Introduction and summary

Almost every step of America’s food supply chain has grown more concentrated in the past few decades. From manufacturers of agricultural inputs such as pesticides and equipment to commodity buyers and meat processors, growing corporate power has left relatively small farms and ranches vulnerable to exploitation at the hands of the oligopolies with which they do business. Recent mergers and acquisitions continue the relentless trend toward increasing corporate concentration across many agricultural markets. This report examines two key markets—for corn and soybean seeds and for hogs—and finds evidence that market concentration has resulted in considerable corporate market power, to the detriment of America’s farmers.

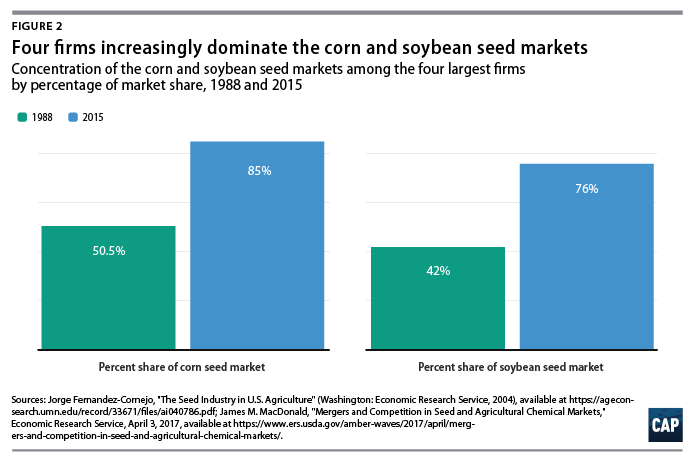

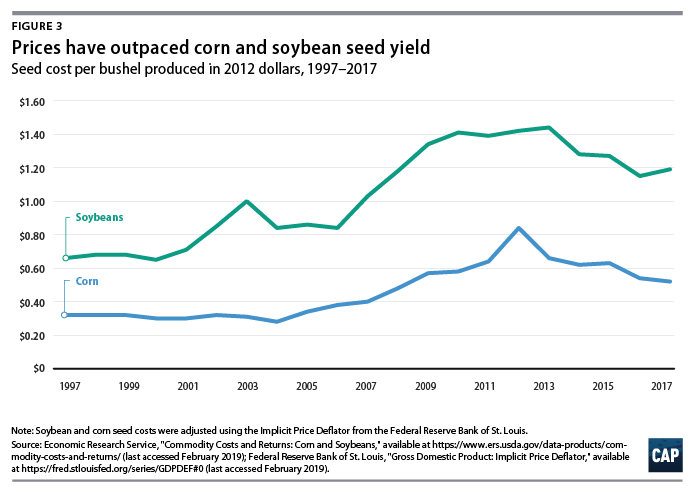

For example, the share of the corn seed market that is controlled by the four largest biotech companies has risen from 50.5 percent in 1988 to 85 percent in 2015. (see Figure 2) Meanwhile, the increase in the price of corn and soybean seeds has outpaced increases in yield. Moreover, spending on research and development (R&D) in the sector seems to be slowing, and farmers face diminished choice in seed.1 Between 1995 and 2011, the cost of purchasing seed to plant one acre of soybeans and corn increased 325 percent and 259 percent, respectively, while yield per acre only increased 18.9 percent and 29.7 percent, respectively.2

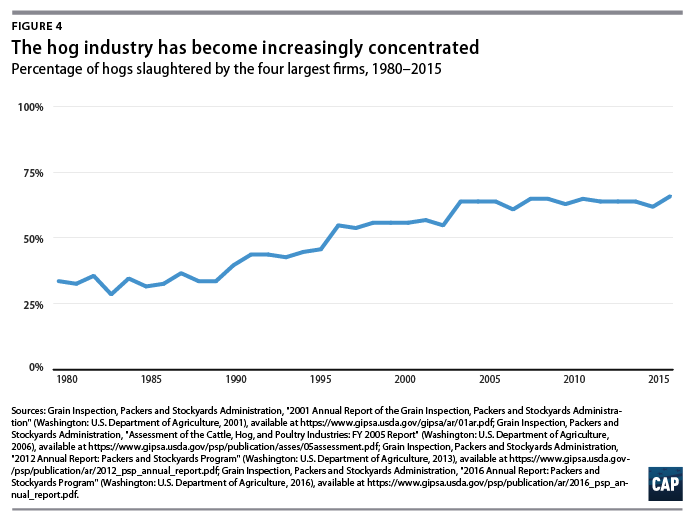

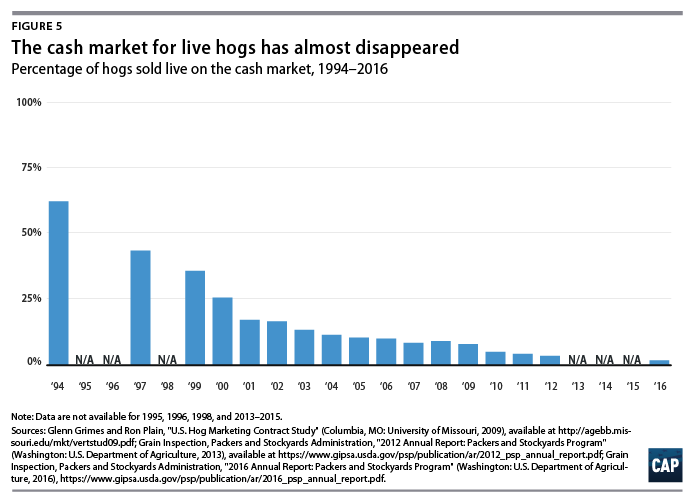

Hog farmers face increasing processor buyer power resulting from the twin trends of increasing concentration and the prevalence of production contracts. As of 2015, 66 percent of all hogs were slaughtered by the four largest meatpackers, up from 34 percent in 1980.3 Meanwhile, 63 percent of hogs were raised under contract with processors, and only 2 percent of hogs were sold in the cash spot market.4 (see Figure 5) The rest were raised on packer-owned and -operated lots. With only a handful of processors with which they can do business, hog farmers have little choice but to enter into contracts that compensate them through opaque and often manipulatable pricing formulas that saddle farmers with burdensome terms and quite often large levels of debt.

The resulting impacts on farmers’ ability to share in the fruits of their labor are severe. Indeed, agricultural economists who modeled farmer and consumer welfare under various degrees of market power among buyers note that even a modest departure from a perfectly competitive market can result in a 30 percent decrease in farmer surplus.5 The increasing difference between the price paid to hog farmers and the wholesale price of pork is consistent with the hypothesis that processors are benefiting from market power, in part at the expense of farmers’ livelihoods. (see Figure 6)

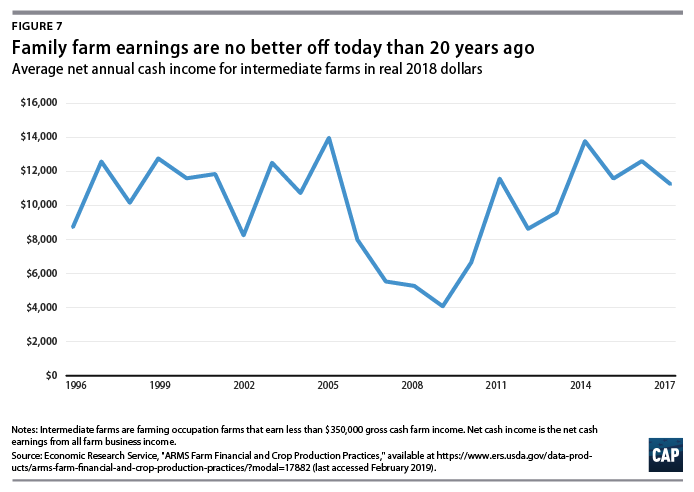

Similar challenges exist across American agriculture and ranching. It is not surprising then that small and midsize farmers struggle to keep their operations running and make ends meet. Indeed, real net farm income for intermediate farms—defined as family farms operated by someone whose primary occupation is farming and with annual gross cash receipts of less than $350,000—has seen little improvement over the past two decades.6 As of 2017, more than 40 percent of midsize farms—defined as family farms with gross cash receipts between $350,000 and $1 million—had an operating profit margin of less than 10 percent, placing them at high risk of financial problems, according to the U.S. Department of Agriculture (USDA).7

While a wide range of economic forces—from volatile international trade relations to climate change to technological upheaval—put economic pressure on America’s farmers, the impact of monopoly power on farmers can no longer be ignored. Like millions of workers whose wages have been stagnant in recent decades, farmers are quite simply not receiving a fair share of the returns from their labor. With 1 in 5 rural counties dependent on farming, and a rural poverty rate 3.5 percent higher than in urban areas, rural America cannot afford depressed farm earnings.8

The analysis in this report aims to shed light on the impact that corporate concentration and the subsequent decline in competition in agricultural input and commodity markets have had on farm families and their communities. This report concludes with a set of specific recommendations that aim to increase competition; empower farmers to secure their fair share; and protect farmers from an array of unfair, deceptive, and abusive practices in these markets. These recommendations include:

- Restoring competition in agricultural markets: Reviving strong antitrust enforcement across the agricultural sector is the starting point for protecting farmers and ranchers. Specific steps include a temporary moratorium on mergers in the agriculture sector, a statutory cap on concentration in various agriculture markets, and more broadly restoring the powerful tools of antitrust enforcement that have been eroded over the past four decades. Antitrust enforcers must also take affirmative steps to break up monopolies and monopsonies, while federal policy should proactively support the growth of new competitors.

- Guaranteeing a fair share for farmers: Farmers must be empowered to receive a fair share of the fruits of their labor. Policymakers must implement alternative tools such as pricing models that guarantee farmers a percentage share of the ultimate returns on their commodities, as is the case today in some agricultural markets such as that of wine grapes. Alternative bargaining models can also be deployed to help farmers and workers receive a fair return, including farmer fair share boards made up of farmers, workers, and processors to facilitate farmer and worker collective bargaining with large buyers over commodity prices.

- Codifying contract reform to protect farmer rights: The dramatic trend in many agricultural markets toward production under contract, rather than the sale of product on the spot market, means it is essential that contracts be regulated to protect farmers from unfair, abusive, and deceptive practices by large buyers. Farmers must also be empowered to better protect their interests under the law when they suffer violations of their rights.

- Creating an Independent Farmer Protection Bureau (IFPB): America’s independent farmers deserve to have a dedicated, independent champion fighting for their interests against highly concentrated agribusiness. Modeled after the Consumer Financial Protection Bureau, which was created to protect consumers from the predatory financial practices that helped cause the 2008 financial crisis, an Independent Farmer Protection Bureau should be empowered to investigate and stop abuses of market power; protect farmers’ contract rights under laws such as the Packers and Stockyards Act; combat anti-competitive practices in seed and other input markets; and more. The IFPB should have backup authority to review and block mergers in markets that affect farmers.

The agricultural sector is vitally important to America’s economy and society. Two million American families still operate farms and ranches, and farm output contributed $164.2 billion to the United States’ gross domestic product (GDP) in 2018.9 Nationally, food is the third-largest household expenditure, comprising nearly 13 percent of monthly household expenses, and all told, farming and agricultural processing employs 4.6 million Americans.10 Therefore, the economic health of the agricultural sector and the food system is crucial to America’s economy. Restoring agriculture as a pathway to a decent, independent living will begin the process of rebuilding rural America.

The changing structure of America’s food system

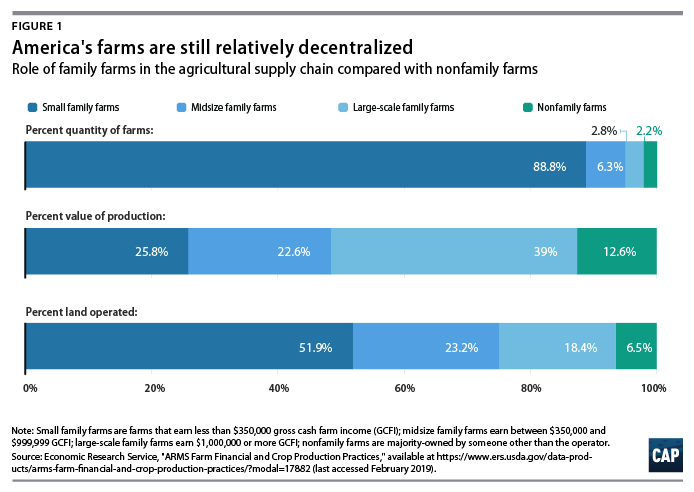

Over the past few decades, America’s agriculture sector has undergone increasing concentration at nearly every step of food production and marketing. Agricultural inputs—which include seed, crop protection chemicals, machinery, and more—processing, food manufacturing, and retail are now dominated by a handful of firms in their respective markets.11 The only part of the supply chain that remains relatively decentralized is the actual production of agricultural goods. Small and midsize family farms operate nearly three-fourths of all farmland and account for about half of all production. (see Figure 1) The concentration of agricultural input suppliers and commodity buyers raises the possibility that some firms may use their size to exert power over relatively small farms.

Measures of concentration

Concentration and relative size do not necessarily equate to market power, though they do contribute to it. Monopoly power is difficult to directly measure, so government agencies and economists use concentration measures, such as the four-firm concentration ratio and the Herfindahl-Hirschman Index (HHI)—which captures the relative size of dominant firms in relation to each other—as useful heuristics to estimate it.

Concentration ratio: The sum of the four largest firms’ market shares.

Herfindahl-Hirschman Index: The squared sum of the market shares—expressed as a percentage—of all participants in a market. The DOJ and the Federal Trade Commission (FTC) use this measure when they evaluate proposed mergers and acquisitions.12 HHI values range from 0 to 10,000, the latter of which indicates an absolute monopoly or monopsony under FTC and DOJ standards.

According to the 2010 FTC and DOJ merger guidelines:

- An HHI of less than 1,500 indicates an unconcentrated industry.

- An HHI of between 1,500 and 2,500 indicates moderate concentration.

- An HHI of more than 2,500 indicates high concentration.

Rising concentration in input markets

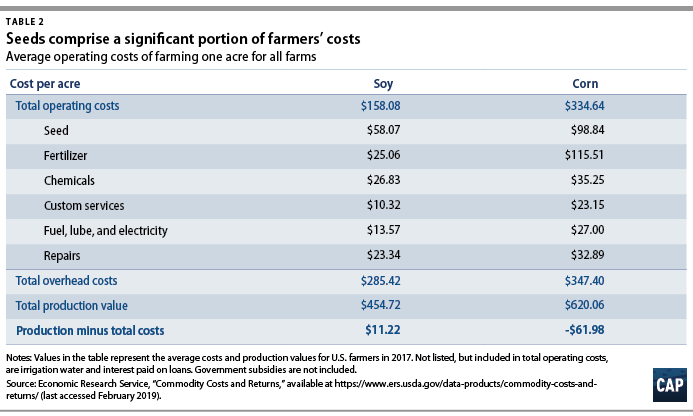

Like other small-business owners, farmers must purchase the inputs necessary for the production process. The chief operational expenses that farmers pay to run their business are for feed, labor, livestock, seed, and fertilizer.13 For crop farmers, net farm income is sensitive to the price of seed and fertilizer, as well as capital investments in equipment such as tractors or irrigation systems. Unfortunately, as concentration in agricultural inputs increases and the quantity of suppliers declines, farmers and ranchers may find it difficult to keep costs under control and maintain a livable income.

The consolidation of agricultural input markets is widespread. As of 2012, the four-firm concentration ratio—the percent of a market controlled by the four largest participants—in the markets for pesticide manufacture was 57 percent.14 The four largest firms in the farm machinery industry account for half of all sales.15 The four-firm concentration ratio in livestock pharmaceuticals and farm machinery has also increased significantly since the 1990s.16 The high levels of consolidation in agricultural input markets raise legitimate competition concerns.

The seed market serves as a good example of the widespread consolidation occurring throughout the agricultural supply chain. The rise of biotechnology in the seed market created a new industry that integrated traditional hybrid methods, modern genetic modification, and chemical manufacturing. A wave of mergers and acquisitions in the 1990s and 2000s gave birth to a handful of dominant biotech firms.17 Between 1985 and 2009, the vast majority of acquisitions of small and medium-sized biotech companies were acquired by the six largest companies.18 By 2013, four companies accounted for nearly 60 percent of the seed market.19 The implications of this concentration are discussed below in a case study on corn and soybean seeds.

Despite pressing concerns about the impact of high levels of concentration, the U.S. Department of Justice (DOJ), which is responsible for antitrust enforcement in the agriculture sector, has taken a surprisingly permissive stance on agrichemical and biotech company mergers, permitting the number of dominant firms to shrink from six to four. For example, in 2018, the DOJ permitted the Bayer-Monsanto merger on the condition that merging parties divest holdings in narrowly drawn input markets in which they directly competed.20 The remedies for the Bayer-Monsanto merger were complex, necessitating dramatic transfers of personnel and complementary divisions as well as extensive oversight to maintain the firewall meant to preclude collusion between the merged firm and BASF—a third biotech giant that bought the divested assets.21

While it is too early to observe all the ramifications of recent mergers, consolidation has had serious, observable effects on farmers.22 One recent merger retrospective, authored by two former attorneys from the DOJ’s Antitrust Division, surveyed 1,000 farmers to gauge how they were affected by the Bayer-Monsanto merger. The 2018 survey found that 80 percent of crop farmers reported that their seed prices increased over the past five years. Nearly two-thirds of those surveyed expressed feeling that they have less bargaining power when buying seed than they had previously enjoyed.23 This means lost dollars and cents for farmers who have no choice but to source their seeds from a dwindling number of manufacturers. The case study below of corn and soybean seed markets illustrates the real-world implications of seed monopolies on farmers.

Growing buyer concentration and prevalence of contracting

Farmers also face increasingly consolidated firms when selling the commodities that they produce. Direct farmer-to-consumer sales make up a negligible portion of farmers’ sales; most farmers’ real customers are the processors, grain traders, and marketers that buy raw goods from farmers and then grade, package, process, manufacture, and distribute them as food products. In recent years, these processors have consolidated at rates comparable to those of agrichemical and biotech companies. Increased concentration among food processors presents a risk of monopsony power—the exertion of market power by a large buyer to influence the price or quality of its inputs. A series of 2010 nationwide workshops held by the DOJ revealed that monopsony power is a pressing concern of farmers.24

While increasing concentration is not uniform across all agricultural commodity markets, there are some that have exhibited alarming rates of consolidation. For example, from 1986 to 2008, the four-firm share of animal slaughter nationwide increased from 55 percent to 79 percent for cattle, from 33 percent to 65 percent for hogs, and from 34 percent to 57 percent for poultry.25 The concentration level of processing varies from market to market. While this report focuses on pork processing as a case study of concentration and the threat that possible monopsony power poses for hog farmers, there are other markets that are at least as concentrated as pork processing. For example, the four largest wet corn millers and soybean processors control 84 percent and 82 percent of their respective national markets.26 Similarly, four grain traders control the movement and allocation of nearly 73 percent of the world’s grain.27 The beef packing industry has an astounding four-firm market concentration of 82 percent.28 Meanwhile, the top four specialty canners account for nearly three-fourths of the market for goods such as beans, baby food, and soups.29

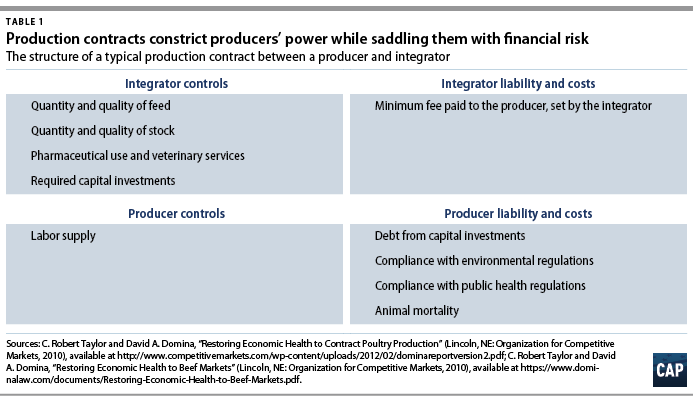

As concentration among processors has increased, so has the importance of sales through contracts between the processor and the grower, as opposed to on the open cash, or spot, markets. These contract agreements arrange the terms of sale for commodities before they are produced. In 2017, more than one-third of the value of agricultural commodities was produced under contract, though this varies greatly across commodities.30 These contracts come in two main varieties. Marketing contracts typically specify the amount of a commodity that a processor will purchase from a farmer and determine the price that the processor will pay, often using a formula based on spot market prices. Production contracts go further by dictating the way in which livestock is raised or field crops are grown, sometimes down to the exact type and quantities of inputs or production techniques. Often, the livestock raised and inputs such as feed are themselves owned and supplied by the packer—referred to in this report as the integrator—while contracts require farmers to make capital investments to meet integrator requirements.31 In this report, the authors refer to meatpackers and processors that rely on contracting as “integrators” to describe how the contracts effectively vertically integrate the production process, though this term is not generally used to describe processors outside the broiler industry.

At their core, production contracts are a way for integrators to control the quantity and quality of inputs that they process while cutting costs and minimizing risk.32 While the nature of contracting varies across commodity markets, contract poultry serves as an apt illustration of how these contracts work to effectively vertically integrate agricultural production. Though farmers have limited control over the way they can raise the animals, their contracts nonetheless determine that they bear much of the liability and risk for raising the animals owned by the integrator. The typical contracting arrangement gives the integrator the power to control the type and quantity of stock raised, the pharmaceuticals used, the type of feed used, and the equipment and facilities required. The integrator owns the animals, supplies the required feed, and controls the veterinarian services that the farmers use, while farmers assume debt in order to meet capital investment requirements.33 The typical contract explicitly assigns legal liability for regulatory compliance and animal fatalities to the farmers.34

With the number of packers dwindling, most farms have little bargaining power with which to negotiate the terms of these contracts, resulting in extractive terms. Farmers must accept the terms of the contract as written by the integrator or find another integrator. The integrator sets the terms of compensation, usually as a per-unit rate based on a pricing formula with some bonuses or penalties associated with yield, efficiency, or quality. Farmers who attempt to organize or negotiate better terms risk intimidation and retaliation, for example, through the threat of termination of the contract or the supply of substandard livestock or feed. Poultry integrators and, to a lesser extent, pork integrators, use a so-called tournament system in which farmers are ranked by efficiency and paid according to their ranking. Farmers often call this system the “lottery” because after their capital investments are made, the performance of a farm is heavily dependent on the quality of inputs that the integrator allocates to it.35

These provisions had come under heightened scrutiny thanks to a mandate in the 2008 Farm Bill that was inserted by then-Chairman of the Senate Agriculture Committee Tom Harkin (D-IA) that required the Grain Inspection, Packers and Stockyards Administration (GIPSA) to formulate rules clarifying unfair and deceptive contracting practices, which were ultimately implemented by the Obama administration in 2016.36 Notably, one of the first acts of President Trump’s USDA was to withdraw those rules.37 Though weakened after years of fierce lobbying by one of the most powerful interests in Washington—the meat lobby—the Farmer Fair Practices Rules still would have locked in significant reforms that would have begun to fix a deeply flawed system rigged against America’s farmers. These rules included commonsense provisions that banned price discrimination between similar growers and retaliation against farmers who organize for better contract terms.38 The rules also promised to protect farmers from the bad faith negotiation and fraud that had become pervasive in industries such as hog and broiler (chicken) production.39 President Trump’s USDA further ordered that GIPSA be shuttered.40

The twin trends of horizontal consolidation and vertical integration in food processing have serious implication for farmers. The resulting thinning cash markets and increasingly powerful buyers make prices vulnerable to manipulation. While much of the discussion here focuses on livestock markets, production contracts also exist in some produce markets, demanding further study. This report continues the discussion of consolidation and integration in agriculture with a case study that examines the dynamics of the hog market.

Relatively decentralized production

In contrast to the large firms that dominate the other stages of the supply chain, the production of agricultural commodities happens on relatively decentralized farms and ranches. Nearly half of all agricultural production occurs on small and midsize family farms. (see Figure 1) Eighty-seven percent of farms are primarily worked by the owner and operator’s family. These true family farms account for 57 percent of the country’s agricultural production.41 Although the number of American farms is slowly dwindling and their average size is increasing, farms are still relatively decentralized compared with biotech companies and processors.42

In the 1950s and 1960s, industrial agricultural techniques spurred the acceleration of a trend that began during the Dust Bowl era of the Great Depression, in which millions of families moved from farms to find work in factories in major cities. Since the 1970s, a range of factors—including mechanization, automation, and concentration trends—have continued to drive farm consolidation and growth. However, the trend of farm consolidation in recent years has been less dramatic than the consolidation of inputs and processors, resulting in a food system in which small family farms must grapple with large input suppliers and large buyers.

Two key agricultural markets highlight the issue of concentration

The following case studies reveal evidence of the monopoly and monopsony power that is associated with high concentration in specific markets. Markets for specific inputs and commodities have unique characteristics that make it difficult to generalize about the effects of concentration in the agriculture sector writ large. However, many other markets have levels of concentration comparable to those of the markets studied here and therefore deserve closer scrutiny by academics, experts, antitrust enforcers, and state and federal policymakers, including Congress, the USDA, the DOJ, the FTC, and state attorneys general.

Case study: Corn and soy seed

Each year, about 180 million acres of soybeans and corn are planted in the United States, primarily in the Midwest.43 Corn and soybeans—the most and second-most planted field crops, respectively—are closely related economically, with almost no distinction between a corn and soybean farm, given that the two crops thrive in similar climates and are commonly rotated year after year to promote soil health.44 Many farmers explicitly substitute soy and corn when planning their planting, balancing the expected returns of one commodity against the other to determine the amount that they will plant of each.45 Furthermore, the corn and soybean seed markets are shaped by the same dominant firms.46 Therefore, this report will address the markets for corn and soybean seeds together.

Nearly all the corn and soybeans grown in the United States are genetically modified (GM) for resistance to herbicides, pests, or both.47 Due to their bolstered yield and the reduction in necessary labor, most farmers view GM seeds as almost indispensable to their operations. While some farmers may not consider non-GM seeds substitutes for their GM counterparts, available analysis does not distinguish between them, likely providing an overly broad definition of the corn and soybean markets and an underestimate of market concentration.48

Biotechnology companies require three main components to manufacture transgenic seeds: genetic traits, the technology necessary to transmit them, and the germplasm that carries these traits. In some seed markets, it is common for a seed to carry multiple transgenic—or “stacked”—traits. Through research and development, acquisitions, patents, and licensing agreements, biotechnology companies strategically expand their portfolio of technology, traits, and germplasms to create marketable transgenic seeds.49

By acquiring independent seed companies and the technology startups that pioneered new methods of genetic modification, a handful of dominant firms won control of the bulk of biotechnological intellectual property, and, consequently, the GM seed market. Since the mainstream success of GM seeds, four biotechnology firms—Monsanto, DuPont, Dow, and Syngenta—have emerged as dominant players in the corn and soybean seed markets.50 As of 2015, the four-firm concentration ratio for all corn and soybean seeds—GM seeds or otherwise—was 85 percent and 76 percent, respectively.51 This is an extraordinarily high level of concentration, comparable to that of the domestic airline industry.52 In 2016, before the approval of the Dow-DuPont and Bayer-Monsanto mergers, Monsanto and DuPont each accounted for more than one-third of the market for corn seed. DuPont controlled 33 percent of the soybean seed market while Monsanto closely followed with a market share of 28 percent.53 These large market shares should raise serious concerns for antitrust experts and farmer advocates alike.

In addition to consolidation, biotech companies amass market power through exclusionary practices and protective patenting. The remaining so-called independent seed companies that the four largest firms have not acquired directly are often bound by exclusive dealing agreements with biotech giants that penalize them for licensing traits from any other companies. Alternatively, bundling agreements may incentivize seed companies to ensure that a certain proportion of their seed offerings contain Monsanto traits. These practices erect anti-competitive barriers to entry for new biotech firms that attempt to market alternative traits to seed companies.54

Meanwhile, dominant biotechnology firms directly head off competition from other biotechnology companies through strategic licensing and protective patents.55 When a dominant biotech firm enters a joint venture with another firm, restrictive licensing agreements prevent the other partner from using the technology it helped to develop for other enterprises. When licensing a trait to another firm, the licensing agreement may prohibit the firm from stacking traits with those of other companies. Moreover, much like the pharmaceutical industry, transgenic seed companies employ strategic patenting to delay or block generic alternatives from entering the market.56 Using these practices, dominant firms erect high barriers to entry for firms that want to market competing seeds or traits.

Despite extremely high concentration and significant barriers to entry in the corn and soybean seed markets, the DOJ failed to address the potential anti-competitive effects of the Dow-DuPont merger. At the time of the proposed merger, Dow was the third-largest firm in the corn seed market and the fourth-largest in the soybean seed market.57 Before the Dow-DuPont and Bayer-Monsanto mergers, the HHI for corn seed was 2,696—already exceeding the threshold that the DOJ considers highly concentrated.58 According to the DOJ and FTC merger guidelines, above this threshold, mergers that result in an HHI increase of more than 200 points are “likely to enhance market power.”59 Researchers at Texas A&M University projected that the HHI in corn seed would increase by more than 400 points to 3,110 points after the consummation of both mergers.60 For soybean seeds, the HHI was expected to increase from 2,360 to 2,705 points.61 Yet the competitive impact statement of the Dow-DuPont merger filed by the DOJ and the proposed merger remedies did not mention seed markets at all, focusing instead on chemical markets.62 This oversight is alarming given the already high levels of concentration and importance of patents in the GM corn and soybean seed markets.

Increases in corn and soybean seed prices suggest that dominant firms may be extracting supracompetitive prices from farmers. In 2010, a DOJ listening tour found widespread concern among farmers about the rising cost of seed as a result of the rise of GM technology and the powerful firms that control it.63 Charles Benbrook, research professor at Washington State University’s Center for Sustaining Agriculture and Natural Resources, has observed that in a competitive market, widespread adoption of new technology such as GE seeds leads to a decrease in that technology’s price; however, the cost of GE seeds increased 230 percent from 2000 to 2010.64 Specifically, the seed cost of planting one acre of soybeans increased 325 percent between 1995 and 2011, while the cost of planting an acre of corn increased 259 percent. Meanwhile, yield only increased 18.9 percent and 29.7 percent, respectively, over the same period.65

The continued consolidation of the seed industry will likely exacerbate this trend. In 2016, researchers at Texas A&M University estimated that the mergers of Dow with DuPont and Bayer with Monsanto would result in an initial 1.9 percent increase of soybean seed prices and a 2.3 percent increase in corn seed prices.66 For the average American farm—which has a size of 444 acres—this would result in an immediate increase of more than $1,000 in annual corn seed costs in the first year alone.67 Since seed is one of the top two operating costs for soy and corn farmers, further price increases pose a serious threat to family farmers’ already thin margins.

Rising concentration in seed markets will likely result in decreased research and development, innovation, and seed choice. The Bayer-Monsanto merger, for example, appears unlikely to bring about increased innovation. The proposed budget for the company includes less than $800,000 in additional R&D, about .01 percent of the combined research budget of the two companies.68 Expert analysis has found that merger and acquisition activity and the release of new seed varieties are pro-cyclical—meaning increases in research and development coincide with or precede merger and acquisition activity, rather than follow it—which is contrary to the claim that merger and acquisition activity leads to increased innovation.69 Moreover, researchers from the USDA and Rutgers expect R&D expenditures to continue to slow as market concentration continues.70 Due to sluggish R&D, consolidation, and exclusionary practices, farmers are seeing a well-documented decline in choices when buying seeds.71

As discussed earlier in this report, corn and soybean farmers also face increased market concentration in their other inputs, including tractors and agricultural chemicals. Although American farmers work harder than ever, they are increasingly exploited by powerful corporate forces.

Case study: Hogs

Pork production is centered in the Midwest, which accounts for about two-thirds of all hog sales in the United States.72 Four of the top five hog-producing states are located in the American heartland: Iowa, Minnesota, Illinois, and Nebraska.73 Due to its recent structural transformation from a competitive cash market to one shaped by a handful of integrated processors, the pork industry has garnered the attention and concern of a growing number of advocacy organizations.

Hog production and processing look a lot like the broiler (chicken) industry today, notable for its highly concentrated processors and widespread use of contracts. In contrast to corn and soybean seed farmers, who face higher input prices, reduced quality, and fewer choices from the monopoly power of large companies, hog farmers face monopsony power—the ability of buyers to suppress the prices paid to producers. This not only holds down the prices that hog farmers get for their product, but affects the entire nature of their operations. The increase in concentration in meatpacking and proliferation of production contracts have put hog farmers in a financial bind similar to that of broiler producers—forcing them to take on burdensome debt, accept low prices derived from opaque formulas, and assume risky liabilities.74

Since 1985, the hog industry has grown much more concentrated, with the four-firm share of hog slaughter increasing from 33 percent to 65 percent in 2008.75 The DOJ has long failed to vigorously enforce antitrust laws in the hog industry. In 2007, the department greenlighted a merger between Smithfield Foods and Premium Standard Farms, which together operated three of the four packing plants in Virginia, North Carolina, and South Carolina, creating a local monopsony.76 Despite already high levels of concentration, the DOJ permitted the Brazil-headquartered meat processor JBS to purchase Cargill’s pork processing holdings in 2015, increasing JBS’s share of the market from 11.6 percent to more than 20 percent.77 Today, the four biggest pork integrators account for 66 percent of America’s hog slaughter.78

However, national concentration levels obscure regional markets that may be much more concentrated. Hog farmers face several constraints when finding prospective buyers. Namely, after hogs reach market weight, farmers have a limited time to sell before the hogs deteriorate in quality and gain or lose weight, reducing their value. Furthermore, hogs are expensive to ship. It costs about $300 to transport 200 hogs 100 miles, and each mile traveled means increased mortality, decreased quality, and weight loss.79 As a result, the market for live hogs is geographically very limited, and buyers have significant leverage over farmers desperate to sell a rapidly depreciating product. Focus on estimates of national concentration levels ignores the reality that hog farmers face highly concentrated regional markets for their products. For example, after JBS’ acquisition of Cargill’s pork processing operations, the Iowa Farmers Union projected that the top two firms would buy and slaughter 82 percent of Iowa hogs.80 In the case of hogs and other bulky, perishable commodities, national concentration measures provide inadequate estimates of market power.

In tandem with increasing packer concentration, the portion of hog production occurring under marketing and production contracts has also increased dramatically. In 2017, 63 percent of hogs were produced under contract—nearly double the share of hogs that were contracted in 1996 and 1997.81 The price formulas defined in these contracts are often based on spot market prices, although, as noted below, they are complex, opaque, and often do not give the farmer much if any chance to control—or sometimes even observe—the pricing process.82 Usually, the livestock raised is itself owned by the integrator while contracts require the farmer to make burdensome capital investments to meet integrator requirements.83 While integrators offer short-term contracts, the producer must make a long-term financial commitment to specialized livestock production, increasing the relative power of the integrator over the farmer.

Hog contracts, by design, grant processors power over family farms. The prices in these contracts, even though based in theory on spot market prices, are derived from complex formulas that are not made public, sometimes even to the hog farmer. Moreover, when farmers attempt to band together to bargain for more favorable contracts, they risk retaliation from large integrators, a phenomenon that is well-documented in the broiler industry. Rural sociologist Mary Hendrickson has written extensively about how contracts ensnare farmers in a web of dependency on powerful firms. Without meaningful alternative buyers or safeguards that protect growers from extractive contract terms, Hendrickson argues that contract farmers are faced with “structural unfairness that constrains their basic liberties of fairness.”84 This power differential is exacerbated as most farmers now have few local alternative packers.

Additionally, the growth of captive supply—hogs that are owned by the processor throughout their lives—and industry consolidation has considerably thinned the cash market for hogs, sparking concerns about the integrity of market prices as viable price signals and opening the door to the abuse of buyer power. In 2016, just 2 percent of hogs were sold on the cash market, where live hogs are sold in a public market for immediate delivery, compared with more than 60 percent in 1994.85 The rest of production is captive supply, either contracted to outside growers or fed on company-operated feed lots. Thin spot markets are more susceptible to price manipulation because the average reported price is more sensitive to any one transaction and to big buyers moving in and out of markets on a weekly basis.86

There is a sizable body of evidence that shows that pork packers are using their size to exert market power and suppress commodity prices. The most significant study was commissioned by GIPSA and conducted by RTI International.87 This study, which relied on price data unavailable to the public, found that spot market hog prices varied by as much as 40 percent, and the differences were not fully explained by transportation costs, region, and quality of the product. This variability suggests that these markets are not functioning competitively. In fact, RTI concluded that there was buyer power in live hog markets, though they could not determine whether this market power was derived from the use of contracts. However, RTI International found that an increase of 1 percent in captive supply was associated with a nearly 1 percent decrease in spot market hog prices—a large effect when taking into account the thin margins under which many hog producers operate.

While the literature on this subject is not unanimous, several experts have drawn similar conclusions about the competitiveness of hog markets.88 Economists Xiaoyong Zheng and Tomislav Vukina have also found direct evidence of oligopsony in spot markets for hogs that resulted in suppressed commodity prices.89 Others have suggested that thinning markets may no longer provide reliable, competitive prices.90 Research has found that increases in contracting have led to higher price volatility and lower spot market prices, directly suppressing prices by reducing the demand for hogs on the spot market more than the supply.91

Because contracted hog prices are often based on spot market prices, monopsony’s effect is likely felt broadly by all hog producers.92 The magnitude of this market power is hard to measure, but agricultural economists John Schroeter from Iowa State University and Azzeddine Azzam from the University of Nebraska estimated that 47 percent of the farm-to-wholesale price spreads for pork were rents captured by powerful processors.93 This rent capture means that farmers only receive a small fraction of the sales price that consumers pay at the supermarket. For example, when a customer purchases a pound of bacon for $4.33, only about 69 cents of that price goes to the hog farmer.94

The winners and losers in a concentrated food system

Sometimes, scale and vertical integration can realize new efficiencies for the consolidated firm. Contracted production and agribusiness concentration may, in some respects, produce real efficiencies. USDA researchers William McBride and Nigel Key estimated that due to management structure and technology, contracting in the hog sector improves producer output by about 20 percent.95 However, evidence suggests that gains in efficiency from consolidation come at the expense of family farms and the rural communities they sustain. McBride and Key acknowledge that “negative producer welfare effects (e.g., loss of autonomy) or costs to contracting (e.g., increased transaction costs) could offset the potential on-farm efficiency gains from contracting.”96 Moreover, efficiency gains enjoyed by market intermediaries such as processors need not be passed down to consumers if downstream markets are not competitive.

Tina Saitone and Richard Sexton, agricultural economists at UC Davis, best articulate the implications of the current structure of agriculture, writing: “Market intermediaries with rather modest amounts of market power can capture large shares of the economic surplus generated from a market … Thus, even modest market power cannot be ignored from a policy perspective due to its significant distributional impacts.”97 In an article written for the Kansas City Federal Reserve, Saitone and Sexton model farmer and consumer welfare under various degrees of market power and find that even a modest departure from a perfectly competitive market can result in a 30 percent decrease in farmer surplus.98 The increasing difference between the price paid to hog farmers and the wholesale price of pork is consistent with the hypothesis that processors are benefiting from market power (see Figure 6), in part at the expense of farmers’ livelihoods.

Some economists assert that profit-maximizing processors with monopsonistic market power over producers will refrain from exercising that power to the detriment of farmers. The short-run profit gained from suppressing prices that are paid to farmers may be outweighed by future costs incurred if contracted producers leave the market because they cannot turn a profit or even sustain their operations.99 However, firms still have an incentive to suppress farmer prices below a competitive level, keeping farmers’ incomes low, knowing that the farmer has incurred sunk costs to enter the sector and has few alternative packers nearby. Indeed, one hog farmer who attended a 2010 DOJ workshop noted that his premiums declined in tandem with increasing concentration.100

Buyer power and the growing concentration in agricultural input markets discussed above threaten farmers’ already thin profit margins. In 2017, 41.8 percent of midsize family farms—family farms with annual sales between $350,000 and $999,999—had an operating profit margin of less than 10 percent; the USDA considers a farm with a margin of 10 percent or less at high risk of financial problems.101 The rise in farm bankruptcies in recent years, with seven states hitting their highest rates of Chapter 12 filings in a decade, illustrate the precarious economic condition of America’s farmers today.102

All told, America lost nearly 5 percent of its farms from 2010 to 2017—101,520 farms in all.103 The loss of family farms over the past several decades has deeply wounded rural counties, 1 in 5 of which are economically dependent on farming.104 Decades of studies of the industrialization of farming demonstrate that family farms are associated with more economically vibrant communities, higher wages, and lower economic inequality.105 Rural communities still have not recovered fully from the 2008 recession; employment in nonmetro areas has seen one-third the growth of that of metro areas and has yet to reach pre-2008 levels.106 In 2017, the poverty rate in rural communities was 3.5 percent higher than in urban areas.107 Given the importance of farming to many struggling rural economies, the distributional impacts of concentration and vertical integration in the food system should not be dismissed.

The case studies laid out in this report suggest the presence of significant market power in at least two markets in the agriculture sector. As policymakers come together to address the economic hardships of farmers and their communities, they must examine the role that monopoly and monopsony power play in agriculture.

Recommendations

It is time to put in place policies to ensure that America’s farmers and ranchers can thrive. Since Upton Sinclair’s groundbreaking novel, The Jungle, sparked a historic FTC investigation into the meatpacking industry a century ago, leading to the passage of the Packers and Stockyards Act, federal policymakers have periodically taken up the fight for family farms.108 These efforts have been frustrated by industry pressure and court decisions that have eroded the protections afforded to farmers under current law.109 Today, the work of farmer advocates remains unfinished.

As family farms struggle to keep their operations running, policymakers, enforcers, and regulators must act swiftly to counter the trend of growing corporate power. Below, the Center for American Progress outlines a range of recommendations for restoring competition and leveling the playing field for family farms.

Restore competition to agriculture markets

Reviving strong antitrust enforcement across the agricultural sector is the starting point for protecting farmers. Here are several specific steps to start doing so:

Halt and cap concentration. Congress must stem the uncontrolled growth of agribusiness by enacting a moratorium on agribusiness mergers and mandating that antitrust agencies conduct a comprehensive evaluation of competition in the food supply chain. Sen. Cory Booker (D-NJ) and Rep. Mark Pocan (D-WI) have introduced a bill that would do just that.110

Congress should also pass legislation that establishes statutory caps on concentration above which mergers will not be permitted. Congress has passed similar legislation before—including the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 and Section 622 of the Dodd-Frank Wall Street Reform and Consumer Protection Act, which prohibited a merger or acquisition in the financial sector that would result in a market share in excess of 10 percent in, respectively, the deposit and the non-deposit lending markets.111 Riegle-Neal also established state-based caps on concentration, but these have weakened over time and need to be strengthened112

Strengthen structural presumptions. Antitrust agencies must maintain strong structural presumptions against further consolidation, as CAP discussed in its 2016 report, “Reviving Antitrust.”113 Strong structural guidelines on mergers provide clarity and uniformity in enforcement and reduce the risk of underenforcement. In recent years, the presumptions of the illegality of mergers in moderately or highly concentrated sectors have been weakened, as demonstrated by the approval of the Dow-DuPont and Bayer-Monsanto mergers.114

Heighten scrutiny of buyer power. The DOJ and the FTC must place far greater weight on the potential buyer power of a merged entity in relevant agricultural markets. In 2008, the DOJ blocked a merger between JBS and National Beef on the grounds that it would result in anti-competitive buyer power, but the subsequent approval of JBS’ acquisition of Cargill’s Midwestern pork packing operations illustrates that antitrust enforcers do not sufficiently evaluate buyer power.115

The DOJ and the FTC should place more emphasis on buyer concentration when reviewing proposed mergers. These calculations should be based on the number of firms buying in a regionally specific input market, known as a “captive draw area,” rather than broader retail markets in which those entities compete to sell their products. Antitrust enforcers should modify their merger guidelines so that buyer power raises stricter scrutiny at lower levels of concentration than those applied to seller mergers. While current FTC and DOJ merger guidelines apply the same concentration thresholds to analysis of buyer and seller power, monopsony literature suggests that buyer power occurs at much lower levels of concentration.116 Antitrust scholar Peter Carstensen writes that buyers with market shares as small as 15 percent may raise competition concerns.117

Ultimately, antitrust policy in the past four decades has placed a great deal of emphasis on preventing the perceived harms of overenforcement, resulting in extraordinary levels of concentration across the agricultural sector. Utilizing the stricter buyer power test as an additional structural presumption in mergers may be a useful tool, at least in agricultural markets, to cure underenforcement likely without negatively affecting economic efficiency or setting up a complex balancing test.

Deconcentrate market power. Antitrust agencies should go even further than simply preventing further concentration of already oligopolistic markets; they should also aim to deconcentrate market power in agriculture. They should start by reviewing the competitive impact of recent mergers, such as those of Dow-DuPont and Bayer-Monsanto. If they find evidence that these mergers resulted in higher seed or chemical prices or other indicia of anti-competitive outcomes, these mergers should be reversed. These agencies should also—individually or jointly—conduct in-depth studies that evaluate the competitiveness of all major agricultural input, commodity, and retail markets. Where they identify evidence that concentration in markets has contributed to decreased innovation; higher input prices; reduced quality or choice of inputs; manipulated commodity prices; suppressed earnings; extraordinary rents; or other indicia of anti-competitive outcomes, the DOJ and the FTC should pursue enforcement to the greatest extent possible, including by pursuing the breakup of large firms in concentrated markets and unraveling recently consummated mergers.118

Support new competitors. Congress should expand USDA programs that are specially designed to support the establishment of new service or value-added cooperatives and alternative competitors in highly concentrated markets. For example, Congress should seek to increase funding to the Value Added Producer Grant program, which assists farmers and ranchers that wish to expand their operations by processing and marketing their goods themselves.119 The U.S. Department of Defense, the Department of Education, and other large federal and state government procurement entities should explore how they can support new competitors through government procurement and consider competition issues when purchasing food.

Guarantee a fair share for farmers and ranchers

Fair share pricing. Historically, spot markets have been central to farmers’ ability to earn a fair return—and, indeed, a middle-class living—as they gave farmers the ability to negotiate with multiple buyers for their best products.120 But as buyers have concentrated and contracting has become more prevalent, the health of these spot markets should be called into question. Many contracts continue to reference spot markets that are increasingly subject to abuse, to the detriment of the farmers seeking to earn a fair return. Given these challenges, spot market prices should only be permitted for contract grower pricing when sufficient liquidity is present and the competitiveness of the market is certified by the IFPB, discussed below.

Instead, alternative pricing models should be deployed that secure a fair share for farmers based on a percentage of the relevant wholesale or retail prices or, at a minimum, on a fixed dollar amount on the day the contract is signed. Pricing based on so-called tournaments—where farmers compete against neighbors and drive down farmer prices—should be prohibited. Some contracts, such as those used in the wine grape industry, already tie farmer prices to that of the consumer product.121

Farmer fair share boards. In the face of ever-growing market concentration, farmers and ranchers must be empowered to more effectively bargain to secure fair compensation and fair contract terms without fear of retaliation. Farmers’ rights to organize must be protected, including through bargaining cooperatives—the farmer’s equivalent of a union. To that end, Congress should reinvest in support of cooperative growth and expansion—including through technical assistance and capital expansion grants—and should strengthen penalties for any interference with or retaliation against the formation of a cooperative.

But Congress should go even further and pilot cutting-edge approaches such as sectoral bargaining, modeled after that which has been adopted in labor markets—for example, the market for domestic workers in Seattle.122 CAP has proposed expanding this arrangement to independent contractors broadly, and it could easily be modified to fit the agricultural sector. One way to do this could be to establish farmer fair share boards for each agricultural commodity and region. These boards could be made up of representatives from organizations representing farmers; farmworkers and adjacent agricultural workers; and processors. The IFPB, discussed below, could certify and oversee these boards as they set minimum prices or fee standards for farmers. The boards would ensure that prices paid for contracted commodities meet or exceed the costs of production and provide a fair return to farmers.123

Implement contract reform to protect farmer independence and rights

In addition to the pricing reforms noted above, high buyer concentration in agricultural markets that rely on contracted production means that Congress must enact commonsense guidelines that protect farmers from other aspects of abusive contracts and empower farmers to set their own terms.

Prohibit unfair, deceptive, and abusive terms in contracts. Production contracts can be so comprehensive that they turn nominally independent farmers into affiliates of the processor. That is, the processor has so much control over the producer that the producer ceases to be an independent business. Indeed, the Small Business Administration (SBA) has recently concluded that farmers in these circumstances are not independent businesses.124 Under these circumstances, even though the contract controls how the farmer conforms to environmental standards, the economic consequences of violations are borne by individual farmers and the public. Instead, Congress or the IFPB should ensure that processors are held jointly responsible for violations of public policy—such as environmental pollution, workplace safety, and health and food safety standards—by their contractors.

Moreover, the unequal bargaining power of small farmers and large processors—together with opacity of payment terms in producer contracts, the ability of processors to alter payments and other terms under those contracts, and the potential for changes in terms or outright cancellation to result in default on loans required to finance mandated capital investment—should make the worst of these contracts unconscionable and unenforceable.125 The IFPB, discussed below, should investigate and regulate or ban many of these practices. Processors should also have to enter into risk-sharing arrangements and guarantees with farmers for any mandated investments by the farmer.

Transparency. Even when the most egregious abuses are removed from contracts, farmers still must be empowered to review their contracts, share them with others, and understand them fully before signing. To that end, contracts must be written in clear language and must disclose costs and fees for feed, fertilizer, pesticides, pharmaceuticals, and other integrator-delivered or specified inputs. Integrators should be prohibited from preventing farmers from sharing the details of the contract with advisers of their choosing and must be required to provide farmers ample time to consider their offer before signing a contract. Pricing formulas and pricing determinations at the time of slaughter must be transparent. Forms of contracts should be filed with the IFPB and made publicly available. The IFPB should also conduct consumer testing of the contract language and provide model language for farmers to utilize.

Discrimination and retaliation. Congress should codify the proposed 2010 GIPSA rules that clarified what constitutes illegal differential treatment of two similar growers in pay or terms of contract. This rule would guarantee that growers with similar outputs are offered the same terms, premiums, and information.126 It would also prevent integrators from withholding or canceling the delivery of livestock to farms without notice or the discriminatory provision of inputs. This provision is crucial to protect farmers from retaliation and prevent packers from suppressing prices for growers in more concentrated regional markets while offering pay at more competitive rates to growers in others.127

Enforcement. Contract reform must restore the effective ability for farmers to sue under the P&S Act. In particular, farmers who sue for violations of the act should not be required to show competitive harm from the illegal practice—a burden of proof that is nearly insurmountable for most farmers and ranchers and that, in practice allows courts to second-guess the determination of Congress regarding what rights farmers enjoy.128 Furthermore, Congress should prohibit the use of forced arbitration clauses to bar farmers from seeking justice in court.

Create an Independent Farmer Protection Bureau

To implement and enforce many of the provisions outlined above, Congress should create an independent agency within the USDA that is dedicated to maintaining competitive agricultural markets and protecting family farmers—free from the capture and corruption that large agribusiness has often been able to work upon the broader USDA. Modeled after the Consumer Financial Protection Bureau (CFPB), which was founded to protect consumers from the predatory practices that helped create the 2008 financial crisis, this Independent Farmer Protection Bureau would be led by a five-year presidential appointee subject to Senate confirmation and would have its own dedicated funding stream paid for by a modest fee on the largest agribusinesses. It would succeed GIPSA, but have expanded authorities, stronger independence, and heightened status.

The IFPB would be the primary oversight and investigatory body of the federal government dedicated to American farmers’ economic independence and competitive welfare. Expanding on current mandatory price reporting requirements, it would monitor agricultural markets by collecting, analyzing, and publishing a wide range of data in support of family farmers and competitive markets. Using this data, the IPFB would support the competitive functioning of markets, including by certifying when spot markets are adequately competitive. Like the CFPB, it would establish a public hotline and complaint database for farmers to report anti-competitive practices.129 The data collected by the IFPB would also be used to inform the DOJ and FTC’s evaluation of proposed mergers and acquisitions in relevant markets.

The IFPB should have the authority to enforce laws passed to protect farmers from the abuse of market power such as the P&S Act, as well as its own new authority to combat unfair, deceptive, or abusive practices. The IFPB would also have backup authority in addition to the DOJ—and as relevant, the FTC—in areas such as retail to review and stop merger proposals, as well as enforce all relevant antitrust laws. This authority would overlap with, but not diminish, the authority and responsibility of other antitrust agencies to enforce antitrust law.

The IFPB should also have the mandate to combat anti-competitive practices on the input side. Granting it mandatory licensing authority or pricing authority could be deployed to support competitive choice among inputs.130 Similarly, it should have the authority to ensure farmers’ “right to repair” their tractors.131 Moreover, the IFPB should have supplemental truth-in-labeling authorities beyond those of the FTC to protect farmers against products labeled “USA Beef” even though they are made primarily from imported meat. It should also have the authority to certify and label products that meet farmer compensation and labor standards so that consumers may make informed choices at the grocery store.

The IFPB should have regional offices in major agricultural centers across the United States that can work with state attorneys general and local agriculture commissioners to protect independent farmers. It should also have designated offices to support farmers who are veterans, women, young people, people of color, people with disabilities, LGBT individuals, and immigrants. It should also be staffed with a technical office that can support farmers across the country who seek to organize for the purpose of collective bargaining or file suit against a firm that violated federal or state competition law.

Conclusion

Family farmers who have suffered from stagnant earnings for the past two decades are increasingly imperiled by the rise of powerful agribusiness firms. As agricultural input companies, processors, and marketers grow more concentrated, small family farmers face increased costs and suppressed commodity prices. If this market power remains unchecked, America may lose the last of its family farms, dealing a deadly blow to agriculture-dependent rural communities.

Policy reforms that halt the trend of increasing firm concentration, nurture competitive markets, and implement and enforce commonsense protections for family farms are essential to restoring a healthy food system and bolstering the middle class in rural America.

About the authors

Caius Z. Willingham is a research assistant for Economic Policy at the Center for American Progress.

Andy Green is the managing director for Economic Policy at the Center.

Acknowledgements

The authors would like to extend a special thanks to Dudley Butler, Peter Carstensen, Austin Frerick, Mary Hendrickson, John Ikerd, Marc Jarsulic, Jesse Lee, Dennis Olson, C. Robert Taylor, and many others for their contributions to this report.

Willingham previously published under the name Zoe Willingham.