The global collapse of tax revenues was one of the major challenges that policymakers confronted during the Great Recession. The Bush and Obama administrations both responded to recessions early in their terms by stimulating the economy. Governments typically counter the shortfall of demand that occurs during a recession by reducing taxes or increasing spending, an approach that former President John F. Kennedy once defended by asking, “Don’t you remember your Economics 101?”

Other governments, however, had made budget commitments that gave them less latitude in their fiscal policy approaches. Instead of stimulating the economy, they implemented austerity measures, including slashing spending and raising taxes in the face of the Great Recession.

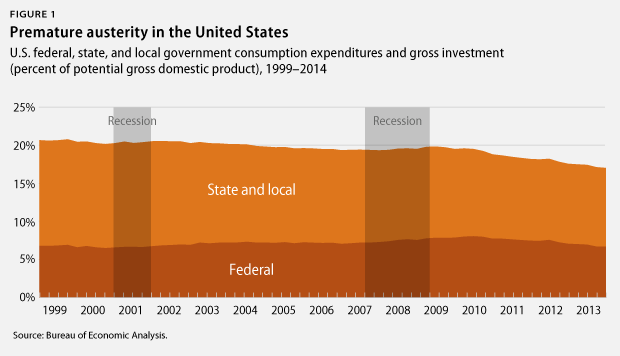

Most prominently, EU member states had their hands tied by fiscal goals they committed to as a condition of joining the European Economic and Monetary Union. Less prominently, state and local governments across the United States dutifully cut spending and raised taxes to meet balanced budget rules and ride out the recession.

In Washington, politicians were quick to distance themselves from the stimulus package; at the same time, most of the stimulus was negated by all of the forced austerity at the state level. By 2010, both American and European politicians of every major party were burnishing their austerity credentials.

Meanwhile, academic economists began to seriously revisit how to measure the effectiveness of fiscal stimulus for the first time in a generation. Researchers have devoted more attention to studying the effectiveness of fiscal policy in the wake of the Great Recession than at any other point in the past 50 years. Experts in the field have created richer datasets, more-precise measures of policy changes, and new theoretical and empirical techniques. Informed expert opinion has moved in the opposite direction from politicians in both parties: In academic departments across the United States, economists have come to the conclusion that stimulus is actually more powerful—and austerity more harmful—than even many stimulus proponents thought a decade ago. Economists have also significantly shifted their thinking about what happens to the U.S. economy after recessions, and many have come to the conclusion that failure to stimulate the economy and push out of recessions has irreversible, negative, long-term effects on the economy.

There are three major lessons for policymakers from this research:

- Direct government intervention during recessions, either through deficit-financed tax cuts or deficit-financed increases in government spending, is a more powerful tool for fighting recessions than we realized before the Great Recession.

- In a slack economy, or one that is operating below its potential, austerity—taking money out of the economy to balance government budgets—is especially bad policy. Whether via tax hikes or cuts in government spending, contracting the government’s budget during a recession reduces gross domestic product, or GDP, by more than the size of the cuts—possibly as much as three times more.

- The costs of doing nothing can be permanent and much higher than we previously thought: U.S. GDP is currently 10 percent below its prerecession 2014 projection, and many economists believe that we have reached a new normal. If this is true, austerity could cost the U.S. economy more than $1 trillion in economic activity every year, even after we have fully recovered from the Great Recession.

The most important development in economic research during this recession has been a better understanding of how short-term labor markets affect the long-run size of the economy. It is simply not the case that recessions have only transitory effects on an economy. This is a profound, if counterintuitive, lesson for policymakers: The prudent approach during a recession may be much more aggressive fiscal and monetary activism than we are used to.

This issue brief is an attempt to bring policymakers up to speed with the latest academic research on how policy should broadly respond to economic downturns. The first section begins with a brief discussion of the challenges of studying fiscal stimulus. This is followed by a discussion of research on structural changes in the U.S. economy, including the increasingly accepted finding that austerity in the wake of the Great Recession has permanently reduced both U.S. employment and GDP. We also look at how our new understanding of the way the U.S. economy recovers from recessions suggests that there are fewer risks to fiscal activism than previously thought. The brief concludes with a summary of how recent theoretical work on macroeconomics has helped our understanding of fiscal policy’s effectiveness during recessions, as well as a survey of some of the empirical work that has informed the emerging consensus view that activist fiscal policy is an important policy tool.

How economists think about stimulus and austerity

The logic of fiscal stimulus is straightforward: When the economy is not operating at full speed, workers and capital are sitting idle; there is slack in the economy. This is a short-run problem. In the long run, the economy makes use of its resources, but it can take time for aggregate demand to adjust enough to equal aggregate supply. One way to return these idle resources to productive use more quickly is for the government sector to put these resources to work and increase aggregate demand. The government can either do this directly—by spending more—or indirectly—by cutting taxes, so that the private sector has more money to spend and invest.

Austerity and stimulus

In the simplest terms, stimulus and austerity represent opposite reactions, typically to a recession. Recessions result in lower tax revenues, and a government can respond by either doing nothing—in which case it runs a budget deficit—or by engaging in stimulus or austerity. Stimulus, the prescription of the Keynesian economic view, involves deliberately issuing more debt today to finance tax cuts and/or additional spending in a depressed economy to raise aggregate demand and GDP. Austerity is responding to a short-run decline in the economy by raising taxes and/or cutting spending to balance a budget during a depressed economy.

How well this stimulus works is a crucial question for economists. Unfortunately, it is difficult to precisely measure the effects of these policy changes in a depressed economy. Christina Romer, President Barack Obama’s first chair of the Council of Economic Advisers and a University of California, Berkeley, professor, has used the analogy of evaluating treatment for victims of car accidents based on precrash and post-treatment reports of how well the patient feels. Patients always feel worse after a procedure than they did before the crash, but that is hardly informative about how the procedure worked, as it is likely the discomfort is from the effects of the accident. Likewise, it is difficult to measure the effectiveness of fiscal intervention in the economy precisely because the relevant fiscal interventions are only recommended if the economy is experiencing severe negative shocks.

Here, Romer is getting at the issue of counterfactuals. In perfect scientific experiments, researchers recruit and treat a control group and a treatment group so they can know the effect of doing everything but the procedure they are studying, as well as the effect of everything and the procedure they are studying. Economists do not get to do that. There is only one economy, so it is not moral to experiment on it. Consequently, economic researchers only get to try things that are believed to be likely to work, and they have to be clever about finding ways to separate out the effects of the policy they want to study from everything else that happens in the economy. This problem is endemic to economic research, and it is a uniquely difficult challenge in studying activist fiscal policy.

This is an active area of academic debate, so consensus does not imply certainty or uniformity of opinion, but there have been three major shifts in our understanding of fiscal policy since the end of World War II. The first is the original rise of Keynesian economics, which lasted through the 1960s and held that the government should take a very active role in stabilizing the economy.

The second is the rational-expectations revolution that rose to prominence in the 1970s and was the consensus view in academic economics until fairly recently. Under this view, stabilization of the economy was certainly not a task for fiscal policy. Two of the more striking findings from this work were the ideas that the costs of recessions are quite small and that even if the government tried to stimulate the economy, rational citizens would increase their own private savings during any short-term increase in public debt in anticipation of future tax increases, negating any attempt at fiscal stimulus. Although policymakers have never fully converted to this view, it has been the dominant paradigm in academic circles for a generation.

The slow recovery from the Great Recession, amid austerity on both sides of the Atlantic, has coincided with new research in economics and generated a strong theoretical and empirical foundation for the work that policy economists have been doing all along. This research—the third shift in our fiscal policy understanding—has won important converts in academia and the research departments of many of the world’s major macroeconomic institutions.

Keynesian economics

This school of thought believes that governments should actively manage the economy’s aggregate demand to minimize fluctuations in unemployment and economic output. In most instances, these interventions are best conducted through monetary policy. During large recessions, however, managing fiscal policy is often deemed superior because the economy is more responsive to monetary contractions than to expansions. Also, in a sufficiently deep recession, the interest rates needed to stimulate the economy can be negative.

Long-term economic health is not independent of the short-term economy

Macroeconomics textbooks have long subscribed to the view that there are different approaches and techniques that we should use when studying short-term fluctuations and long-term growth in an economy and that the two are driven by distinct, independent factors. In the short term, Keynesian models have been used to justify and design fiscal and—to a greater extent—monetary interventions that keep the economy within acceptable parameters by managing demand. In the long term, the proper understanding is that investment, capital accumulation, and the size and skill level of the labor force are the key drivers of economic growth and that demand is assumed to meet output. Under this convention, long-run changes in the growth rate of the real economy must be the result of shocks, or policy changes, that change aggregate supply.

Short run vs. long run

Economists make strong distinctions between the short run and the long run. In the long run, demand is assumed to meet supply, but in the short run, this need not hold. Governments and central banks can affect aggregate demand, but aggregate supply is driven by long-term fundamentals that are difficult to actively manage. In the short run, most economists believe that either the government or the central bank can raise the economy’s real output by increasing demand when it falls short of supply. In the long run, when supply and demand are balanced, raising demand has no effect on output and only increases prices.

Economists recognize that sharp distinctions between the short run and the long run are a bit artificial, but until this recession, the idea that long-run supply is independent of short-term demand was widely accepted. New research since the recession reveals that insufficient demand alone over a long-enough period of time can actually cause aggregate supply to fall. This reduces the speed limit—or potential GDP—of the long-run economy.

Potential GDP

Potential GDP is the level of GDP that it is possible to achieve for a given aggregate supply without increasing the rate of inflation beyond an acceptable range.

The growing role of human capital in the economy has called this approach into question. Just as physical capital depreciates over time—consider what a five-year-old computer is worth, for example—so can human capital, especially if workers lose contact with the latest developments in their fields of expertise. If the long-run speed limit of the economy—typically called potential GDP—depends on human capital accumulation, and if recessions produce prolonged periods of unemployment that cause a country’s stock of human capital to decline, then short-term demand shortfalls could reduce long-term GDP.

Since the onset of the Great Recession, the shift in expert opinion on this topic has been more dramatic than on any other—if only because the existing consensus was so strong. Before the recession, the accepted wisdom was that macroeconomic shocks could either affect aggregate supply or aggregate demand. Supply shocks—such as a spike in oil prices—would move the potential GDP of the economy, and demand would eventually adjust, balancing at the new level of supply.

Our previous understanding of demand shocks was that they could cause a temporary increase or decrease in GDP but would have no effect on long-run aggregate supply or potential GDP. Consequently, any effect of a demand shock would have to be temporary, and only supply-side shocks could cause long-term changes in the potential GDP of the economy. Olivier J. Blanchard and Lawrence H. Summers first suggested a short-term to long-term demand-side interaction in their 1986 examination of post-1970 growth in European unemployment. At the time, the fact that the problem existed for European economies and not the United States led the authors to suspect that less-flexible European labor markets were translating short-term shocks into long-term growth slowdowns, because higher long-term unemployment reduces the stock of human capital. The authors used the term “hysteresis” to describe the long-run feedback effects of persistently high unemployment, but “eurosclerosis” became the term of art for what the authors were describing. A generation later, there is now talk of “Amerisclerosis” in the wake of the 2007 recession.

As recently as 2011, J. Bradford DeLong and Summers presented research that pointed out the possibility that a similar dynamic may be at play in the United States during the continued slow recovery from the Great Recession. Their central argument was that if we accept the possibility that fiscal intervention can affect long-run aggregate supply, the costs of fiscal stimulus are much lower than previously thought, and activist fiscal policies should be pursued more often. Typical estimates implicitly assume the economy will return to its previous trend and potential GDP, but our experience over the slow recovery shows this is not always the case.

This finding was quite controversial—a point that is unusually clear because the published paper includes a summary of a skeptical discussion that immediately followed the paper’s presentation. As 2013 drew to a close, this view gained considerable validation, with a paper by three economists in the research division of the Federal Reserve Board—Dave Reifschneider, William L. Wascher, and David Wilcox—suggesting that the costs of the prolonged slump could be very large, permanently reducing GDP by as much as 7 percent per year.

Empirically demonstrating that recessions can produce long-run effects in labor markets was a much tougher task given the data requirements, but this too has been a productive avenue for research since the beginning of this recession. As data quality has improved over the past 20 years, this question has become one that can be answered, and it increasingly appears as if short-term shocks do have long-term costs to individuals. This is important because it upends the conventional wisdom that the long-term cost of doing nothing is essentially zero. This new research indicates that even a fiscal multiplier of less than 1 may still correspond with a prudent policy, due to the long-term downside risks to GDP from hysteresis.

Fiscal multiplier

This term is used to describe how large an effect on the entire economy we can expect for a given fiscal intervention. If the government provides $100 in tax cuts or spending increases and GDP then increases by $200, the fiscal multiplier would be 2, which is likely during a recession when the multiplier is typically greater than 1. If the same $100 in cuts or spending only increases GDP by $70, the fiscal multiplier would be 0.7—a typical outcome when the economy is operating at capacity and the multiplier is less than 1. A fiscal multiplier of less than 1 is the mathematical condition that defines “crowding out,” where public spending simply displaces private spending and produces no additional economic growth.

Pairing longitudinal Social Security records with the relatively new Job Openings and Labor Turnover Survey, or JOLTS, Steven J. Davis and Till von Wachter show that workers who are displaced from employment during the mass layoff episodes often associated with recessions experience significant, permanent losses in lifetime earnings. A worker who is laid off when the unemployment rate is more than 8 percent can expect to lose twice as much in lifetime earnings as one who loses a job when the unemployment rate is less than 6 percent. More recently, Alan B. Kreuger, Judd Cramer, and David Cho have presented research suggesting that a disturbingly large fraction of workers who are unemployed for long periods of time never fully regain stability in the labor force, possibly due to individual specific factors, statistical discrimination against the long-term unemployed, or a combination of the two.

Another structural change in U.S. recessions since the early 1980s is the rise of the jobless recovery. Until 1990, recoveries from recessions tended to involve rapid increases in GDP and employment—colloquially called V-shaped recoveries because most data series exhibited a rapid fall and rapid return to baseline—but the 1990, 2001, and 2007 recessions all broke from this pattern with rapid falls followed by slow recoveries. This formed the pattern that gives rise to the so-called L-shaped recovery. Olivier Coibion, Yuriy Gorodnichenko, and Dmitri Koustas found significant evidence of Amerisclerosis in a retrospective look at the U.S. labor market, though they rejected the simple conclusion that monetary and fiscal policies could explain the slowdown. Instead, their lesson for policymakers is forward looking: The structure of the U.S. economy has changed, and the V-shaped recoveries of the 1950s to 1980s, when growth and employment increased rapidly in the period immediately after a recession, seem to be a thing of the past. If that is true, then ensuring that stimulus does not last too long—one of the primary practical problems of devising such a program—is far less worrisome.

These researchers suggest that the “timely, targeted, and temporary” rule of thumb used by policymakers may be out of date in our current economy. Longer-lasting fiscal stimulus programs are more appropriate if L-shaped recoveries continue, as they pose both less risk of inflation due to mistiming and are less likely to end too soon, induce premature austerity, and harm long-term growth prospects. One additional benefit of such a program is that the Federal Reserve’s monetary policy tools are much better at slowing a recovery than speeding one up, so a fiscal policy that creates too much demand will not require unconventional policy measures from the Federal Reserve.

Toward a state-dependent understanding of fiscal intervention

Returning to Christina Romer’s medical analogy, the most important component of successful treatment is a correct diagnosis. Removing an appendix that is about to burst prevents a life-threatening infection and is a useful treatment, but removing a healthy appendix will leave the patient in pain and with unnecessary holes in the abdomen. The effectiveness of the treatment is state dependent: Its benefit can be positive or negative depending on the health of the appendix. The traditional estimate of the effectiveness of fiscal policy is a fiscal multiplier that is not state dependent, equivalent to estimating the benefits of arbitrarily taking out an appendix without first checking to see if the appendix is about to burst. If we assume that policymakers have no ability to discern whether the economy is healthy, this is the optimal approach, but that is a pretty extreme assumption. Since 2000, both governments and central banks have been relatively successful at diagnosing economic crises in real time. Yet until the Great Recession, most mainstream macroeconomic models did not allow for state dependency of fiscal multipliers.

Economists used to model the fiscal multiplier—the percent by which GDP would increase given an additional 1 percent of GDP in spending or tax cuts—as if it were more or less constant across business cycles. Both simple intuition and complex economic models show that this is not the right way to think about short-term fiscal policy, with much of that progress in modeling coming over the course of the Great Recession. In good times, fiscal policy is not very effective—in fact, it is often counterproductive. The simplified explanation is that in normal times, prudent monetary policy counteracts much of the intended stimulus to avoid an overheated economy. But during recessions when the central bank’s monetary policy is also expansionary, fiscal policy is useful, and in severe recessions, when central banks cannot cut rates any further, fiscal stimulus is a crucial, very powerful tool.

The traditional Keynesian view, as laid out by Johnathan A. Parker, is that fiscal policy has beneficial effects when there is slack in the economy, but not when the economy is operating normally. Unfortunately, as Parker goes on to explain, there are very few rigorous macroeconomic simulation models that are mathematically compatible with the idea of slack in the economy. In technical terms, the models do not allow for state dependency. In other words, they are unable to estimate different multipliers for recessions and for normal times. For a variety of reasons, estimating these two different multipliers is much more than twice as hard as estimating one.

Estimating multipliers

Developing rigorous estimates of fiscal multipliers is a technical challenge, and state-dependent multipliers are even more difficult to estimate. Theoretical estimates of multipliers come from simulating policy in a model. These models abstract from the economy by leaving out some detail, but they rigorously specify how people and firms behave to maximize their own benefits in major sectors of the economy. The model is then calibrated to match the behavior of historical data in the U.S. economy.

Such a model is already a mathematical approximation of the real world, and solving for simultaneous equilibriums in the policy simulations of a model often requires further approximation. Most of these simulations start with the model in equilibrium, then introduce a shock and solve for the new equilibrium. The vast majority of solution techniques used represent the model as a continuous function, often one that is nearly linear near the previous solution.

This implicitly makes it much harder to represent a state-dependent multiplier—one that jumps from a value of less than 1 when the economy is at equilibrium to a value of significantly more than 1 in a recession—because it does not behave like a continuous function. This means that even a correctly structured model may give incorrect or imprecise estimates of the size of fiscal multipliers in the conditions where policymakers are most likely to use fiscal policy.

Fortunately for us but unfortunately for our models, recessions are rare, and large recessions are even more rare. More flexible models require more data to make estimates. A model that has more structure can make use of a greater variety of macroeconomic data in every time period and use theory to tease out more information when there are limited data available. Part of the reason we have made so much progress in modeling state-dependent multipliers since the Great Recession is that we now have more data about how the U.S. economy performs in severe recessions.

Modeling techniques: DSGE and VAR

Macroeconomics is very hard to study because there are a relatively small number of data points, so macroeconomic modelers rely on economic theory to extract as much insight from these data as possible. Two of the most commonly used techniques are vector autoregression, or VAR, and dynamic stochastic general equilibrium, or DSGE, models. In VARs, relationships between data points can be flexibly established over time. We know, for example, that tomorrow’s investments must depend on today’s savings, so we can estimate these internal linkages and maximize the information that each time series provides in the context of other data to estimate how an economy responds to shocks. In a DSGE model, a series of equations defines economically rational behavior in individual markets, and individual, random shocks hit parts of the economy. Their effects then decay over time due to linkages in the model economy.

In VAR and DSGE models, the mathematical techniques used to solve the models rely on abstracting an additional level from them. Typically, these restrictions on the complexity of the models’ solutions are an acceptable trade-off because they can show a significant level of detail about the linkages between economic variables. This is particularly important to macroeconomic modelers because of the relative paucity of relevant data, even if it comes at the cost of being able to precisely model the exact dynamics of rare events. The trade-off, however, is that the conditions that must be satisfied for a solution method to work may not be an accurate description of how markets function during the early stages of a recession. In a review of relevant literature, Valerie A. Ramey provides a fairly complete taxonomy of how the mechanisms in both classical and Keynesian models drive the estimates about the size of these models’ multipliers.

This is not to say that it is impossible to build advanced models that incorporate state dependency. Indeed, some of the more interesting recent work in macroeconomic modeling has addressed this challenge. Alan J. Auerbach and Yuriy Gorodnichenko use a VAR approach and come up with much larger estimates for multipliers when the economy is depressed. Lawrence Christiano, Martin Eichenbaum, and Sergio Rebelo likewise constructed one of the first examples of a DSGE model economy where agents face different incentives when interest rates run up against the zero lower bound—the point at which the central bank’s policy calls for negative interest rates—and find that in this context, a 1 percent increase in government expenditures can generate as much as a 3 percent increase in GDP.

There is still reason to treat all of these estimates with caution, as Parker points out. There are two major failings of the mathematical models that generate these estimates of fiscal multipliers. Not only is state dependency difficult to model mathematically, its interpretation is not straightforward even when one does get a reasonable estimate of the state-dependent multiplier. We can use models to estimate the effect of the first dollar of stimulus—the marginal multiplier—but not the effect of an entire stimulus program—the average multiplier, which is more useful for developing policy solutions. For a small stimulus program, this marginal multiplier is a reasonable approximation of the entire program’s effects. But for precisely the kind of stimulus that theory suggests we should be studying—large programs in the face of significant economic downturns—the size of the marginal multiplier can differ significantly from the average multiplier. This makes it difficult for policymakers who are fighting recessions to gauge the effects of their policy choices.

One area of research in which considering the effects of expansionary policy vs. austerity policy in the face of a depressed economy has not changed in the past decade is the idea that not every dollar of stimulus is alike. There remains broad agreement that fiscal multipliers vary dramatically based on how spending and tax cuts are directed. It remains true that the bang for the buck is smallest when government cuts taxes for high-income earners. Intuition is helpful here, as wealthy people are most likely to behave as optimizers, saving temporary cuts to finance future taxes or consumption. In other words, giving someone with a steady job and lots of cash on hand a $1,000 tax cut is likely to result in approximately $0 in increased demand for output. In contrast, giving an unemployed worker $1,000 in extended benefits is likely to result in nearly the entire amount being spent, as these workers lack the additional assets or income to save more or secure a loan to finance their consumption during unemployment.

One of the less explored aspects of this debate is that the actual benefit of the investments the additional spending generates is largely irrelevant for these economic models. The typical assumption is that public investments are analogous to throwing the money in the ocean. That is, most macroeconomic models generally assume that public investment has zero productive benefit. This assumption is obviously a caricature, but it reflects both the field’s desire for comparable measurements across studies and its general belief that private markets are more efficient at allocating capital than are public officials. This approach is often counterproductive in assessing fiscal stimulus—it allows researchers to isolate the effects of the timing of spending from its productive effects but obviously undervalues any public investment with positive returns.

Actual economic work on the effectiveness of public investments is rare, but one interesting source is a 1993 paper by Marianne Baxter and Robert G. King. This is a well-known work among academics, and the authors are broadly skeptical of the effectiveness of fiscal policy. Yet they note that a $1 investment in productive public capital could produce between $4 and $13 in overall long-run GDP increases, with the range coming from differences in assumptions about how much less productive public investment is than private investment.

Again, some caution is warranted here. These results do not suggest that government spending is the right response to every hiccup in the economy. In fact, the literature is quite consistent in its suggestion that this kind of micromanaging of the macroeconomy is unlikely to be successful. However, with considerable slack remaining in the U.S. economy five years after the Great Recession, it is clear that the premature moves toward austerity that took hold on both sides of the Atlantic have been bad policy, and it may now be too late to prevent a large, permanent decline in both U.S. and EU GDP.

Evolution of techniques for measuring fiscal policy

The hardest part of studying fiscal intervention is determining appropriate counterfactuals. This means that good economic research has to be clever about finding ways to separate out the effects of the policy we want to study from everything else that happens in the economy. This is an especially challenging problem in the study of fiscal policy for two reasons:

- There are very few of the right kind of events to study—periods in which the government acted with fiscal policy to counteract a negative economic shock.

- The examples where this does happen include, by definition, an unusually large negative economic shock, which usually has an even larger effect on the economy than the actual policy about which we care.

With these caveats, it is important to point out how far research on fiscal policy has come over the past 20 years and how much better it is now than the research that formed the consensus among academics and policymakers in the decades leading up to the Great Recession.

Cyclically adjusted budget balance

The cyclically adjusted budget balance is a measure of what the budget deficit or surplus of a government would look like, when changes in tax revenue and need-based spending driven by the business cycle are taken into account.

Until surprisingly recently, the dominant method of studying fiscal policy was to look at the cyclically adjusted budget deficit of a country. Recall that fiscal expansion can take the form of deficit-financed tax cuts or increases in government spending, so it is reasonable to look at the budget deficit as a measure of fiscal stimulus in the face of data-gathering

constraints.

Unfortunately, lots of things that are not tax cuts or government spending affect the budget deficit. On the expenditure side, means-tested programs—such as the Supplemental Nutrition Assistance Program, or SNAP, formerly known as food stamps, and unemployment insurance—automatically become more expensive as recessions make people worse off and a larger share of the population qualifies for them. On the tax side, as firms’ profits and individuals’ incomes are reduced by the recession, income and capital gains tax revenues automatically fall. A recession that causes both of these things to happen at the same time will produce a large budget deficit, but that deficit is not a great measure of how much the government is trying to stimulate the economy. Researchers have corrected for these effects on budgets by using a cyclically adjusted measure that attempts to take into account the state of the economy and its effect on budget deficits. But because cyclical factors have a strong and persistent effect on the budget deficit, it is very difficult to establish whether growth happens because of or in spite of the policies pursued. Consequently, it is a poor measure for drawing conclusions about whether or not fiscal policy caused changes in economic conditions.

A new approach, pioneered by Valerie Ramey and Matthew D. Shapiro in 1998, is to examine a narrative historical record—reading articles from the past to determine when government spending was unexpected and on what it was spent. Because this spending was unanticipated, it was less likely to be subject to mismeasurement due to other economic factors. A similar approach was taken in 2009 by Christina Romer and David H. Romer, who used narrative records not only to identify the timing of historical tax changes but also to divide the intended effects of these changes into four categories: stimulating the economy, reducing deficits, inducing higher long-run growth, or other goals.

Ramey, working with multiple co-authors and using a variety of structural predictions of models to analyze macroeconomic policy, has consistently found that multipliers in the United States are small. Some of these mechanisms include spillovers from increased government spending in one sector to other sectors and the cyclical behavior of firms’ pricing markups. In contrast, the Romer and Romer approach finds that the multiplier on tax cuts—especially those explicitly meant to stimulate a depressed economy—is quite large. This is somewhat surprising because theory is very clear that the multiplier on tax cuts should be weakly smaller than on government purchases.

As these more informative, labor-intensive methods gain traction, it is important to note that simple empirics have become much more powerful in the past five years, largely because of policies pursued in response to the Great Recession. It is still true that there is a paucity of relevant data points from advanced economies, but researchers are awash in data compared with 10 years ago. While there may have been some debate about the size of fiscal multipliers before the recession, a broad consensus would have prevented economists from recommending the austerity policies pursued in Europe and the United States since the Great Recession. The data from these policy actions have demonstrated that austerity has been counterproductive across the globe for the levels of slack seen in the aftermath of the Great Recession. Olivier Blanchard and Daniel Leigh use relatively simple techniques to show that austerity in Europe has consistently resulted in lower GDP growth than was forecasted during the past five years.

This is far from the last word on the question of fiscal stimulus. Data will be revised and improved, and theoretical and empirical techniques will advance, both of which will give us an even clearer picture of what effects fiscal policy can have in a depressed economy. Overall, economic researchers are in much stronger agreement about the usefulness of fiscal policy than they were a decade ago. Ironically, much of the data that have made the empirical work that supports this consensus possible are the result of policymakers going against the existing economic consensus.

Conclusion

Since the onset of the Great Recession, fiscal policy has become a much more widely studied topic in academic circles. The broad conclusions of recent work are surprisingly consistent for the field. Fiscal multipliers are larger than we thought, at least in slack economies. Even some of the sharper critics of activist fiscal policy have concluded that “the US aggregate multiplier for a temporary, deficit financed increase in government purchases … is probably between 0.8 and 1.5. Reasonable people can argue that the data do not reject 0.5 and 2.” Supporters suggest that multipliers as large as 3 are possible in a slack economy and that fiscal policy is perhaps even more important in light of the new understanding of how the long-term potential GDPs of advanced economies are affected by recessions.

This research does not indicate that deficits do not matter or that stimulus is always the answer. Instead, the greater consensus around larger fiscal multipliers suggests that fiscal stimulus has fewer risks than we thought and is a very powerful and important tool for boosting short-term economic growth in a way that monetary policy cannot replicate. Turning to austerity before robust economic growth occurs can be self-defeating, depressing economic growth and increasing budget deficits in both the short term and the long term. Considering fiscal policy in a vacuum is a mistake, and it is important to consider the role of the central bank, which has better tools to address too much stimulus than it does to address too much austerity.

More importantly, economic research has developed a new understanding that prolonged, short-run unemployment decreases long-run GDP. The consensus on the costs of inaction has changed dramatically within the field: While many academic researchers thought of the costs of recessions as a rounding error a generation ago, the emerging view is that failing to lift an economy out of recession could permanently reduce its size. In the United States, this could reduce GDP by something on the order of $1 trillion each year.

The takeaway for policymakers is simple. Fiscal stimulus is a much more powerful tool in today’s economy than we previously thought, and the austerity policies we have been pursuing are even more costly. Most importantly, the comforting belief that policymakers can, without causing harm, do nothing while they wait for the economy to rebound is mistaken. The failure to break out of the deep recession and the anemic growth still engulfing Western economies has resulted in significant long-term damage to them. That damage continues to pile up as policymakers ignore the need to get their respective economies back to full employment.

Michael Madowitz is an Economist at the Center for American Progress.