for employer-sponsored insurance would be limited for high-income employees.

Financing Medicare Extra

Medicare Extra would be financed by a combination of health care savings and tax revenue options. CAP intends to engage an independent third party to conduct modeling simulation to determine how best to set the numerical values of the parameters. Developed countries are able to guarantee universal coverage while spending much less than the United States because their systems use leverage to constrain prices. In the United States, adopting Medicare’s pricing structure—even at levels that restrain prices by less than European systems—is an essential part of financing universal coverage.

Health care savings

Provider payment rates

Extensive research recently has shown that variation in prices charged by medical providers is the main driver of health care costs for commercial insurance.24 Hospital systems in particular can act as a monopoly, dictating prices in areas where there is little competition. Excessive prices are not a major issue for Medicare because it has leverage to set prices administratively.

To lower both the level and growth of health care costs, provider payment rates under Medicare Extra would reference current Medicare rates. Currently, Medicaid rates are lower than Medicare rates, and both are significantly lower than commercial insurance rates.25 Medicare Extra rates would be lower than current commercial rates in noncompetitive areas where hospitals reap windfalls, but higher than current Medicaid and Medicare rates.

Medicare Extra rates would reflect an average of rates under Medicare, Medicaid, and commercial insurance—minus a percentage. For illustrative purposes, CAP estimates that if Medicare Extra rates are 100 percent of Medicare rates for physicians and 120 percent of Medicare rates for hospitals, the rates would be roughly 10 percentage points lower than the current average rate across payers.26 For rural hospitals, these rates would be increased as necessary to ensure that they do not result in negative margins.

For physicians, average rates for primary care would be increased by 20 percent relative to certain rates for specialty care on a budget neutral basis. This adjustment would correct Medicare’s substantial bias in favor of specialty care at the expense of primary care. Extensive research suggests that greater shares of spending on primary care result in lower costs and higher quality of care.27

Importantly, the benefits of Medicare Extra rates would extend to employer-sponsored insurance and significantly lower premiums. For employer-sponsored insurance, providers that are out of network would be prohibited from charging more than Medicare Extra rates. Research shows that this type of rule—which currently applies to Medicare Advantage plans—indirectly lowers rates charged by providers that are in network.28

Prescription drug costs

Until Medicare Extra is launched, drug manufacturers would pay the Medicaid rebate on drugs covered under Medicare drug plans for low-income beneficiaries. The Congressional Budget Office estimates that this policy would reduce federal spending by $134 billion over 10 years.29

The Congressional Budget Office estimates that this policy would reduce federal spending by $134 billion over 10 years.

Medicare Extra would negotiate prices for prescription drugs, medical devices, and durable medical equipment. To aid the negotiations, multiple nonprofit, independent evaluators would vet data submitted by manufacturers, conduct studies, and make periodic value assessments. If negotiated prices are within the range of prices recommended by all evaluators, Medicare Extra would include the product on a preferred tier with limited cost sharing. If prices for existing products rise faster than inflation, manufacturers would pay rebates on products covered under Medicare Extra—just as they do under the current Medicaid program.

Payment and delivery system reform

Medicare Extra would reform the payment and delivery system to reward high-quality care. Medicare Extra would pay hospitals for a bundle of services, including associated care for 90 days after discharge. The objective of this reform is to reduce variation in post-acute care, which is the main driver of health care costs under Medicare.30 Medicare Extra would phase in this reform over three years until it applies to half of spending on hospital admissions.

Medicare Extra would make “site-neutral” payments—the same payment for the same service, regardless of whether it occurs at a hospital or physician office.31 The current Medicare program pays hospitals far more than it pays freestanding physician offices for physician office visits. Not only is this excess payment wasteful, it provides a strong incentive for hospitals to acquire physician offices—aggregating market power that drives up prices for commercial insurance.

Administrative efficiencies

Excessive administrative costs are a key reason why health care costs are so much higher in the United States compared to other developed countries.32 Medicare Extra would take advantage of the current Medicare program’s low administrative costs, which are far lower than the administrative costs of private insurance.33 In particular, the cost and burden to physicians of administering multiple payment rates for multiple programs and payers would be greatly reduced.

In addition to having economies of scale and no need to make a profit, Medicare Extra would implement several administrative efficiencies. Providers would only need to report one set of quality measures and physicians would only need to submit one set of clinical credentials. Medicare Extra and providers would transmit claims information and payment electronically.34 Electronic health records would automatically convert clinical entries into claims information. Importantly, so-called churning between Medicaid and the individual market—in which individuals must frequently enroll and unenroll due to changes in eligibility—would be eliminated.35

Tax revenue options

The American people have many major unmet needs. Medicare Extra is carefully designed to leverage existing financing by states and employers and extract maximum savings so that the program would not consume all potential sources of tax revenue. Some combination of the following tax revenue options would be sufficient to finance the remaining cost of Medicare Extra.

The recently enacted Tax Cut and Jobs Act (TCJA) lowered the corporate tax rate from 35 percent to 21 percent and enacted several other tax cuts skewed toward the wealthy. As part of a broader effort to replace the tax bill, some of the revenue could help finance Medicare Extra.

Medicare Extra would be financed in part by taxes on high-income individuals. One option would be a surtax on adjusted gross income—including capital gains—on very high-income individuals. CAP’s modeling will determine the exact parameters of the surtax, including the rate. In addition, under current law, large accumulations of wealth are never subject to capital gains taxes if held until death and transferred to heirs. One option would be to eliminate this stepped-up basis so that large accumulations of wealth cannot avoid capital gains tax.

Medicare Extra would also be financed in part by increasing health care taxes and curtailing health care tax breaks. For high-earners—singles with income above $200,000 and couples with income above $250,000—the additional Medicare payroll tax and the Medicare net investment income tax (NIIT) could be increased. In addition, all business income of high-income taxpayers—including S corporation shareholders, limited partners, and members of limited liability companies—could be subject to the Medicare tax either through self-employment taxes or the NIIT. The tax benefit from the exclusion for employer-sponsored insurance would be capped at 28 percent. In addition, lower premiums for employer-sponsored insurance would significantly reduce this tax expenditure. Medicare Extra would also obviate the need for tax benefits for flexible spending accounts and health savings accounts.

Lastly, Medicare Extra would be financed in part through public health excise taxes. The federal excise tax on cigarettes would be increased by 50 cents per pack and adjusted for inflation. A tax could also be imposed on sugared drinks equal to 1 cent per ounce. These taxes would reduce health care spending, helping to offset the cost of Medicare Extra.

Conclusion

Medicare Extra for All would guarantee the right of all Americans to enroll in the same high-quality plan, modeled after the highly popular Medicare program. It would eliminate underinsurance, with zero or low deductibles, free preventive care, free treatment for chronic disease, and free generic drugs. It would provide additional security to individuals with disabilities, strengthen Medicaid’s guarantee, improve benefits for seniors, and give small businesses an affordable option. At the same time, enrollees would have a choice of plans, and employer coverage would be preserved for millions of Americans who are satisfied with it.

Our society will be judged by how it treats the sickest and the most vulnerable among us. Health care is a right, not a privilege, because our positions in life are influenced a great deal by circumstances at birth; and beyond birth, the lottery of life is unpredictable and outside of one’s control.

America, the most powerful and wealthiest nation in the history of civilization, has endured a long journey spanning decades to fulfill these principles. The country has slowly added step upon step toward universal health coverage. The ACA was a giant step, and the sustained political fight over the law showed that the American people want to expand coverage, not repeal it. It is now time to guarantee universal coverage and health security for all Americans.