Introduction and summary

Expanding Medicaid in states that have refused to extend this lifesaving health program would save more than 14,000 lives per year, according to new data compiled by the Center for American Progress. This is just one of the staggering benefits that CAP found in researching the far-reaching effects of Medicaid expansion in the states, including reductions in infant deaths, reductions in uninsured opioid-related hospitalizations, and earlier and additional cancer diagnoses. These new estimates underscore the lifesaving effects of Medicaid expansion and its role in combating some of the nation’s most deadly health crises. The estimates also demonstrate the extent to which expanding Medicaid in remaining states would reduce bankruptcies, enhance public safety, keep money in families’ pockets, and more.

Since the Affordable Care Act (ACA) was signed into law in 2010, 31 states and the District of Columbia have expanded Medicaid, extending health care coverage to low-income nonelderly adults. Virginia and Maine are slated to join them as soon as 2019.1 In November 2018, voters in four more states—Idaho, Montana, Nebraska, and Utah—will decide whether to follow suit.2

Overwhelming evidence shows how Medicaid expansion, which began in 2014, has substantially increased health insurance coverage and improved access to affordable care. As of 2016, Medicaid covered 11.9 million newly eligible Americans in expansion states, reducing the share of nonelderly adults without insurance in these states from 13.6 percent in 2013, the year before expansion, to 8.1 percent.3 A growing body of research also shows that Medicaid expansion’s benefits extend far beyond coverage and access to care: It also saves lives, reduces families’ chances of facing bankruptcy, and increases access to opioid addiction treatment, among other benefits.4

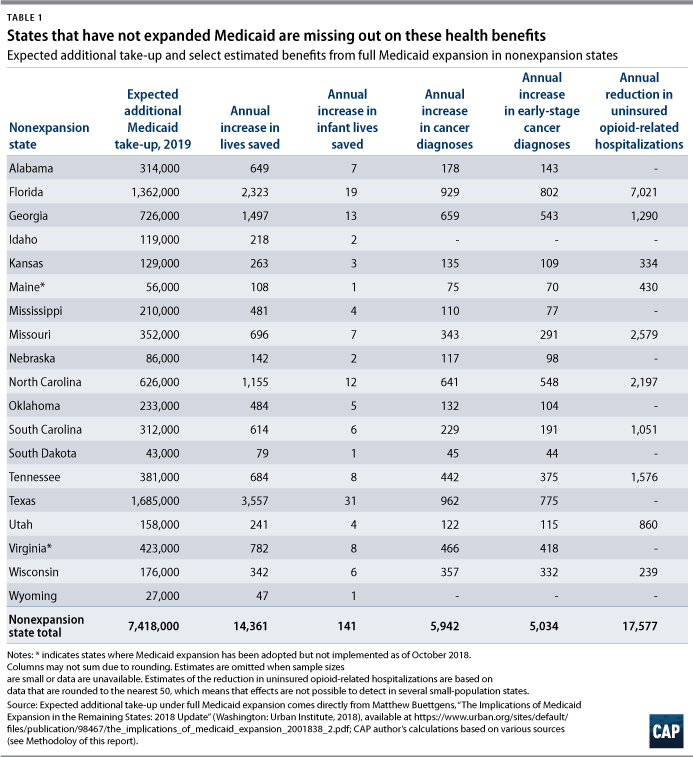

Yet in 17 states, lawmakers have blocked their constituents from sharing in these benefits. As of 2018, 18.4 percent of nonelderly adults in nonexpansion states lacked insurance; this rate is more than twice that of nonelderly adults in expansion states, at 8.7 percent.5 In their refusal to expand Medicaid, governors and state legislators not only continue to harm the 7.4 million Americans who would be enrolled in Medicaid in 2019 if expansion took place (see Table 1), but they also deprive their states’ residents of greater financial security, enhanced public safety, and longer lives.6 CAP estimates that if remaining states were to fully expand Medicaid, the benefits would include:

- Additional lives saved per year: 14,361

- Additional infant lives saved per year: 141

- Additional early-stage cancer diagnoses per year: 5,034

- Reduction in uninsured opioid-related hospitalizations per year: 17,577

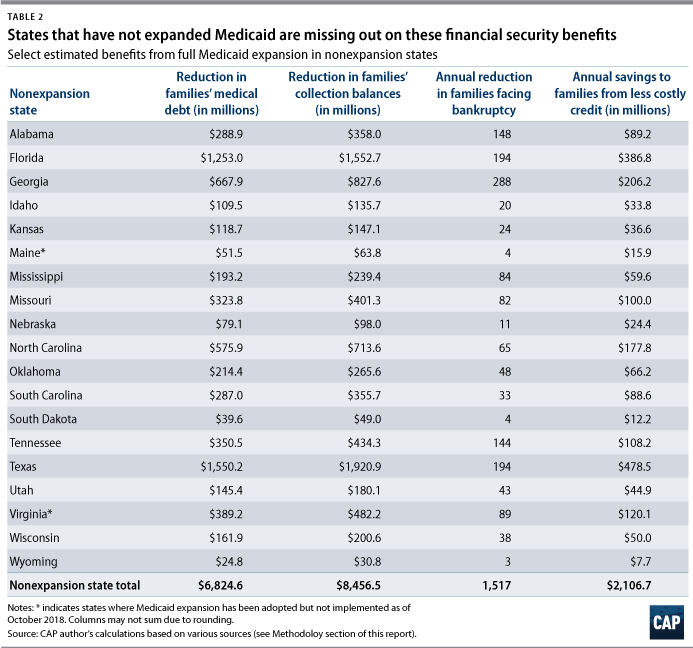

- Additional bankruptcies prevented per year: 1,517

- Reduction in families’ accrued medical debt: $6.8 billion

- Money kept in families’ pockets from less costly credit per year: $2.1 billion

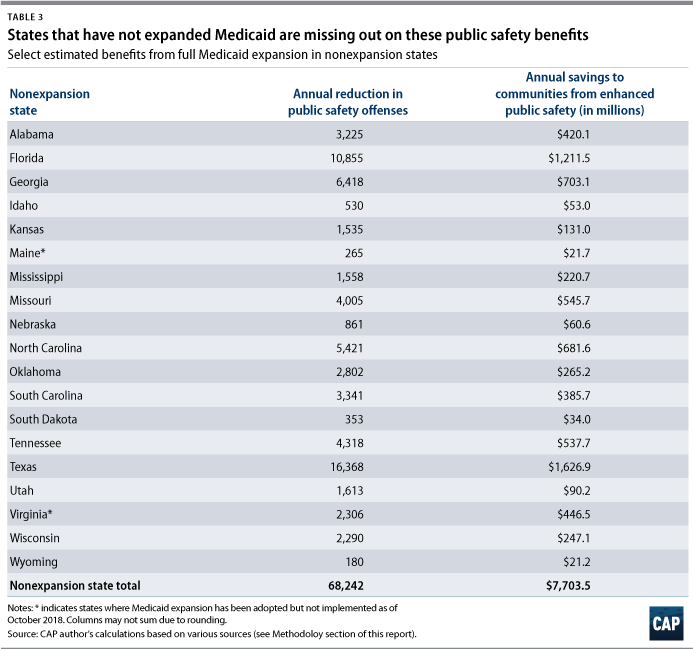

- Savings to communities from enhanced public safety per year: $7.7 billion

This report offers new numbers on how nonexpansion state lawmakers are holding their states back. It provides state-by-state estimates of the far-reaching benefits that each nonexpansion state could expect from expanding Medicaid based on multiple recent academic studies.7 As the positive evidence of Medicaid expansion’s effects continues to mount—and nonexpansion states are left increasingly far behind—residents of nonexpansion states deserve to know what their elected officials are denying them.

Health benefits of expansion

The United States tops the charts among high-income nations in the share of residents who report that they skipped seeing a doctor or forewent needed medical care due to cost, according to a Commonwealth Fund study of 11 countries.8 For millions of low-income adults, Medicaid expansion has fully or largely eliminated this cost barrier. Substantial research evidence has not only shown how expansion has improved insurance coverage and access to care, but it has also quantified its effect on multiple specific health outcomes.

Lives saved

Despite living in one of the world’s wealthiest nations, Americans live shorter lives in poorer health compared with their peers in other developed nations.9 What’s more, tremendous disparities in life expectancy by race, income, and geographic location mean that the length of an American’s life is tightly linked to her parents’ income, the color of her skin, and the ZIP code in which she grew up.10 A key factor in this dismal picture is that so many Americans must bear the sky-high costs of health care out of pocket—or forego critical care—because they cannot afford health insurance.11

By providing insurance to low-income, nonelderly adults—the group least likely to be insured—recent expansions of Medicaid have enabled millions more Americans to access preventative care and affordable treatments.12 This access has saved lives. In a 2017 study of New York, Arizona, and Maine, Dr. Benjamin Sommers of Harvard University’s T. H. Chan School of Public Health found that mortality fell in expansion states following Medicaid expansion—driven by a reduction in “health-care amenable deaths”—but rose slightly in nonexpansion states.13 Sommers estimated that one additional life was saved each year for every 239 to 316 adults who gained insurance. Applying the more conservative end of this estimate to the number of people who would gain coverage if the holdout states expanded Medicaid, CAP estimates that approximately 14,361 lives would be saved every year by expanding Medicaid.

Reduced infant mortality

Medicaid is critical to women’s health, including during pregnancy and childbirth. Women make up the majority of Medicaid beneficiaries in part because states are required to cover low-income women during pregnancy14 and because women are more likely be lower-paid and lower-income compared with men.15 Medicaid finances nearly half of all births in the United States.16 Unsurprisingly, Medicaid also plays a vital role in infants’ health at birth. Infants whose mothers are uninsured or sporadically insured are more likely to experience adverse outcomes such as low birth weight in part because their mothers receive fewer prenatal care services.17

While states were already required to cover low-income pregnant women regardless of whether they had adopted Medicaid expansion, research suggests that Medicaid expansion has had additional positive effects on ensuring access to critical prenatal and postnatal health care services. For example, a 2018 study found that Ohio’s Medicaid expansion significantly increased receipt of prenatal vitamins and guideline-concordant screenings by reducing instability in women’s insurance coverage before and after pregnancy, particularly among first-time mothers.18

Research by Florida International University researchers Chintan B. Bhatt and Consuelo Beck-Sagué in 2018 suggests that Medicaid expansion may have a modest but meaningful effect on infant mortality.19 In the years leading up to 2014, expansion and nonexpansion states experienced similar modest annual declines in infant mortality rates—but starting in 2014, expansion states made greater gains against infant deaths. In particular, the study reveals that among African American infants—who are twice as likely to die in infancy as non-Hispanic white infants20—the large 14.5 percent decline in mortality between 2010 and 2015 was more than double the decline in nonexpansion states.21 Using the same data source as Bhatt and Beck-Sagué’s study, Table 1 shows CAP’s estimate of the number of infant deaths that could be potentially averted in nonexpansion states. (see Methodology for details)

Earlier and more cancer diagnoses

Cancer is the second leading cause of death in the United States behind only heart disease. Multiple studies have linked Medicaid expansions to improved cancer-related outcomes;22 significant drops in uninsurance rates among both cancer patients and survivors, who often face ongoing high medical expenditures;23 and reduced disparities in insurance rates among survivors by race and ethnicity, income, and urbanicity.24

Research finds Medicaid expansion significantly increases the likelihood of cancer detection at an early stage, which increases survival and reduces treatment costs.25 A study of first-time cancer diagnoses among nonelderly adults in more than 600 counties conducted by Aparna Soni of Indiana University and others found that Medicaid expansion was associated with a 6.4 percent increase in early cancer diagnoses as well as a 3.4 percent increase in overall cancer diagnoses for this group.26 As Table 1 shows, based on Soni’s survey results, CAP estimates that expanding Medicaid to nonexpansion states could lead to more than 5,900 additional first-time cancer diagnoses—including more than 5,000 early-stage diagnoses—among nonelderly adults each year.

Expanded access to treatment and affordable care for opioid addiction

Each day in 2017, approximately 115 Americans died from an opioid overdose—a rate about five times greater than that in 1999.27 In recent years, opioid overdoses were responsible for more deaths than motor vehicle accidents and nearly twice as many as homicides.28 Combatting the opioid epidemic—which is ripping apart millions of families—requires a thoughtful, public health-focused policy response. Such a response must account for the needs of people living with chronic pain, many of whom rely on opioids to live and work,29 as well as communities of color, who often face discrimination in the medical system that can lead to inadequate and inequitable medical treatment.30 But it is clear that for both individuals struggling with opioid misuse disorder and people experiencing chronic pain, Medicaid expansion improves lives and health outcomes.31

The opioid crisis looms particularly large in nonexpansion states such as Maine, Florida, and Missouri, which had among the highest rates of overdose deaths in recent years.32 Opioid misuse disproportionately affects working-age adults33; in nonexpansion states, high rates of uninsurance among low-income working-age residents entails reduced access to substance abuse treatment and greater costs for uncompensated care. Analysis by the Center on Budget and Policy Priorities (CBPP) found that the uninsured rate for opioid-related hospitalizations dropped by nearly 80 percent in states following Medicaid expansion, compared with a decline of only 5 percent in nonexpansion states.34 CAP estimates show that uninsured opioid-related hospital visits would fall by nearly 18,000 each year if nonexpansion states adopted Medicaid expansion. (see Table 1)

Meanwhile, in expansion states, Medicaid expansion has proven a critical tool for combatting the opioid epidemic. According to the Government Accountability Office (GAO), health officials in these states report better access to health care and more widespread use of medication-assisted treatment for substance abuse.35 Additional research confirms this report: For example, Medicaid expansion was associated in a 13 percent increase in patients claiming buprenorphine with naloxone, a common and effective but costly medication-assisted treatment for opioid use disorder.36 Such improved access to affordable treatment options can be expected to save lives, boost workforce productivity, and restore communities that the opioid crisis has devastated. According to CAP estimates, if Florida and Georgia, two of the largest nonexpansion states, expanded, they would see roughly 3,200 more patients and 910 more patients, respectively, obtain needed buprenorphine with naloxone prescriptions each year. (see Methodology for full explanation)

Improved family financial security

A sizeable body of research has shown how Medicaid expansions preceding the ACA’s passage, such as those in Oregon and Massachusetts, substantially reduced financial distress along multiple dimensions—including lowering unpaid medical bills, delinquencies, third-party collections, bankruptcies, and payday loan use—while raising credit scores.37 Not surprisingly, recent research demonstrates that Medicaid expansion under the ACA has had similar benefits for families’ financial security in expansion states.

Fewer unpaid medical bills

In a 2015 survey, more than 1 in 4 American adults reported that they or someone in their household had experienced trouble paying medical bills in the previous 12 months; that share more than doubled to 53 percent among the uninsured.38 Having health insurance is not a guaranteed protection against unaffordable medical bills, but in most states, Medicaid enables recipients to access health services at very low cost. The capacity of Medicaid to reduce crushing medical burdens was borne out in the so-called Oregon health insurance experiment; the state’s 2008 expansion almost completely eliminated catastrophic expenditures—that is, out-of-pocket expenditures greater than 30 percent of household income—among enrollees.39

Researchers Kenneth Brevoort, Daniel Grodzicki, and Martin B. Hackmann examined millions of credit card records, finding that Medicaid expansion decreased the amount of newly accrued medical debt by 30 percent to 40 percent among enrollees, with a particularly large impact on catastrophic medical debt.40 They estimate that when averaged across all people who gain coverage, Medicaid expansion reduced accrued medical debt by about $920 per person, which CAP estimates could save Americans in nonexpansion states more than $6.8 billion.

Reduction in collection balances

Because uninsured Americans often struggle to pay their medical bills—or to pay their other nonmedical-related bills while meeting medical costs—they are significantly more likely to become delinquent on their bills and have their debt sent to third-party collection agencies. Medicaid expansion reduced this distress. Using a nationally representative sample of millions of credit reports for 19- to 64-year-olds, Luojia Hu of the Federal Reserve Bank of Chicago and her colleagues found that, on average, collection balances dropped by about $1,140 per person who gained coverage.41 These reductions in collection balances were greatest in local areas with the greatest share of uninsured, low-income residents.

Bankruptcies prevented

For families facing crippling medical debt, bankruptcy may be the only way out despite the damage it inflicts on credit scores. Medical bills have been one of the largest contributors to personal bankruptcy in recent decades, particularly prior to the ACA’s passage.42 Medicaid expansion has reduced bankruptcies—potentially because it has dramatically reduced medical debt—particularly among some of the most financially vulnerable families. Brevoort, Grodzicki, and Hackmann estimate that Medicaid expansion prevented 50,000 bankruptcies among those with subprime credit scores—scores lower than 620—in the two years after it was enacted.43 And tracking adults who newly gained coverage in Michigan, Sarah Miller of the University of Michigan and her colleagues found that the number of bankruptcies decreased by 10 percent. As Table 2 shows, if nonexpansion states experienced a similar effect upon expansion, the number of bankruptcies among new Medicaid recipients would shrink by about 1,500, based on CAP estimates.

Savings to families from greater access to less expensive credit

Bankruptcy, unpaid medical bills, and other debts that arise from a lack of insurance not only directly create hardship and stress, but they also indirectly inflict harm by reducing families’ access to credit markets. Thus, a family’s inability to pay bills may make it costlier—or even impossible—for them to borrow to meet other needs such as a mortgage or emergency expenses or to invest in education.

By contrast, when families are better able to afford their medical bills, they also gain greater access to credit at less expense. Indeed, a 2017 study showed that Medicaid expansion reduced new delinquencies on debt by 30 percent, indicating that expansion significantly reduced financial distress.44 Other studies found that Medicaid expansion led residents to be 16 percent less likely to overdraw their credit cards and 18 percent less likely to have credit scores below 500.45 They are also less likely to need to turn to costly predatory loans. A study of California counties that adopted Medicaid expansion early found that expansion decreased the number of payday loans taken out in the early-adopting counties by 11 percent, in addition to reducing the numbers of borrowers and the amount of debt.46 By enabling families to meet their medical costs, reducing their debt burden, and placing them on firmer financial footing, Medicaid expansion has increased families’ credit scores.

As a consequence of greater creditworthiness, banks and other lenders charged individuals in expansion states lower interest rates, which lowered their payments on items such as credit cards, personal loans, auto payments, and mortgages compared with their nonexpansion-state counterparts. Brevoort, Grodzicki, and Hackmann found that savings from reduced interest costs averaged about $284 per year for each adult who gained Medicaid coverage. Table 2 displays the potential annual savings for consumers in each nonexpansion state.

Enhanced public safety

Over the past decade, the criminal justice reform movement has sought to address the nation’s shameful legacy of mass incarceration and overcriminalization, which has left 1 in 3 adults—an estimated 70 million to 100 million Americans—with a criminal record.47 A comprehensive plan to address this legacy requires removing the many barriers that people with criminal records face—including barriers to employment, housing, income supports, health care, and more.48

Prior to the ACA’s passage, most working-age adults’ access to affordable health care was overwhelmingly dependent on their employment status.49 As a consequence, Americans who face barriers to employment—including due to labor-market discrimination or having a criminal record—often had little access to health care and to services they needed to enter the job market or maintain stable employment. This includes individuals who may need to access mental health services or substance abuse treatment to have a chance at successful re-entry into their communities.50 Furthermore, for individuals who are involved in the justice system, even when they are able to overcome obstacles to employment, they are disproportionately likely to work in low-paying, low-quality jobs that do not provide health care.51

By removing a major barrier to re-entry—as well as to needed medications, mental health services, and substance abuse treatments—for low-income working-age adults, whom the justice system disproportionately affects, Medicaid expansion has enhanced public safety. For example, research by Qiwei He of Clemson University finds that Medicaid expansion led to a statistically significant drop in five types of offenses, including a 3.6 percent drop in burglaries and a 10 percent drop in motor vehicle theft.52 Author He’s results are consistent with substantial previous research finding that interventions that support and raise living standards for low-income individuals and families—such as raising the minimum wage and expanding the earned income tax credit and nutrition and cash assistance—led to greater public safety by improving financial stability and increasing access to critical, stabilizing medical services.53

As a result, Medicaid expansion has saved billions of dollars in American communities.54 Based on estimates of the social cost of crime, implementing Medicaid in nonexpansion states would save communities in these states $7.7 billion each year. (see Table 3)

Conclusion

Medicaid expansion under the ACA has vastly increased coverage and access to affordable care for the nation’s least-insured population. In the 17 states where policymakers have refused to expand Medicaid, residents are not only less likely to have insurance or be able to afford needed health care, but their communities are also being denied a host of benefits such as earlier cancer diagnoses, greater access to opioid-related treatments, and relief from medical debt.

Indeed, Medicaid expansion is nothing short of lifesaving and could prevent an additional 14,000 deaths each year in nonexpansion states. As policymakers seek to address major health, economic security, and public safety challenges in their states, they should look first to this simple solution: Expand Medicaid.

Methodology

This Methodology describes the author’s approach to estimating each of the outcomes offered in the tables above. The analysis includes estimated outcomes for Virginia and Maine even though these states have already elected to expand Medicaid because expansion has not yet taken effect.

Throughout this analysis, the author relies on two state-level forecasts from the Urban Institute: 1) the total number of individuals—whether currently uninsured, underinsured, or otherwise insured—who would newly take up on Medicaid coverage in 2019 if Medicaid were expanded in remaining states; and 2) the number of currently uninsured individuals who would take up on Medicaid if it were expanded in remaining states.55 In order to provide relatively current estimates for nonexpansion states, this analysis uses the most up-to-date base data available. For example, when state populations are required for the procedure, the analysis uses the 2017 American Community Survey (ACS) 1-year estimates. While estimates are intended to be appropriate for 2019 and other near-term years, this analysis does not attempt to forecast population, household, or other base data into 2019 and beyond. Estimates given in annualized terms should be expected to change somewhat in future years based on changes in population and other factors, with greater certainty in the near-term than in the out-years. Monetary figures cited in the text generally represent current values as of 2015 to 2017, depending on their source; using these values in estimates produces conservative values compared with 2018 dollars.

Extrapolating from the findings of empirical research frequently requires making assumptions, and often there is more than one reasonable possible approach. In such cases, the author chose among the alternatives so as to produce a more conservative estimate of expansion’s effects.

Lives saved

In his 2017 study, Sommers finds that Medicaid expansion reduced all-cause mortality for individuals ages 20 and 64, with roughly 1 life saved annually for every 239 to 316 adults gaining insurance after being uninsured.56 The author of this report applied the more conservative end of this range, 316 adults, to estimates of newly covered individuals upon expansion from the Urban Institute.

Reduced infant mortality

Following Bhatt and Beck-Sagué, the author estimated the reduction in infant mortality rates due to Medicaid expansion.57 First, the author verified that expansion and nonexpansion states experienced similar trends in the pre-expansion period and found that, indeed, between 2010 to 2013, both sets of states saw modest annual decreases of similar sizes in their infant mortality rates. The author then calculated the simple difference-in-difference estimator for expansion states and nonexpansion states in the immediate pre- and postexpansion years, 2013 and 2015, following CBPP’s analysis of Medicaid expansion and opioid-related hospital visits in excluding from the estimation procedure states that were early or late expanders—that is, states that did not expand starting January 1, 2014. This yields a more conservative estimate than using Bhatt and Beck-Sagué’s data points, suggesting that Medicaid expansion was associated with a roughly 1.4 percent rather than 3.0 percent reduction in infant mortality.58 Finally, the author applied this decrease to state-level infant mortality data in nonexpansion states from the Centers for Disease Control and Prevention (CDC) for 2016, the latest year of data available.59

Earlier and more cancer diagnoses

The author obtained cancer diagnoses by stage, age, and state for 2015, the most recent year of data available, from the National Cancer Database (NCDB).60 Following Soni and her co-authors, who studied first-time cancer diagnoses among patients aged 19 to 64, this analysis approximates diagnoses among this group using the NCDB. Because the NCDB aggregates patient data in decade-wide age groups, this analysis omits diagnoses among 19-year-olds and includes half of diagnoses among the 60–69 age group. Based on Angela Mariotto and others, who found that the roughly 8 percent of cancer patients of all ages had been affected by more than one form of cancer, this analysis assumes that roughly 92 percent of diagnoses among adults ages 19 to 64 were first-time overall and early diagnoses.61 This is likely a conservative estimate because approximately 60 percent of cancer survivors are age 65 and older.62 The author applies a 3.4 percent and 6.4 percent decrease to overall and early diagnoses, respectively, to estimate postexpansion reductions in each type of diagnosis, based on Soni and others.63 The author defined early diagnosis in the NCDB as diagnoses made in Stage 0 or Stage I, which is intended to align with Soni and others’ definition of early diagnosis in the Surveillance, Epidemiology, and End Results (SEER) Program data as “in situ, local, or regional by direct extension only.”64 The early diagnosis estimates may be conservative because the dataset Soni and others’ use to estimate the sensitivity of early diagnoses to Medicaid expansion—from the NCI’s SEER Program—is representative of the entire population of each state it covers, while the NCDB is a hospital-based registry and thus may not capture cancer diagnoses made outside of hospitals. SEER data, however, are only available for a limited number of nonexpansion states.

Expanded access to treatment and affordable care for opioid misuse disorder

Estimates of the decrease in uninsured opioid-related hospitalizations are based on CBPP analysis.65 Following CBPP, the author used data from the Healthcare Cost and Utilization Project (HCUP) at the Agency for Healthcare Research and Quality to calculate the share of all in-patient opioid-related hospitalizations by state and discharge quarter in 2013 and 2015—the years spanning Medicaid expansion.66 Like CBPP, the author combined data for the first three quarters of the year due to the cyclicality in opioid-related hospitalizations. Since HCUP data are rounded to the nearest 50, estimates for low-population states such as Wyoming, Nebraska, and South Dakota are excluded. The author calculated a basic difference-in-difference estimator between these two time periods, which suggests that expansion was responsible for a reduction of 9.6 percentage points in uninsured hospitalizations in expansion states, a 71.6 percent reduction. This analysis approximates a seasonally adjusted number of annual hospital visits in nonexpansion states in 2015—the most recent year for which data in all states is available—by assuming that seasonally adjusted Q4 visits were effectively the average of Q1–Q3 visits. Finally, it applies the 71.6 percent reduction to estimate the drop in uninsured hospital visits in nonexpansion states.

To gauge improved access to treatment, this analysis uses 2018 estimates from Brendan Saloner and others, who find that patients receiving buprenorphine with naloxone in the population increased by roughly 13 percent due to Medicaid expansion.67 Two of the study’s co-authors, Saloner and Jonathan Levin, provided CAP with unpublished base levels of buprenorphone with naloxone claims in the population in Florida and Georgia in 2015. Assuming that the three Medicaid expansion states are valid counterfactuals for the trends in Florida and Georgia and that the rate of buprenorphone with naloxone use in the population has been relatively stable in these two states in recent years, the author used the latest available population for those two states from the 2017 ACS 1-year estimates to estimate the number of additional patients who would use buprenorphone with naloxone if Medicaid were expanded.

Fewer unpaid medical bills

Based on 2017 estimates by Brevoort, Grodzicki, and Hackmann— and assuming that average pre-expansion medical debt for the expansion population was roughly equivalent in expansion and nonexpansion states—this analysis assumes that expansion would reduce newly accrued medical debt by $920 for each person gaining Medicaid coverage per year on average.68

Reduction in collection balances

Based on estimates by Hu and her co-authors, this analysis presumes that expansion would reduce the average collection balance by about $1,140 per person who gained Medicaid coverage.69 This approach implicitly assumes that the average pre-expansion collection balance among the expansion population was roughly equivalent in expansion and nonexpansion states. However, according to Hu and her co-authors’ Table 1, the average collection balance from 2010 to 2013 was larger in nonexpansion states than in expansion states—$480 compared with $333. Given that collection balances likely have further to fall in nonexpansion states than they did in expansion states, the present approach may yield a conservative estimate of reductions in collection balances.

Bankruptcies prevented

The author obtained cumulative bankruptcy filings by state in 2017 from the American Bankruptcy Institute and combined Chapters 7 and 13 bankruptcies, the most common types of bankruptcies undergone by people rather than corporations.70 Assuming that bankruptcies typically occur at the household rather than the individual level, the author calculated the rate of bankruptcies per household in each state using data on the number of households obtained from the 2017 ACS 1-year estimates.71 The author then translated the number of individuals in nonexpansion states who would newly gain health care coverage under Medicaid expansion into a number of households by obtaining the median family size for 18- to 64-year-olds who had household incomes of 138 percent of the federal poverty level or less in nonexpansion states, also using the 2017 ACS 1-year estimates. To produce a conservative estimate, this analysis calculates family size among all low-income working-age adults rather than only those with dependent children. While Medicaid expansion is often characterized as targeting adults without dependent children, because parents were eligible for Medicaid prior to the ACA’s passage, the income thresholds for parents’ eligibility remain quite low in many nonexpansion states.72 Assuming that households with individuals transitioning from uninsured to Medicaid experience personal bankruptcy at the same rate as other households—likely a conservative assumption, considering that these low-income households tend to be more financially vulnerable—the author estimated the number of bankruptcies associated with these households. Finally, the author applied a decrease of 10 percent, consistent with Sarah Miller and her co-authors’ findings, to estimate the number of personal bankruptcies prevented by expanding in nonexpansion states.73

Savings to families from greater access to less expensive credit

This analysis applies results from Brevoort, Grodzicki, and Hackmann by presuming the savings from reduced interest costs would average about $284 per year for each individual who would newly gain Medicaid coverage in nonexpansion states.74 In doing so, this analysis presumes that the average cost of credit for the expansion population was roughly equivalent in expansion and nonexpansion states prior to expansion. This seems reasonable based on the similarity of offered credit card interest rates in expansion and nonexpansion states in the period before expansion, since a reduction in credit card interest was the largest driver of postexpansion savings in the study.75 Furthermore, because average credit scores were about 2.5 percent lower in nonexpansion states76 and rates tend to be higher for individuals with lower credit scores, an average savings of $284 per newly covered individual may be a conservative estimate.

Enhanced public safety

Beginning with 2016 Universal Crime Reporting system data by state and type of crime from the FBI,77 this analysis applies the results of He’s 2017 study, which finds statistically significant reductions in five types of offenses (burglary, motor vehicle theft, criminal homicide, robbery, and aggravated assault) due to Medicaid expansion.78 (He does not explore the effect of Medicaid expansion on rape and finds only a small but statistically insignificant reduction in larceny theft. To produce a conservative estimate, the author excluded these two types of offenses.) Based on He’s reported values of the social cost per offense for each of these five offense types, expressed in 2017 dollars, the author estimated the annual social savings in each state.79

Acknowledgments

The author would like to thank Donovan Hicks and Sai Nikitha Prattipati for their excellent research assistance. The author would also like to thank Emily Gee, Katherine Gallagher Robbins, Heidi Schultheis, Aparna Soni, Brendan Saloner, and Jonathan Levin for their policy expertise and guidance.

About the author

Rachel West is the director of research for the Poverty to Prosperity Program at the Center for American Progress.