The United States is one of the few bright spots in a global economy that needs more of them. The U.S. economy is projected to grow 2.4 percent in 2016—faster than the United Kingdom at 1.9 percent, Germany at 1.5 percent, and Japan at 0.5 percent. Unemployment is low, inflation is barely present, and the housing market is on the mend.

But the most concerning aspect of the U.S. recovery—other than the unequal distribution of its gains—has been the sharp slowdown in productivity growth. Productivity grew a meager 0.9 percent in 2015 and actually fell in the first half of 2016.

Growth in productivity, or the amount of goods and services a worker produces in a given period of time, may be abstract, but it is the key to raising living standards. A precondition for the American Dream—children enjoying a better life than their parents—is for each new generation to also live in a more productive economy. Indeed, the main reason the United States in 2016 is a richer country than it was a century ago is that workers today can produce nine times as much in an hour as their counterparts in 1916.

The productivity slowdown and the missing $2.8 trillion

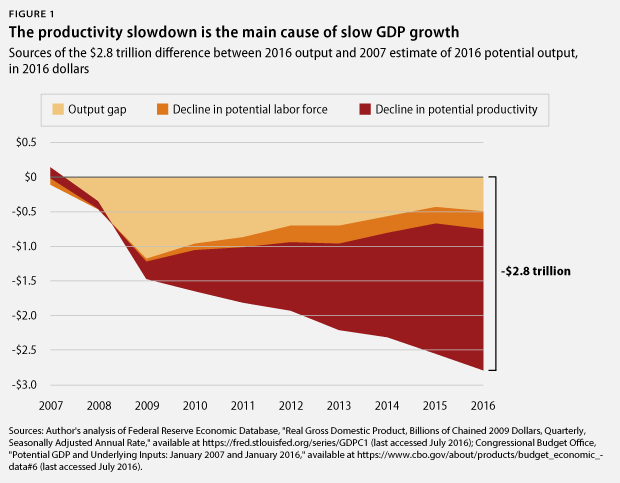

One way to see the consequences of the slowdown in productivity growth is to examine how it has reduced gross domestic product, or GDP, growth. Figure 1 compares the most recent estimate of 2016 GDP with the 2007 estimate of potential 2016 GDP by the Congressional Budget Office, or CBO. This provides an excellent yardstick for comparing where the economy is today against where forecasters thought it would be nine years ago.

The United States will produce about $2.8 trillion, or 13 percent, fewer goods and services in 2016 than the CBO thought it would be able to before the Great Recession. The difference amounts to $13,500 per working-age adult and illustrates just how slow the recovery has been relative to prerecession expectations.

We can unpack the $2.8 trillion in missing GDP into three parts: the gap between current and potential output, typically known as the output gap; lower-than-expected growth of the size of the potential labor force; and lower-than-expected growth of what the CBO calls “potential productivity,” or potential GDP divided by the size of the potential labor force. The bulk of the $2.8 trillion in missing GDP—$2 trillion, or 74 percent—has come from unexpectedly slow growth in potential productivity.

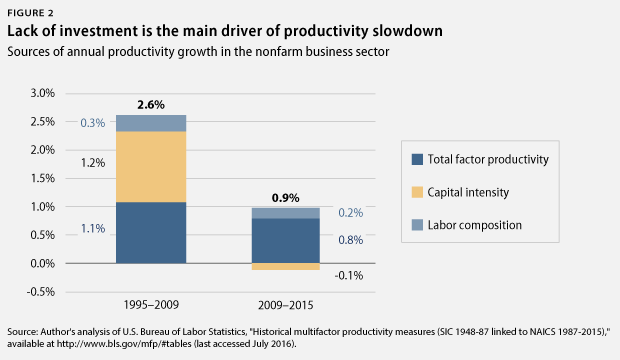

What is the main reason for slow productivity growth? There are three possible explanations: slow growth in workers’ human capital; slow growth in investment, known as capital intensity; and slow growth in the efficiency with which workers use capital, which is referred to as total factor productivity. Looking at actual productivity growth in the nonfarm business sector—as displayed in Figure 2—the principal problem is a lack of investment. Speeding up GDP growth will require faster productivity growth—which, in turn, will require more investment.

Tax cuts will not do the trick

One theory many politicians hold dear is that reducing the corporate tax rate is the key to raising productivity and investment. Unsurprisingly, some are using the recent slowdown in productivity as a justification for reducing corporate tax rates. Speaker of the House Paul Ryan’s (R-WI) recent tax plan, for example, cites “flat productivity” as a reason for cutting taxes on savings and investment, including the corporate income tax.

Conservative advocates for cutting corporate taxes frequently focus on the fact that the United States has the highest statutory corporate tax rate among advanced economies. But the statutory rate does not reflect the vast number of ways that corporations can reduce the actual taxes they pay as a share of profits, which is known as the average effective tax rate. The U.S. average effective tax rate is near the average among advanced economies, as is the marginal effective tax rate, the tax rate that corporations use to make investment decisions.

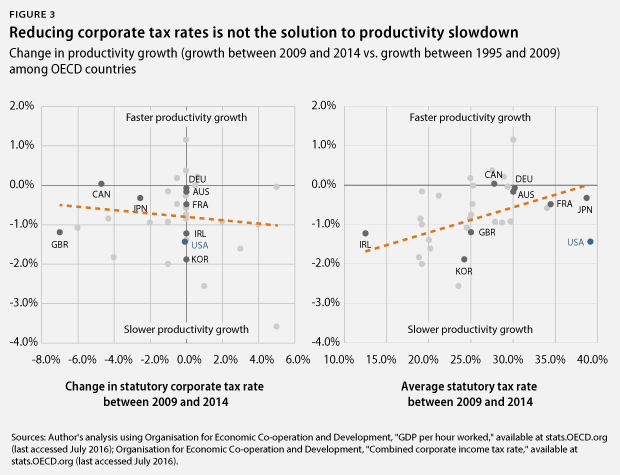

But there is no reason to think that the productivity slowdown has anything to do with statutory corporate tax rates. After all, advanced economies’ statutory corporate tax rates vary a great deal, and yet productivity growth has slowed in virtually every one of them. Figure 3 shows that advanced economies that have cut their statutory corporate tax rates also have experienced a slowdown in productivity growth: There is no statistically significant relationship between corporate tax cuts and the size of the productivity slowdown. And countries with lower statutory corporate tax rates actually have experienced a sharper productivity slowdown. Even Ireland—the poster child for low corporate tax rates—has seen its productivity slow at a rate similar to that of the United States.

While these graphs certainly do not prove that corporate tax cuts have no effect on productivity or investment, they do show that the productivity slowdown is also a problem in advanced economies with lower statutory corporate tax rates. Policymakers hoping to solve the productivity slowdown need to look beyond corporate tax rates for solutions.

Raising demand

A more promising way to raise investment is to raise aggregate demand. Businesses are unlikely to invest in new plants and equipment when they think a weak economy will translate into weak sales. International Monetary Fund and Organisation for Economic Co-operation and Development research using a traditional model of investment growth does indeed show that weak demand is the main reason for slow business investment growth in the United States. This suggests that policies that raise demand—such as low interest rates and increased infrastructure spending—will cause companies to raise investment as they expect stronger sales as a result of job and wage growth.

Has the window for raising demand already passed? If the economy is already operating at its potential, then more demand will only generate higher inflation instead of faster real economic growth. But if the economy is operating below potential, then raising demand is a relatively easy way to boost growth.

The gap between real gross domestic product and the CBO’s estimate of potential GDP has indeed declined, but correctly estimating the latter is clearly difficult: The CBO has, after all, revised its estimate of potential 2016 GDP by more than $2 trillion since 2007. A more reliable way for policymakers to gauge whether the economy is operating at its potential is to observe whether the real prices of labor and capital—wages and interest rates—are rising quickly, implying an economy that is approaching capacity. Yet real wages are growing less than 1 percent per year, and real interest rates are negative.

Relearning the lesson of the 1930s and 1940s

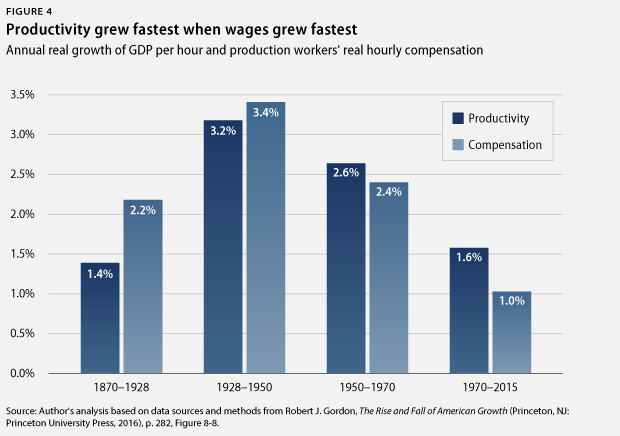

Another method for boosting productivity is offered by Northwestern University economist Robert Gordon—one of the country’s leading productivity experts—in his recent book The Rise and Fall of American Growth. Gordon describes the period between 1929 and 1950 as “the Great Leap Forward” for productivity, which grew an astounding 3.2 percent per year—far more than any era since 1870 and double the growth rate since 1970.

Gordon argues that a key reason productivity surged during this period was that rising real wages provided an incentive for firms to invest in capital, such as machinery. When labor is cheap, businesses have little incentive to invest in capital because they can always hire another worker on the cheap. But higher wages reduce the price of capital relative to labor, nudging firms to make investments and raise productivity.

The 1929–1950 increase in wages was at first a result of several policies that directly raised workers’ wages, including the first federal minimum wage, the first federal overtime law, and the National Labor Relations Act, which made it easier for workers to join a union and bargain with their employers. The entry of the United States into World War II further drove investment higher, as the economy converted into what Gordon describes as a “maximum production regime.”

It is striking that during this period of rapid productivity growth, wages for production workers grew even faster than productivity growth did. The current debate about whether a typical worker’s compensation has kept track with the economy’s productivity typically envisions productivity growth as the precondition for wage growth. But Gordon’s research implies that the relationship can go both ways: Not only can productivity growth raise wages, but higher real wages also can boost productivity growth—the main reason for slow gross domestic product growth—by giving firms a reason to purchase capital.

Can higher wages raise productivity growth in 2017? Basic economic theory and common sense suggests that an increase in the price of labor—wages—achieved through higher labor standards will cause firms to invest in more capital, raising the economy’s productivity.

Some have tried to use this fact to claim that raising wages ultimately will hurt workers by causing them to be replaced with machines. But automation is just another way of saying productivity growth: Robots replacing humans means more output produced using fewer human hours—the literal definition of higher productivity. We can either have a productivity problem or an automation problem, but we cannot have both at the same time.

The sharp slowdown in productivity growth today heavily implies that we currently have too little automation rather than too much. At the same time, the evidence on policies that raise wages—such as the minimum wage—points to no noticeable effect on employment. Indeed, the New Deal and its rising labor standards were also a period of rapid employment growth.

A more important question is whether we have enough of the other key ingredient for the productivity growth that made the 1930s possible: innovation. Technological change itself is another reason firms purchase new capital—otherwise, investment amounts to “stacking wooden ploughs on top of wooden ploughs.” Gordon makes clear that the 1930s were in fact one of the most innovative decades in history, as the economy began to harness the potential of the internal combustion engine and electrification. Firms ultimately could afford policies that raised wages because they could raise their productivity with new equipment featuring innovative technology.

There exists a vigorous debate today about whether we live in a period of very ordinary or extraordinary innovation. Some—such as Gordon himself—argue that productivity growth inevitably will be slower because today’s new technology is inherently less innovative than that of the 1930s. In that case, there still exists a strong justification for raising labor standards: Slow productivity growth makes it that much more important that its fruits be shared equitably.

But others—including Andrew McAfee and Erik Brynjolfsson of the Massachusetts Institute of Technology, the country’s leading growth optimists—argue that we live in a period of extraordinary technological change. Even so, recent innovations—such as 3-D printing and social media—have failed to raise productivity growth, even after accounting for the possible problems with how statistics measure it. Therefore, it may be the ability of firms to hire workers at wages that have barely grown since 2000—rather than purchasing new equipment and adopting new technology—that has prevented productivity from rising.

The truth likely falls somewhere in between the pessimists and the optimists, with healthy—if not necessarily explosive—productivity growth possible. In that case, policies that raise wages may be the key to unlocking productivity growth by increasing incentives for firms to invest in capital. Such wage-raising policies include making it easier for workers to bargain collectively, raising the federal minimum wage, and modernizing overtime rules. Fortunately, the Obama administration recently has taken action on the latter and proposed an increase in the overtime threshold to $47,000 per year.

Conclusion

The productivity and investment slowdown presents a direct threat to the growth of U.S. living standards. It is the main reason gross domestic product growth has slowed, and it is a challenge with which advanced economies across the world are grappling. Importantly, productivity has slowed regardless of countries’ corporate tax policies—some politicians’ favorite solution to every economic problem.

Policymakers should heed the advice of the International Monetary Fund and focus on attacking the main cause of the productivity slowdown—low aggregate demand. A substantial investment in infrastructure—as the Center for American Progress recently proposed—would go a long way toward getting business investment back on track.

An additional and complimentary avenue to raising productivity is policies that directly raise wages. Employers have little reason to invest in new capital and raise productivity when real wages are stagnant. When faced with higher labor costs, employers will invest and innovate—two of the keys to raising productivity.

Policymakers in the 1930s and 1940s turned the Great Depression and World War II into the most rapid growth in living standards our country has ever seen. Hopefully, their counterparts today can learn from their example.

Brendan V. Duke is the Associate Director for Economic Policy at the Center for American Progress.