The law commonly known as the Tax Cuts and Jobs Act1 (TCJA), enacted in December 2017 by the Republican-controlled Congress, is substantially increasing federal deficits—and will for years to come. Regrettably, the law increased federal borrowing while addressing none of the nation’s most pressing challenges. In particular, after decades of growing income inequality and stagnant real wages for working-class Americans, the law conferred its largest benefits on the wealthiest Americans. The law did nothing to rebuild the nation’s infrastructure, advance education, or prevent climate change. Moreover, by increasing federal deficits and debt, the law will increase pressure to cut vital programs, including Social Security, Medicare, and Medicaid.

This issue brief assesses the fiscal damage from the TCJA and finds:

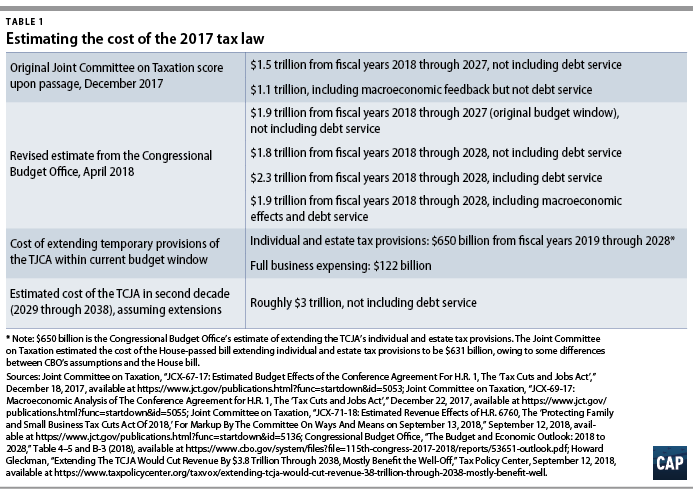

- The law will increase deficits by about $1.9 trillion over 10 years, according to the nonpartisan Congressional Budget Office (CBO). This increase would constitute major fiscal damage. If core features of the law are extended, the TCJA would increase deficits by another $650 billion over 10 years and add roughly $3 trillion to deficits over the second decade after enactment.

- The law has already drained revenue and thus hiked deficits. Indeed, the TCJA was the biggest contributor to the large increase in the deficit for the fiscal year that ended in September 2018.

- The law could cost much more than official estimates because it includes numerous fiscal time bombs, including expiring tax cuts that future Congresses could extend and delayed tax increases that future Congresses could further forestall. The law is also replete with loopholes that are already being exploited in ways that were not fully recognized during the bill’s hasty consideration.

These are not unintended effects of the law. The tax law was part of a deliberate strategy to increase budget deficits and thereby raise pressure to cut programs such as Social Security, Medicare, and Medicaid. And the aspects of it that will likely cost more than advertised are, for the most part, also the result of a deliberate strategy: Congressional leaders rushed the bill through Congress with no hearings and little time for public scrutiny in order to obscure its effects. Wealthy individuals and corporations are the law’s biggest beneficiaries, and it is no coincidence that they will have many opportunities to stretch the law’s myriad loopholes even further and press Congress for even more tax breaks.

The TCJA will increase federal deficits by $1.9 trillion over 10 years

When the TCJA was finalized in Congress in December 2017, Congress’ nonpartisan Joint Committee on Taxation (JCT) estimated that the legislation would increase federal budget deficits by about $1.5 trillion, or $1.1 trillion if scored dynamically, over the 10-year period from FY 2018 through FY 2027, not including the government’s interest costs resulting from the increase in debt.2 Because the JCT is Congress’ official scorekeeper on revenue bills, $1.5 trillion was the bill’s official score upon passage.

In April 2018, the CBO, likely in consultation with the JCT, issued a new estimate of the budgetary effects of the law. The CBO’s report estimated that the law would increase deficits by nearly $1.89 trillion over the FY 2018–2027 period—more than $400 billion greater over the same period than the JCT had estimated four months earlier.3 The CBO attributed its higher estimate in part on technical revisions and explained: “Many of those adjustments reflect information that has become available in recent months about the 2017 tax act.” In other words, new information had caused the underlying cost estimate of the bill to increase by more than $400 billion.

The CBO also produced estimates covering the current budget window, which extends through FY 2028. Between FY 2018 and FY 2028, the CBO estimates that the TCJA will cost slightly less, or $1.84 trillion, than over the original FY 2018–2027 budget window because the law is projected to reduce deficits beginning in 2027. However, as discussed below, there is reason to doubt whether that will be the case. The CBO also produced a dynamic estimate, which included the budgetary impact of macroeconomic feedback, and estimates of the additional interest costs. These latter two effects roughly offset each other, resulting in deficit increases of $1.9 trillion from FY 2018 to FY 2028. In sum, regardless of how it is measured, the legislation inflicts major fiscal damage.

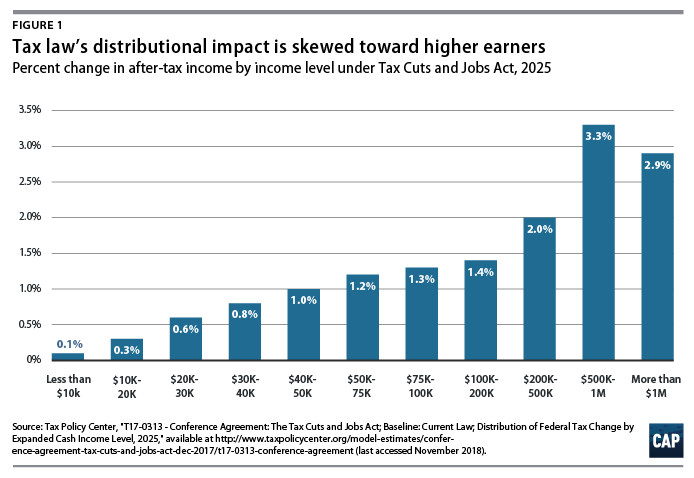

The tax law inflicts this fiscal damage while also worsening one of the nation’s most fundamental problems: economic inequality. The TCJA’s benefits were heavily weighted to high-income Americans. The highest-income 1 percent of Americans—people with annual incomes of at least $732,000, averaging $2.25 million—are receiving an average tax cut of more than $50,000 this year from the bill.4 This is more than 50 times greater than the benefit for the average middle-income family. High-income Americans even receive a disproportionately large benefit as a percentage of their income. (see Figure 1)

Moreover, the law was poorly timed and misdirected. It increased federal borrowing to boost demand several years after the U.S. economy needed it most, yet it also failed to seriously address underlying structural challenges in the economy. In the years when the economy was struggling to recover from the Great Recession, the federal government—due to the Republican-led House’s demands—shifted prematurely to budget austerity, keeping millions out of work and prolonging the economic pain.5 Only now, nine years into the recovery, have President Donald Trump and congressional Republicans shifted to expansionary fiscal policy, albeit through a tax bill that delivers low bang for the buck. The tax cuts are likely providing some economic boost this year, but they come at a tremendous cost and in the most inefficient way possible: through long-lasting tax cuts that are weighted toward the already-wealthy. By increasing federal debt, the tax law could worsen future economic downturns by making policymakers more reluctant to address them with aggressive fiscal policy.6 This wasteful approach to fiscal policy completely ignores the deeper structural challenges facing the U.S. economy, particularly in areas that have been hit hard by deindustrialization. Tax cuts provided to companies are failing to deliver job opportunities, wage growth, or hope to those workers and hard-hit communities, who will have to live with the debt that the TCJA created for years to come.

The tax cut is already draining revenues and increasing deficits

The negative fiscal effects of the tax law are already materializing. In FY 2018, federal revenue fell well short of pre-tax cut projections.7 Revenue for FY 2018 was $202 billion less than the CBO forecast before the TCJA’s passage. FY 2018 revenue was $325 billion less than the Trump administration projected in its initial budget, which ostensibly incorporated the effects of the president’s tax proposals. Moreover, the core provisions of the tax law did not take effect until three months into FY 2018, and the tax payments that individuals made in April 2018 were based on the pre-TCJA tax code. Since May 2018, overall revenue has decreased by 3 percent compared with the same period in 2017, without even adjusting for inflation or growth.8

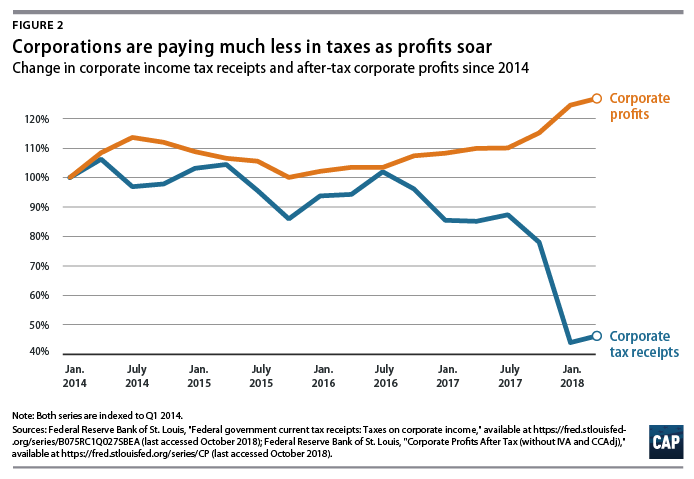

Tax revenue from corporations has fallen dramatically as a result of the massive corporate tax cut that was at the core of the TCJA. The law slashed the corporate tax rate by two-fifths, or from 35 percent to 21 percent, while expanding the already substantial depreciation deductions (moving from bonus depreciation to the more generous full expensing). And rather than phasing in over time, the corporate rate was made immediate, taking effect only days after the bill was signed into law in December 2017. As predicted, corporations paid $92 billion, or 31 percent, less in taxes in FY 2018 than they did in the year before.9 The decline was more dramatic compared with what corporations would have paid in FY 2018 under pre-TCJA law. Compared with the CBO’s pre-TCJA forecast, the decline in corporate tax revenue for FY 2018 was $119 billion, or 37 percent.10

The TCJA was the primary reason the federal budget deficit increased by 17 percent to $779 billion, or 3.9 percent of gross domestic product (GDP), for FY 2018.11 Revenue fell to 16.5 percent of GDP. The draining of revenue and corresponding rise in the deficit is particularly striking given that the economic recovery has continued apace in 2018, with unemployment levels continuing on the downward trajectory that began in 2009. The level of revenue as a share of GDP in FY 2018 was the lowest in more than 50 years except for six years during and following recessions, FY 2003–2004 and FY 2009–2012.12

The draining of revenues belies the predictions made by the TCJA’s proponents. Upon the bill’s passage in the Senate, then-Majority Leader Mitch McConnell (R-KY) said: “I not only don’t think it will increase the deficit, I think it will be beyond revenue neutral.”13 Treasury Secretary Steven Mnuchin claimed that “this tax plan will not only pay for itself but in fact create additional revenue for the government.”14 All credible nonpartisan analysts rejected claims that the tax cut would pay for itself, and their warnings of reduced revenue are now bearing out. The TCJA’s proponents’ claims were premised on the law sparking an enormous boom in private investment, but to date, there is little to no sign of any such investment boom.15

The fiscal damage may be far worse than it appears

Official estimates of the TCJA may significantly understate how much the law will drain revenue over time. Packed within the law are three kinds of fiscal time bombs, the costs of which are not reflected in official estimates. This was deliberate on the part of the bill’s authors. As President Trump’s Director of the Office of Management and Budget Mick Mulvaney has admitted, the timing of many of the bill’s provisions was “simply trying to essentially manipulate the numbers and game the system so that you can fall into this square peg”—in other words, to fit within budget constraints.16

Expiring provisions

Almost all of the TCJA’s individual tax provisions expire after 2025, and the law’s proponents are already seeking to extend them. The TCJA’s authors inserted the 2026 expiration date to manipulate the official scoring of the bill so they could pass it without any support from congressional Democrats. They also chose to advance the bill through the budget reconciliation process, shielding it from a potential filibuster by Senate Democrats. Under the Byrd Rule, bills moved through the reconciliation process cannot score as increasing deficits over the long term, or else they effectively require 60 votes in the Senate.17 The score of reconciliation bills also must fit under the maximum deficit increase allowed in the House-Senate budget resolution, which, under a deal struck by Senate Republicans, was $1.5 trillion over 10 years.18 To fit within these two constraints, the TCJA’s authors chose to sunset the bill’s individual tax provisions so that the JCT’s official scores would reflect the revenue drain ending after just eight years.19 While the TCJA gave corporations a permanent net tax cut, it managed to offset that cost in the official estimates through a permanent, broad-based tax increase on individuals—through a technical change in the tax code’s inflation adjustments—and the permanent repeal of the Affordable Care Act’s (ACA) individual mandate—which scored as reducing deficits because it will result in fewer people having government-subsidized health insurance.20

The artificial sunsets reduced the bill’s official cost to just less than $1.5 trillion over 10 years. That allowed the bill to be passed despite unified Democratic opposition and helped some Republican members who had frequently decried rising deficits to rationalize their support for the bill.21 But no sooner had the TCJA passed than Republican leaders announced they would take up legislation making its costly individual and estate provisions permanent without offsetting the cost. The House passed such legislation in September 2018.22 On top of the original tax cuts, the House bill was estimated to cost an additional $631 billion within the 10-year budget window, which would bring the total cost from the TCJA and its extension over 10 years to about $2.5 trillion. The revenue loss would continue in the following decade. Together, the TCJA and the extension of the individual provisions would drain roughly $3 trillion in revenue over FY 2029–2038, raising the total cost of the legislation over two decades to more than $5 trillion. (see Table 1) As with the original TCJA, the extension of its individual and estate tax provisions favors people with high incomes. The average household in the top 1 percent of incomes would receive a $40,000 annual tax cut; this is more than 80 times greater than the average tax cut for households in the bottom-earning 60 percent.

The TCJA also included other temporary provisions that lose revenue and would continue to do so if extended. The largest is full expensing of business investment, which would add $122 billion to the TCJA’s cost over the next decade if extended beyond its scheduled phasedown.23 Other sunsetting provisions would add around another $60 billion over that period.24 If permanently extended, the cost of these provisions would continue beyond the next decade as well.

Delayed revenue-raising provisions

The TCJA included many provisions that raise revenue from corporations and other businesses, which partially offset the cost of the corporate and business tax cuts. However, several of the biggest of these provisions do not begin or take full effect for several years, giving the business community plenty of time to lobby Congress to stave them off. For example, the TCJA’s authors reduced the official 10-year cost of the bill by $120 billion with a provision requiring businesses to spread their deductions for research and experimentation expenses over a five-year period rather than claiming them immediately. But that provision does not take effect until 2022 and will certainly be the subject of intense lobbying before then.

Other corporate and business provisions take effect in 2018 but become more stringent in later years, creating the same dynamic. Two of the most significant are the tax on certain foreign income of U.S. companies, known as the global intangible low-taxed income (GILTI) tax, which starts at a rate of 10.5 percent—half the U.S. domestic rate—but rises to 13.125 percent after 2025; and the limit on interest deductions, which becomes tighter starting in 2022. If these two provisions are not dialed up on schedule, the TCJA’s cost would increase by tens of billions of dollars.

Although it was billed as a once-in-a-generation tax reform, the TCJA failed to permanently resolve the fate of the so-called tax extenders—the temporary tax breaks that Congress has habitually extended for one or two years at a time. In 2015, and at a sizeable cost, former President Barack Obama and Congress reached agreement on legislation to make many of these extenders permanent while letting others expire after 2016 or gradually phase down. At the time, House Speaker Paul Ryan (R-WI) said: “We are ending Washington’s days of extending tax policies one year at a time.”25 Any legislation worthy of being called tax reform should have resolved the fate of these provisions once and for all. But the TCJA was silent on them, and soon after, Congress extended them for yet another year, retroactively for 2017, at a cost of $13 billion. If these provisions continue to be extended, they would drain $92.5 billion of revenue over the next decade.26

Gaping loopholes

The revenue drain from the TCJA could also be greater than initial estimates as clever lawyers and accountants find ways to exploit the law’s loopholes. The TCJA is an enormously complex piece of legislation that was rushed through Congress in only 50 days with no public hearings—a shocking departure from norms of tax policymaking.27 Whereas Congress worked on the Tax Reform Act of 1986 for 53 weeks, the TCJA went from introduction to enactment in just seven weeks.28 The process gave tax experts and the public very little chance to scrutinize the legislation. A group of tax law scholars hurriedly assembled an extensive list of ways that taxpayers, and particularly corporations and well-heeled individuals with expensive tax advisers, could game the new tax system.29 But Congress did not address the red flags that they raised, and corporations and wealthy taxpayers are already actively gaming the new law.30 In fact, some large corporations began gaming aspects of the law even before it was passed, such as the differential rate on offshore earnings held in cash and noncash assets, which was telegraphed well ahead of the law’s enactment.31

The JCT’s cost estimates seek to account for this kind of tax avoidance, but given the law’s truncated consideration, it is unlikely that the JCT, with its first-rate but fairly small staff of about five dozen people, anticipated all of the schemes that would develop over time. Such a rushed and secretive process inevitably creates an asymmetry: Powerful corporations and interest groups will speak up when they are disadvantaged by draft provisions under consideration but may stay silent when they spot hidden loopholes that work to their advantage.

Furthermore, congressional Republicans have waged a sustained effort to starve the Internal Revenue Service (IRS) of the resources that it needs to prevent illegal tax evasion and aggressive tax avoidance by corporations and individuals wealthy enough to hire high-priced tax advisers. The number of IRS enforcement personnel is down by one-third since 2011.32

Following are examples of major provisions of the law that may lose much more revenue or raise much less revenue than anticipated at the time of enactment.

Passthrough business deduction

Before the TCJA, people who own passthrough businesses such as partnerships, S-corporations, and LLCs paid taxes on the income from those businesses at ordinary income tax rates. The TCJA created a special new deduction that effectively cuts the rate on such income by 20 percent, with various, highly complex rules, or so-called guardrails, restricting the deduction for some owners and types of businesses. As tax expert Michael J. Graetz explains:

The new law creates important new differences in tax rates between employees and sole proprietorships—including individual independent contractors—and among businesses depending on their levels of income, their kinds of business, and, for higher income businesses, the wages they pay and the size of their business assets … Never before 2018 have such sharp distinctions in tax rates been applied so broadly to varying industries and lines of business.33

These arbitrary rules invite massive tax gaming, which undermines the integrity of the tax system. And indeed, the collective brainpower of the tax and accounting worlds is now being applied to exploit the new provision by recharacterizing income as the kinds eligible for the deduction—as well as to lobby the IRS and Treasury Department for more businesses to receive the favored treatment.34 The passthrough deduction was estimated to reduce revenues by $414 billion over 10 years. But, as many experts have warned, the recent tax expenditure estimates from the JCT suggest that it will prove much more costly.35 And the CBO’s April report cautioned that its estimates of the law’s costs are subject to significant uncertainty, noting specifically that the estimates “incorporate the expectation that the Treasury will be able to enforce the limits that the [TCJA] places on the types of income that are eligible for the deduction.”36 Few tax lawyers share that expectation, which means that the deduction could prove far more costly than estimated.

Opportunity Zone tax shelter

The TCJA carved out new and very generous capital gains tax breaks for investments linked to certain geographical areas, ostensibly in an effort to spur investment in economically distressed communities. Investors who have unrealized capital gains can delay taxes by rolling over their investments into Opportunity Funds. Over time, these investors receive a generous tax break on their original gains and zero tax on their gains from the fund. Official estimates were that the provision would reduce revenues by $1.6 billion over 10 years—mere pennies in the scheme of the tax bill—partly because of budget window gaming.37 But early real-world indications are that this incentive may prove to be a much bigger boondoggle than was fully understood during the TCJA’s rushed consideration, adding to its fiscal cost.38 Moreover, it seems increasingly unlikely that residents of distressed communities will be the main beneficiaries of this new incentive, as opposed to wealthy investors and intermediaries. The magnitude of the tax benefits for investors is potentially limitless, while there are no hard rules to ensure that zone residents benefit in the form of jobs, subcontracts, or other opportunities.39

State and local tax deduction cap

One of the biggest revenue-raising provisions in the TCJA is the $10,000 limit placed on the personal itemized deduction for state and local taxes (SALT). That provision, in conjunction with other changes to itemized deductions, reduced the bill’s official cost by $668 billion. But experts warned that state legislatures could respond by changing their tax systems in ways that would allow their residents to continue claiming uncapped SALT deductions on their federal taxes.40 Since the TCJA was enacted, legislators in several states have introduced bills providing so-called workarounds to the SALT cap, and Connecticut, New York, New Jersey, and Oregon have enacted versions of such workarounds. The IRS and Treasury Department have proposed regulations curbing one such workaround, but states may push forward with others.41

Repatriation tax

The TCJA’s 10-year cost was reduced by $339 billion through a one-time transition tax on the large amounts of earnings that U.S. corporations had booked in their foreign subsidiaries, on which they had never paid U.S. tax. The bill provided for a two-tiered transition rate: 8 percent for earnings held in illiquid assets and 15.5 percent for liquid assets.42 Because it was fairly well-known in advance that Congress would adopt this basic structure for taxing overseas earnings, companies engaged in tax planning by moving assets around.43 Based on actual corporate earnings reports released this year, Bloomberg Tax has estimated that the revenue haul from the one-time tax could be less than half of the $339 billion estimate.44

Implications and solutions

The fiscal damage from the TCJA is only one of the law’s unfortunate effects. The law will also increase income and wealth inequality and widen the racial wealth gap.45 It sabotages the ACA by repealing the individual mandate, which the CBO estimates will raise health insurance premiums by 10 percent and result in roughly 9 million more people without insurance.46 The law sold out the Arctic National Wildlife Refuge for oil drilling.47 And according to estimates, it will reduce charitable giving by 5 percent, which will mean about $20 billion less for the nation’s charities each year.48

The loss of revenue from the TCJA is severe, and unless policymakers address it, it will grow. From the initial cost estimate of $1.5 trillion over 10 years and the revised estimate of $1.9 trillion, the cost will grow if Congress extends its revenue-draining provisions and/or staves off its revenue-raising provisions. The cost could also grow if the Treasury Department and IRS do not aggressively guard against gaming.

The law’s proponents claimed that the TCJA would pay for itself. Some even claimed that it would raise revenue. But those predictions were baseless to begin with and are already being proved wrong. Now the law’s proponents are suggesting that the costs will need to be made up by cutting Social Security, Medicare, and Medicaid—effectively making working Americans and the elderly pay for tax cuts for the wealthy and corporations.

Policymakers should take the following steps to mitigate and reverse the fiscal damage from the TCJA.

Stop extending tax breaks

Congress should stop extending tax breaks, including the new ones that the TCJA created, without offsetting the revenue loss. Moreover, the so-called extenders were extended through 2017 retroactively, and House Republicans are now seeking to extend them retroactively for 2018 in the lame-duck session of Congress.49 Congress should fully offset these provisions or let them remain expired.50 Congress should also resist pressure to further delay revenue-raising provisions or address supposed errors in the TCJA by expanding tax breaks without offsetting the resulting costs.51

Prevent tax evasion by strengthening the IRS

Congress must strengthen the IRS’ ability to prevent tax avoidance. The complexities and special tax breaks in the new law will reward those with resources to exploit them and those who are most willing to push legal boundaries.52 In addition, the United States was already losing more than $400 billion in revenue each year due to noncompliance.53 Recent high-profile stories illuminate the problem of tax evasion by wealthy individuals, including, allegedly, by President Trump and his associates, and its tie-in to corruption.54 Congress should significantly boost the IRS’ budget, including its enforcement resources, to minimize the revenue loss from the TCJA and protect the integrity of the tax system.

Reverse the tax breaks for those who need them least

Most importantly, future Congresses must fundamentally restructure the TCJA to reverse all of the tax cuts for the wealthy and corporations, end egregious loopholes such as the passthrough deduction, and raise revenue to meet national challenges.

Conclusion

In sum, the TCJA was a deeply fiscally irresponsible giveaway that favored profitable corporations and wealthy Americans. The law will increase federal borrowing by nearly $2 trillion—and in all likelihood much more than that amount due to the fiscal time bombs it includes. Moreover, the legislation failed to address the nation’s most urgent challenges. And by increasing federal debt, the law will raise the pressure to cut vital programs such as Social Security, Medicare, and Medicaid. Finally, the legislation could make policymakers much more reluctant to respond aggressively to future economic downturns. Congress should address the TCJA’s deep flaws as soon as possible through real tax reform.

Seth Hanlon and Alan Cohen are senior fellows at the Center for American Progress. Sara Estep is a research assistant at the Center.