The question for policymakers, and all other citizens, is no longer whether humans are changing our climate. The question now is, how we can stabilize an already-changing climate in a way that promotes economic prosperity? While recently established domestic policies have made strides toward a lower carbon future, such measures are stepping stones. They prescribe the initial path but will not lead to the final goal of achieving the reductions in greenhouse gas emissions necessary to help stabilize global temperatures. Effectively mitigating climate change requires identifying exactly how the United States will transform its energy economy to attain international goals to help protect our climate.

This report quantifies the level of investment required for the United States to align emissions reductions with international goals in an economically beneficial and technically feasible manner. The specific emissions-reduction goal we explore in this study is what the Intergovernmental Panel on Climate Change, or IPCC, has proposed for the world as a whole: reducing greenhouse gas emissions by 40 percent from 2005 levels by 2035. To do its part to meet this goal, the United States must reduce its carbon dioxide emissions from energy-based sources by 40 percent, to 3,200 million metric tons, or mmt, over roughly the next 20 years. The proposals in this report put the United States on this track to effectively mitigate global climate change.

The report covers three areas of analysis. It first describes the need for a substantial new wave of mostly private investment in advanced energy technology and higher performing buildings, as well as significant public and private investment needed to build dramatically more efficient infrastructure. Second, it outlines how the United States can and must reduce its use of fossil fuels by 40 percent within the next 20 years, as the window of opportunity to stabilize our changing climate is small and closing rapidly. Third, the report shows that stabilizing the climate requires bold actions that we term the PERI-CAP scenario. In addition to this analysis, the report outlines flexible policy options that can be utilized to take the needed actions. Notably, the report finds that this investment agenda will not only protect our climate but will also generate 2.7 million net new jobs.

Findings

Greater clean energy investment is vital to the nation’s welfare and economy

The report finds that the investment needed to stabilize our climate and improve our economy amounts to about $200 billion annually in both public and private resources. Average net public expenditures would comprise roughly one quarter of that total, averaging $55 billion per year, which falls within the $44 billion to $60 billion per year range that the United States has devoted to clean energy investments in recent years. If a successful carbon tax or cap were implemented as part of this plan, it would also yield public revenues averaging $200 billion per year.

To put the clean energy investment total in perspective, consider the following:

- Public expenditures would comprise 0.3 percent of current U.S. GDP and roughly 1.4 percent of the federal budget.

- Total expenditures—public and private—are roughly 1.2 percent of current U.S. GDP.

- A recent White House Council of Economic Advisors report found that a temperature increase of 3 degrees Celsius above pre-industrial levels would increase economic damages by $150 billion, year after year in perpetuity.

- Total expenditures are roughly 40 percent below U.S. oil and gas industry investments for 2013.

Of the $200 billion needed for annual investments, $90 billion must be invested in raising efficiency standards for the operations of buildings, transportation systems, and industrial equipment. These investments can reduce overall U.S. energy consumption by 30 percent relative to current levels. In most cases, the costs of these energy efficiency investments can be offset within an average of three years, followed by net positive financial gains. The remaining $110 billion per year would be invested in renewable energy that generates low to zero emissions—i.e., solar, wind, geothermal, small-scale hydro, and low-emissions bioenergy—which will raise overall U.S. production from these energy sources more than fourfold. Additionally, the U.S. Energy Information Agency, or EIA, estimates that the average cost for producing electricity from most clean renewable sources—including wind, hydro, geothermal, and clean bioenergy—will be at rough cost parity with most nonrenewable sources by 2017.

The report finds these investments will yield the following employment benefits:

- 4.2 million overall jobs created both by new investments and expanded levels of operations and maintenance

- 2.7 million net increase in jobs, even after estimated contractions in fossil fuel sectors

- Net employment expansion at all levels of pay in the U.S. labor market and a decrease in the unemployment rate by about 1.5 percentage points—e.g., from 6.5 percent to 5 percent within the 2030 U.S. labor market

We must significantly reduce demand for nonrenewable energy sources, including natural gas

CO2 emissions produced by burning oil, coal, and natural gas to generate energy account for roughly 75 percent of all U.S. and global greenhouse gas emissions. Reducing U.S. CO2 emissions by 40 percent within 20 years will therefore require major absolute reductions in U.S. consumption of oil, coal, and natural gas—about 60 percent for coal, 40 percent for oil, and 30 percent for natural gas. Based on careful review of currently available technology and economics, this report determines that such a transformed fuel mix, while ambitious, is entirely achievable without undue disruption to the security, reliability, or affordability of the domestic energy system and would provide a net gain to the U.S. economy.

To meet the 20-year emissions-reduction target, the following energy and economic policies are required:

- Reductions in fossil fuel consumption by approximately 60 percent for coal, 40 percent for oil, and 30 percent for natural gas

- Reduction of overall U.S. energy consumption by approximately 30 percent relative to current levels

- Raising overall U.S. energy production from low to zero emissions renewables by more than fourfold

- Reduction in oil imports to absorb most of the decline in U.S. oil consumption, which will bring a sharp decline in the U.S. trade deficit and favorable macroeconomic effects

- Transitional support for affected communities and workers hardest hit by the reduced U.S. consumption of coal and natural gas. The federal government therefore needs to provide major transitional support for workers and communities that are facing retrenchment in order to promote economic development and job opportunity in these impacted communities and regions.

- No expansion of nuclear energy supply; despite being an emissions-free source of electricity, nuclear energy is unlikely to experience major expansion in the next two decades, due to public-safety considerations and market concerns. This report concludes that nuclear energy’s contribution to the overall U.S. energy mix will therefore remain roughly constant.

These investments are the best path to achieving economically beneficial carbon emissions reductions

The report examines the three distinct pathways for the energy future of the United States: a Reference case of future emissions based on our current actions; an Aggressive Reference case of emissions stemming from substantially more assertive actions based on the current political and policy framework; and finally, the PERI-CAP case, which works backward from the IPCC goal noted earlier to outline a realistic framework of actions needed to achieve success.

The PERI-CAP case may face political challenges. It is not without cost. However, it is also a necessary and feasible way to stabilize the climate. In aggregate it will provide strong net benefits to the U.S. economy.

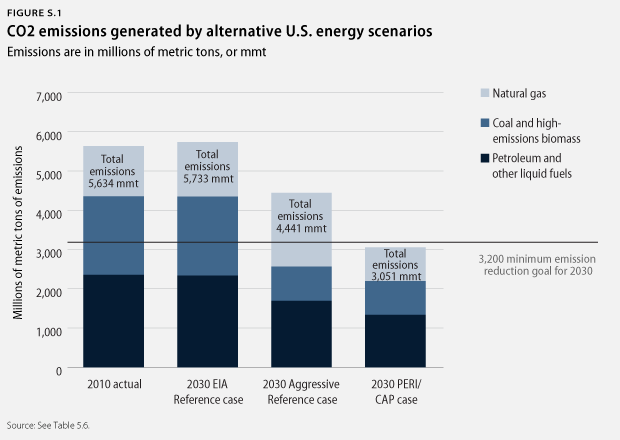

As Figure S.1 shows, this report found that in the Energy Information Agency’s Reference case for U.S. energy consumption in 2030—i.e., what the EIA regards as the most likely U.S. energy-sector conditions in 2030—CO2 emissions are at 5,733 mmt, or roughly 80 percent above the 20-year IPCC emissions-reduction goal.

The report then constructs a scenario based on the Aggressive Reference case—the full implementation of the best clean energy policies currently considered achievable within the near term without a change in the current political and policy debate. Assuming that these initiatives are all fully and successfully implemented, Figure S.1 estimates that U.S. CO2 emissions will be at 4,441 mmt, or 40 percent above the 3,200 mmt target level, under this case.

Finally, under the PERI-CAP case, we work backward from the IPCC goal to understand which technologies can produce a sustainable fuel mix within climate limits. We constrain these choices by the best available technical and economic research to ensure that this scenario is achievable using existing technologies under reasonably anticipated market conditions. The clean energy program we develop—through which overall annual U.S. energy consumption falls to 70 quadrillion BTUs within 20 years, with 15 Q-BTUs coming from clean renewable sources and 55 Q-BTUs from nonrenewables—will enable the United States to achieve the CO2 emissions-reduction target of no more than 3,200 mmt within 20 years. This is a decline of about 40 percent relative to current emissions levels of about 5,600 mmt.

There are four essential pillars to transforming our energy and environmental future

Building from existing policies at the federal, state, and municipal levels within the United States, we highlight four pillars, or policy categories, to promote a $200 billion annual shift in investment across the U.S. economy. These measures will be most effective when used in concert with each other.

- Market-shaping rules that level the playing field and build demand for new technology within energy, real estate, and financial markets. These include a carbon cap or tax, strict enforcement of the Clean Air Act, renewable energy standards and building codes, vehicle fuel-efficiency standards, and state and local regulation of electricity markets.

- Direct public spending, including government investments in energy efficiency retrofits for publicly owned buildings, major infrastructure systems, renewable energy procurement projects, and expanding federal research and development support for efficiency and renewable energy. Such public investment is crucial for setting the platform upon which individual market decisions are made.

- Private investment incentives that manage risk and improve access to capital for private investors at all levels of the economy and thereby make clean energy cheaper and more broadly accessible. These programs include restructuring clean energy production and investment tax credits, implementation of feed-in tariffs, financing green banks, and offering government loan guarantees.

- Regional equity and transitional support for communities and workers, which includes allocating federal government clean energy investment spending equitably among all regions of the country, targeted community-adjustment assistance, extensive worker-training programs, and adjustment-assistance programs for fossil fuel workers. The national clean energy investment program can itself provide a critical base for generating new opportunities among workers and communities that are presently dependent on the fossil fuel industries.

Stabilizing climate change requires a transformational shift in how we construct, finance, and deploy our energy infrastructure. This report quantifies that shift by outlining the challenging but feasible steps that can help restore a climate balance and increase overall U.S. employment in the process.

Robert Pollin is the Co-Director of the Political Economy Research Institute and a Distinguished Professor of Economics at the University of Massachusetts Amherst. Heidi Garrett-Peltier is an Assistant Research Professor at the University of Massachusetts Amherst. James Heintz is the Associate Director of PERI and the Andrew Glyn Professor of Economics at the University of Massachusetts Amherst. Bracken Hendricks is a Senior Fellow at the Center for American Progress.