Climate change will negatively affect every aspect of life and economic production. According to the Intergovernmental Panel on Climate Change, global temperatures have already risen by 1 degree Celsius compared to preindustrial levels.1 In the absence of aggressive and sustained reduction of greenhouse gas emissions, global temperatures will very likely hit and surpass 1.5 degrees Celsius by as early as 2030.2 Higher global average temperatures will cause more devastating storms, floods, and fires as well as rising sea levels.

For many years, climate economists have focused on how the effects of climate change will reduce gross domestic product as well as the earnings of firms directly tied to the production and heavy use of fossil fuels, including the oil, power, and chemical sectors. More recently, researchers have turned their attention to systemically important financial institutions and capital markets, which underpin every aspect of the economy.

Climate change has the potential to have a large impact on the normal functioning of the financial system. Financial markets rely on participants’ belief that the prices of debt and equity securities and other financial products more or less approximate the underlying real economy and its risks. When a natural disaster, pandemic, or other economic shock reveals a large gap between actual risk and asset prices, markets can experience severe volatility. When investors do not understand what is happening in a particular market, they withdraw their capital and look for safe havens. Stated differently, capital markets rely on steady investor demand to provide liquidity. Investor demand in turn relies on accurate pricing. Accurate pricing relies in turn on effective risk assessment. And effective risk assessment relies in turn on transparency and comprehensive disclosures.

Providing accurate and effective assessments of climate risk is critical for maintaining stable financial systems, but are state and local government municipal bond issuers providing potential investors with accurate and comprehensive climate risk disclosures?

While no comprehensive data exist, evidence suggests that climate disclosures in state and local government municipal bonds are a relatively new occurrence, with many issuers including minimal details about how climate could negatively affect an issuer’s ability to make bond payments over time.3 This issue brief uses a recent revenue bond issuance by the Miami-Dade Water and Sewer Department (WASD) to highlight the shortcomings of limited disclosures.4

Climate change is an unprecedented global reality that will require reform in every aspect of the economy, including public finance. Federal regulations should require state and local issuers to provide investors with robust climate risk disclosures. Comprehensive disclosure of climate risk will help ensure that the municipal market continues to enjoy accurate risk-based pricing and a high degree of liquidity.

Importance of the municipal market

The municipal bond market is the mechanism by which state, local, and special purpose governmental entities borrow money to finance capital projects and ongoing operations. According to the Municipal Securities Rulemaking Board, roughly two-thirds of all infrastructure projects rely on municipal bond financing.5 The municipal bond market is large. Currently, there is more than $4.1 trillion in outstanding issuances.6 Without access to capital markets, state and local governments would not be able to provide basic services or build the infrastructure that facilitates economic growth over time.7 Therefore, it is essential that the municipal market continue to function well.

These securities also provide an important option for investors. Nearly two-thirds of all municipal securities are held by individuals either directly or through mutual funds.8 Municipal securities are attractive to investors for two reasons. First, investors are not required to pay federal or state income taxes on the interest income provided by the bonds. Second, municipal bonds have a very low default rate. According to data from the Municipal Securities Rulemaking Board, muni bonds have a default rate of just 0.18 percent, compared with 1.74 percent for equivalently rated corporate debt securities.9

To function well, the muni market requires accurate risk-based pricing to ensure steady investor demand—i.e., no shortage of liquidity—and low volatility. In the absence of comprehensive and accurate climate disclosures, state and local governments may have trouble finding buyers for future issuances or be forced to pay substantially higher interest rates to attract the same level of investor demand. Additionally, if investors do not feel that they can effectively differentiate issuances that face a high degree of climate risk from those with a lower risk profile, they may demand a risk premium across the entire asset class. A uniform risk premium would penalize issuers with lower-risk securities.

Unfortunately, many state and local issuers either do not include any climate risk disclosures or provide only a cursory reference to climate change without meaningful detail. Moreover, there is no affirmative federal regulatory requirement that issuers include a specific climate disclosure.

Muni bond revenue pledges

Every loan involves the risk of nonrepayment. Specifically, creditors—the individuals and institutions that purchase municipal bonds—take on the risk that the state or local government debtor will fail to collect sufficient tax or fee revenue to make bond payments. Many factors can negatively affect tax and fee collections, including acute events such as natural disasters and epidemics, as well as broader structural pressures such as a recession or sea level rise.10

There are two broad categories of municipal bond: general obligation and revenue. General obligation bonds are backed by the full faith and credit of the issuing jurisdiction. This simply means that the state or local government pledges to use its power of taxation to collect enough revenue to make bond payments. For instance, a recent general obligation bond issued by Miami-Dade County for ongoing health facilities and services states, “The full faith, credit and taxing power of the County are irrevocably pledged to the prompt payment of both principal of and interest on the Bonds.”11

Revenue bonds are backed by a specific source of tax or user fee revenue. For instance, the offering documents for the most recent Miami-Dade Water and Sewer Department bonds states, “The payment of principal of and interest on the Series 2019 Bonds is secured by a pledge of and lien on the Net Operating Revenues of the Utility (the ‘Pledged Revenues’).”12 According to the offering documents, operating revenues are defined as “user charges for the provision of water service and sewer service, meter installation fees, and the like, delinquent charges and investment earnings.”13 If the department’s user fee revenues are insufficient to make bond payments, investors would have no recourse to any other tax or user fee revenues collected by Miami-Dade County.

Investors typically consider general obligation bonds lower risk than revenue bonds. The perception of risk comes down to taxing authority. WASD only has the power to raise user fees on the drinking water and wastewater services it provides customers, whereas Miami-Dade County has broad powers of taxation, including over real property and sales transactions, among others.

Another way to think about the issue is that each type of revenue pledge is more or less vulnerable to different types of external shock. For example, Miami-Dade County collects a 6 percent hotel occupancy tax, but discretionary consumer expenditures such as vacations involving a hotel stay are highly sensitive to economic conditions.14 Even a modest downturn can hit hotel tax collections hard. Other revenue pledges—such as tolls on a highway bridge—tend to be more durable because commuting and daily mobility needs do not change as rapidly.15 Conversely, a severe storm that causes the shuttering of a toll bridge for structural repairs may result in investor losses, whereas the surrounding county may recover more quickly with comparatively less disruption to sales or property tax collections.

The unique characteristics of each municipal bond issuance—including the source of taxes or fees to service the debt for revenue pledges—should drive the specific content of climate risk disclosures.

2019 bonds and revenue risk

South Florida faces significant climate change risks, including from acute shocks such as hurricanes as well as long-term structural pressures including rising sea levels. These stresses combined with the unique geology of the region will increase the cost of providing drinking water and wastewater services. Moreover, the complex politics of climate change mean that investors should not assume that Washington will always provide robust disaster aid. Taken together, these factors increase the risk of investor losses and should be disclosed in muni bond offering documents.

WASD is an enterprise unit of Miami-Dade County. The department functions as a separate business unit within Miami-Dade County. WASD’s business is proving commercial and residential customers with drinking water and wastewater services. This means that its finances are functionally separate from the county at large.16

Each year, WASD publishes an audited financial statement by an independent auditing firm in accordance with the accounting standards established by the Governmental Accounting Standards Board. The department owns and operates 8,700 miles of underground drinking water lines and 7,300 miles of sewer lines, among other assets. These facilities provide service to approximately 2.3 million residents each day.17 According to WASD’s 2018 financial statement, the most recent year for which information is available, the department collected $323 million and $388 million in drinking water and wastewater user fees, respectively.18 The department has $2.7 billion in outstanding long-term debt.19 For fiscal year 2019, the department budgeted $545 million in capital expenditures.20

In October 2019, WASD issued $233 million in revenue bonds to finance a portion of its long-term capital improvements program. (The brief refers to these as 2019 bonds).21 The capital program makes upgrades to both drinking water and wastewater projects and includes a mixture of standard maintenance and replacement of aging facilities, improvements to comply with health and environmental regulations, and upgrades to reduce energy consumption and better withstand the impacts of climate change.

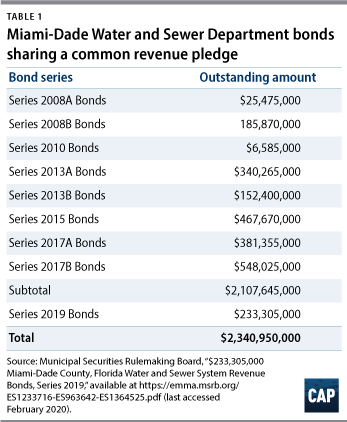

The revenue source pledged to repay investors is the user fees the department charges commercial and residential customers for drinking water and wastewater services. Importantly, this same revenue source is also pledged to eight previous municipal bond issuances made by WASD since 2008, which have a total outstanding value of $2.1 billion.22 The 2019 bonds are “on parity as to source and security for payment with the Outstanding Bonds.”23 The investors who purchased the 2019 bonds have an equal claim to the user fee revenues as all the other investors in the previously issued debt.

The 2019 bonds received an investment grade rating with a stable outlook from three national rating organizations. S&P rated the bonds AA-, Moody’s rated them Aa3, and Fitch gave the bonds A+.24 Part of the reason for this rating is that the 2019 bonds come with a rate covenant and a reserve account. A rate covenant is a promise to investors that the department will continue to charge user fee rates for drinking water and wastewater services that are equal to “one hundred twenty five percent (125%) of the Principal and Interest Requirements on the Bonds.”25 Moreover, WASD promised to charge rates that cover “one hundred percent (100%) of the required deposits into the Reserve Account.”26

The reserve account must be capitalized with enough money to make all principal and interest payments for one full fiscal year on all the bonds that share the save user fee revenue pledge.27 According to the offering documents, the reserve account will include cash and insurance policies equal to $189.7 million.28 It’s important to note that WASD’s user fee revenues must cover ongoing operating expenses in addition to servicing debt obligations.

Based on historical data, the rate covenant and reserve account should provide a financial cushion capable of protecting investors against an unexpected downturn in WASD revenues over the life of the bonds. Yet climate change represents a decisive break from historical patterns, placing a large question mark over the adequacy of WASD’s reserve account specifically and rating agency standards generally.

Catastrophic event

The recent history of the Puerto Rico Aqueducts and Sewers Authority (PRASA) demonstrates how catastrophic storms can lead to unprecedented asset destruction and revenue losses. In early September 2017, Hurricane Irma—one of the most powerful storms every recorded in the Atlantic—passed by Puerto Rico, unleashing torrential rains and harsh winds. The storm killed three people and left nearly 70 percent of the island without power.29 Not even two weeks later, Hurricane Maria hit the island, knocking out the rest of the power grid and causing even more devastation.30

The two storms caused catastrophic damage to PRASA’s infrastructure and caused a severe drop in revenues. The financial tumult continues. In fact, PRASA’s most recent audited financial statement ends on June 30, 2017, prior to the hurricanes.31 Ongoing disclosures tied to PRASA muni bonds provide a window into the volatility of the authority’s financial situation.

In April 2018, as part of a potential restructuring of its outstanding debt, the authority released some financial estimates. According to PRASA, the storms resulted in the suspension of meter readings for 60 days from September 16, 2017, to November 16, 2017.32 During this time, PRASA lost $271 million in water revenues.33 The authority states, “For FY2018, revenues are expected to be substantially lower than budgeted due to, among other things, population migration, decline in economic activity and lower consumption for the period when clients did not have service and lower collections rate.”34 To compound matters, PRASA notes that many water clients are eligible for “a deficient service credit.”35

PRASA also estimates incremental costs associated with storm response of $396 million and capital repairs of $769 million, for a total cost of $1.4 billion.36 Importantly, this estimate excludes additional capital projects that would improve system resilience to future storms. When resilience improvements are added to the plan, the total cost jumps to $4.8 billion.37 To put this number in perspective, it is equivalent to all outstanding bonds and notes payable that PRASA reported in its financial statement issued prior to the two hurricanes.38

PRASA’s recent experience is a powerful reminder that water authorities face the threat of lost revenues from both demand- and supply-side disruptions. When a storm or other disaster damages water assets and interrupts service, a water authority cannot deliver potable water or treat wastewater. The disruption of drinking water and wastewater supply leads to reduced billings. Water authorities also carry revenue risk from a reduction in demand. For instance, if a storm leaves water infrastructure in tact but causes severe damage to homes and businesses, the authority can experience lost revenue. This threat is not limited to island communities such as Puerto Rico.

According to data from the Insurance Information Institute, Hurricane Andrew in 1992 left approximately 250,000 people homeless in Miami-Dade County. Moreover, roughly 25,500 homes were destroyed and another 100,000 were damaged.39 Climate change increases the likelihood that Miami-Dade and WASD will experience another storm like hurricanes Andrew, Irma, or Maria.

Rising long-term costs

Beyond acute shocks such as hurricanes, WASD faces significant long-term costs tied to climate adaptation. As part of its 20-year planning process for drinking water services, WASD notes, “Climate change and sea level rise are expected to present significant challenges relating to water resource planning.”40 The largest risk is from “salt water intrusion into the freshwater Biscayne aquifer,” which provides drinking water for the region.41

The freshwater Biscayne aquifer is primarily made up of “highly porous and transmissive” limestone,42 which is exposed to saltwater intrusion at the coastal margins.43 The zone where the freshwater and saltwater meet is referred to as the “salt front” or the “freshwater saltwater interface.”44

Shifting demographics, rising seas, and seasonal changes all affect saltwater intrusion. Under normal conditions, freshwater percolates into the aquifer and saturates the porous limestone, creating outward pressure that keeps saltwater from seeping in. But as the population of South Florida grows, it increases demand for freshwater, which WASD meets by pumping water out of the aquifer. This creates an opening for saltwater to intrude. The problem is especially acute during the dry season, when there is less recharge of the aquifer.

Additionally, WASD and the U.S. Geological Survey estimate sea level rise of between 9 inches and 24 inches by 2060.45 When the county modeled the effects of seal level rise, it found that, “Increased sea level resulted in landward migration of the freshwater-seawater interface.”46 This results in an increased concentration of chloride in the aquifer, which WASD must treat or otherwise resort to finding an alternative freshwater source—both of which come with a large price tag.

The hydrological challenges for the region don’t stop with saltwater intrusion. The county found that rising groundwater levels increase the risk of flooding during major rain storms: “rising groundwater … reduce[s] soil storage and discharge capacity, with increased potential for both inland and coastal flooding.”47 South Florida also has an extensive network of canals that help with storm drainage. As sea levels rise, “the canals are not able to drain as quickly and … there is less capacity for managing the hydrologic system.”48 In the future, WASD will likely have to shoulder additional capital costs to combat the risk of flooding, adding to its debt burden and potentially increasing the risk of default.

Managing these challenges and adapting to climate change will add to WASD’s operating and capital costs. Yet the 2019 bond documents make no mention of saltwater intrusion and only mention sea level rise twice without connecting the threat to authority revenues.

Political risk

Another investor risk factor that issuers overlook is political risk. State and local issuers benefit from the fact that the federal government has historically acted as a financial backstop. When catastrophic storms hit local communities, the federal government typically steps in with financial aid to rebuild broken infrastructure and catalyze the return of normal economic activity. This de facto federal guarantee reduces the risk of investor losses.

This guarantee may not last for two reasons. First, the rise of political polarization means that disaster aid presents an attractive lever to extract votes or damage political opponents. Second, as climate change brings about more frequent and severe storms, public support for costly bailouts may weaken. Puerto Rico serves as a powerful example of political risk.

In its April 2018 bond disclosure documents, PRASA anticipated that a substantial portion of the $396 million in incremental costs and $769 million in repair costs will be covered by insurance policies and federal disaster assistance grants.49 However, according to The Washington Post, the Trump administration has continued to withhold disaster aid: “The U.S. territory is still waiting on billions of dollars approved by Congress for recovery from Hurricane Maria more than two years ago, though the administration recently agreed to release some of the money subject to several conditions.”50 Given the important role of emergency aid following acute shocks such as hurricanes and other natural disasters, bond-offering documents should similarly include a disclosure about the political risks of assuming that Washington will always provide sufficient disaster relief.

Bond prices

To date, capital markets have not systematically priced climate risk into municipal bonds.51 This is expected to change relatively soon. An analysis by BlackRock Investment Institute found that state and local governments that have collectively issued 15 percent of outstanding muni bonds—roughly $615 billion—will face climate impacts that could meaningfully reduce economic output.52 For instance, BlackRock estimates that annual hurricane damage could cost South Florida an equivalent of 2.5 percent of local gross domestic product. Data from the Federal Reserve show that 2.5 percent of Miami-Dade County’s current economic output is equivalent to $4.1 billion.53

This may not seem like much but consider that the reduced economic activity predicted by BlackRock will take place within a context of rising costs. Population growth in South Florida will require WASD to expand its facilities, and inflation will drive up the cost of materials and labor. Additionally, more stringent public health and environmental regulations will increase both capital and operations costs even as WASD will need to expand its capital program to include ever larger and more expensive climate adaptation projects. Meanwhile, capital markets may begin demanding a climate risk premium on newly issued bonds. Rising costs and reduced economic activity have the potential to become a negative feedback loop, placing serious fiscal strain on WASD.

By providing investors with robust and—to the greatest extent possible—quantitative climate disclosures, WASD will help capital markets price their future debt appropriately. In the absence of a meaningful disclosure, WASD runs the risk that the market will lump its securities in with all coastal water authorities regardless of the underlying climate risk fundamentals. If WASD and Miami-Dade County have taken aggressive adaptation measures that meaningfully reduce climate risks, they should be rewarded by the market with access to cheaper debt. In the absence of issuer risk differentiation, WASD would be forced to pay an unnecessary premium—the market’s version of socializing expected losses.54

Material events

Municipal bond issuances are regulated by the U.S. Securities and Exchange Commission (SEC). In general, issuers are required to disclose information to potential investors that allows for “an informed investment decision.”55 Each muni bond will provide investors with different information depending on the issuer and the nature of the bond. For instance, a general obligation bond issued by a state to finance ongoing operations and backed by income or other general tax collections will contain substantially different information than a private activity bond for an infrastructure project that uses a public-private partnership procurement model that is backed exclusively by user fee revenues.

Regardless of these differences, all muni issuers must avoid making material misstatements or omissions in their offering documents to prospective investors. According to the SEC, a misstatement or an omission is considered material if “the magnitude of the item is such that it is probable that the judgment of a reasonable person relying upon the report would have been changed or influenced by the inclusion or correction of the item.”56 Misspelling the name of the financial advising firm that provided consulting services to the issuer would not be material. By comparison, omitting major outstanding governmental debts or overstating tax revenues would be material.

Going forward, failing to disclose detailed climate change risks should be considered a material omission. Both acute events such as wildfires, floods, and hurricanes as well as structural changes such as rising sea levels will negatively affect governmental revenues and increase the likelihood of investor losses. Moreover, mitigating and adapting to climate pressures will add substantial capital and operational costs to the continued provision of essential governmental services.

Comprehensive disclosure

WASD’s 2019 bonds include a limited climate disclosure that provides a simple qualitative recognition that climate change may produce “negative economic impacts.”57 The disclosure also mentions in general terms the department’s efforts at sustainability and implementation of climate-related “policies and initiatives,” with a link to Miami-Dade County’s climate change strategy known as GreenPrint—a neologism intended to convey the sustainability of the region’s footprint—and a link to the Southeast Florida Regional Climate Change Compact.

The official statement for the 2019 bonds includes the following climate disclosure language:58

The State of Florida is naturally susceptible to the effects of extreme weather events and natural disasters including floods, droughts, and hurricanes, which could result in negative economic impacts on coastal communities like the County. Such effects can be exacerbated by a longer-term shift in the climate over several decades (commonly referred to as climate change), including increasing global temperatures and rising sea levels.

The County is addressing the threat of climate change in the following ways: (1) implementing new policies and initiatives, including environmental protections, sustainability measures, and energy and water conservation; and (2) completing a systematic assessment of the future vulnerability of the most critical County-owned infrastructure and using that information to direct investment into protective measures for the County’s most exposed assets. The County’s climate change strategy is outlined in the GreenPrint link on the County’s website59 … and in the Southeast Florida Regional Climate Change Compact’s (the “Compact”) Regional Climate Action Plan60 … For planning purposes the County relies upon the Compact’s Unified Sea Level Rise Projection for Southeast Florida.

The GreenPrint strategy is an admirable undertaking—especially considering the hostility toward climate science emanating from Tallahassee—that lays out ideas and goals for producing a new generation of climate leaders, creating green jobs as part of a vibrant economy, educating the public about climate change, supporting sustainable land use, and reducing energy and water use, among other areas.61

The last goal is particularly relevant to WASD since water utilities are major energy consumers, which makes drinking water and wastewater services a major source of greenhouse gas emissions. In fact, the department is Florida Power & Light’s largest customer in South Florida.62 As part of its long-term capital program, WASD is making investments to improve energy efficiency.63 These improvements will both lower the department’s operating costs and help the county meet its emissions goals.64

Unfortunately, this deeply laudable and necessary effort at environmental stewardship does not obviate the need to provide potential investors with robust climate risk information. WASD’s minimalist disclosure and reference to the GreenPrint plan do not address the fundamental question of how climate change risks could lead to investor losses over time.

Similarly, the disclosure links to the plans and goals established by the Southeast Florida Regional Climate Change Compact. The compact lays out goals across a number of areas, including agriculture, energy and water use, natural systems, and social equity, among others. The section on water includes 21 goals. These range from very high-level, aspirational goals such as “Foster innovation, development, and exchange of ideas for managing water” to somewhat more specific goals such as “Advance capital projects to achieve resilience in water infrastructure.”65 As with the GreenPrint goals, this information is not specific enough to the assets and revenues of WASD to meaningfully inform the decisions of potential investors.

Both the GreenPrint and compact plans demonstrate that the threat of climate change has penetrated the consciousness of regional elected officials, planners, and civic leaders. This is immensely important since climate change is the greatest collective action problem the world has ever encountered. These plans provide a meaningful indication that regional leaders are pulling in roughly the same sustainability direction. However, these plans do not make up for the inadequacy of the climate disclosure included within the 2019 bond-offering documents.

An effective and comprehensive disclosure should provide a clear explanation and quantitative estimates of how both acute shocks and long-term climate changes could reduce issuer revenues or lead to higher operating and capital costs. Above all, a climate disclosure must be forward-looking. Typically, bond documents provide historical information. The 2019 bonds include, as an appendix, WASD’s most recent certified financial statement. The statement allows a potential investor to understand the basics of WASD’s revenue model, annual expenses, outstanding debt, and other core financial statistics. Yet historical financial performance does not provide much value for assessing future risk since climate change represents a fundamental break with the past.

A better approach would be for the state or local issuer to present multiple risk-based revenue scenarios. Climate models typically output a range of estimates for things such as sea level rise, drought cycles, and storm severity. A scenario analysis would look at how a range of potential shocks could reduce revenues. The analysis could answer a question such as: How long of a disruption in billing would be required to exhaust the bond reserve account? As part of the analysis, WASD could provide data on revenue losses stemming from Hurricane Andrew and crosswalk that with predictive storm models.

In addition, a scenario analysis could determine how much additional borrowing backed by the same revenue pledge would be needed if 10, 20, or 30 percent of authority assets needed replacement following a major storm. With respect to long-term costs tied to climate adaptation, a scenario analysis could look at the costs associated with different saltwater intrusion assumptions. This could answer questions including: At what point would saltwater intrusion require WASD to develop alternative freshwater sources? What would the estimated capital outlay be for either sourcing freshwater from other parts of the state or engaging in large-scale desalinization?

For additional information on how to respond to the threat of climate change in an equitable manner, read the following Center for American Progress reports:

- “A Framework for Local Action on Climate Change: 9 Ways Mayors Can Build Resilient and Just Cities”66

- “Safe, Strong, and Just Rebuilding After Hurricanes Harvey, Irma, and Maria: A Policy Road Map for Congress”67

These are only a few of the questions and analyses that would provide potential investors with material information about climate-related risks. Each muni bond issuance is unique. This means that each issuance will need a slightly different set of quantitative scenario analyses. The point is that the current approach of including a simple qualitative statement recognizing climate change as an extant fact is insufficient. Investors already know this. What matters is how climate change will affect the ability of the issuer to service the debt security in question.

It is common for issuers to provide technical reports prepared by outside experts as part of muni bond offering documents. Moving to a disclosure regime that includes climate risk will require most issuers to engage with outside technical experts. State and local issuers should not bear the full cost of creating a new set of disclosure standards, since a well-functioning muni market provides significant benefits to the economy and society at large. For this reason, the U.S. Environmental Protection Agency and the SEC, working with other relevant agencies and regulators, should establish a clearing house for climate data and establish best analytical practices. Additionally, these agencies should provide direct technical assistance during the early years of implementing any new climate disclosure requirements.

Of course, federal financial support to state and local governments should not be limited to technical assistance for bond disclosures. Every state and local community faces complex trade-offs and costly projects to mitigate and adapt to climate change. Yet economic disparities that stem from persistent discrimination based on race and ethnicity mean that disadvantaged communities will have fewer resources to combat the climate crisis. Federal climate policy must recognize the legacy of discrimination and provide robust funding to those communities facing the greatest need. Otherwise, climate disclosures may result in a risk premium that raises the cost of financing for those communities that can least afford it.

Conclusion

To ensure the continued stability and liquidity of the muni bond market, federal regulations should require issuers to include comprehensive and, to the greatest extent possible, quantitative scenario-based climate risk disclosures. A robust disclosure requirement, applying to both the initial offering documents and ongoing disclosures as additional material information becomes available, will provide the transparency necessary for risk-based pricing. Climate risk transparency will allow investors to judge each issuance on its merits and avoid the uniform application of a risk premium in bond pricing. In short, a robust disclosure requirement will reward those state and local issuers that have taken the most aggressive mitigation and adaptation efforts with lower financing costs.

Kevin DeGood is the director of Infrastructure Policy at the Center for American Progress.