The Tax Cuts and Jobs Act (TCJA) was introduced on November 2, 2017, rushed through Congress on a partisan basis, and signed by President Donald Trump just seven weeks later. No hearings were held on the actual bill and experts who could have helped ensure that provisions were properly drafted had barely any opportunity to digest legislative language or analysis from the Congressional Joint Committee on Taxation, much less to provide comments. Additionally, Democratic legislators were not permitted in the drafting room. The result is a bill riddled with drafting errors, special tax breaks that were not vetted, and new loopholes.1 While some are mere glitches, others appear to be purposeful giveaways that will create complexity and confusion for taxpayers and will have a significant impact on federal revenues.2

Most tax policy experts understand tax reform to involve making the tax system fairer, as well as simpler and more efficient where possible.3 This is achieved in part by eliminating special interest tax breaks and loopholes that allow savvy taxpayers to legally escape tax.4 This approach contributed to the success of the Tax Reform Act of 1986.5 While it will take time before the full ramifications of the TCJA are fully revealed, it is clear at this point that the effort did not result in true tax reform. Rather, while some special interest tax breaks and tax loopholes were eliminated or reduced, a host of others were left in place. And new breaks and loopholes were added that individuals and businesses, with the help of their sophisticated tax advisers, can use to avoid paying taxes in the years ahead.6 This issue brief provides a sample of the many special tax breaks that remain or were added to the tax code, along with some new loopholes that have been identified in the two short months since the bill was passed.

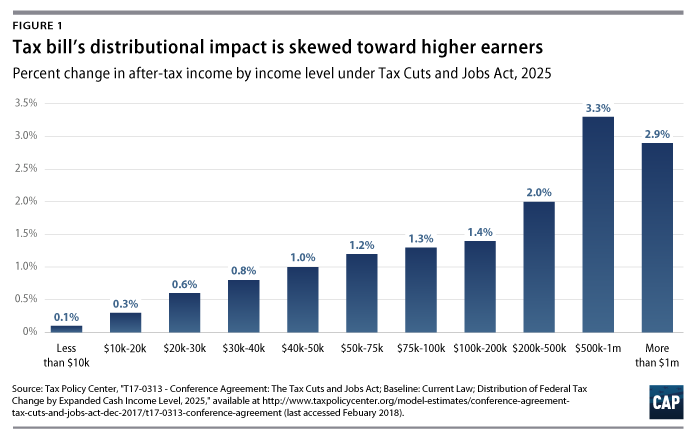

The core elements of the TCJA—and, in particular, its rate cuts—create a significant tilt towards the wealthy and large multinational corporations. Even in 2025 when TCJA’s temporary individual tax cuts are in full effect, higher-income taxpayers will see a much larger increase in after-tax income than working and middle-income families.

And much of the benefit that the wealthy and corporations receive as a result of the tax law is permanent, whereas much smaller benefits to low- and middle-income taxpayers are temporary and, in fact, will be replaced several years from now with tax increases.7 Moreover, this law fails to create the economic incentives promised.8 The international tax provisions appear to encourage more offshoring of operations, and, because the tax cuts in the bill were not fully offset, the new law is expected to add at least $1.5 trillion to federal budget deficits over the next decade.9 This enormous cost will be shifted onto everyone else, either through dramatic cuts to middle class priorities, such as health care, education and housing, or more tax increases in subsequent years.

The special interest tax breaks and loopholes in the post-TCJA tax code exacerbate these fundamental inequities at the heart of TCJA. The benefits of the special breaks and loopholes will redound almost entirely to the wealthy and corporations, coming on top of the basic structure of the bill that is best for those at the top. These breaks and loopholes are too numerous to list, and additional loopholes created by the new law are bound to surface as tax experts continue analyzing and implementing the law. Thus, the provisions described in this brief are merely intended to illustrate the TCJA’s impact, rather than provide a complete accounting of them.

Special interest provisions

President Trump promised to “drain the swamp” and claimed that his tax proposals would not benefit wealthy people like him. House Republicans said the plan would fight “special interest subsidies and crony capitalism.”10 Yet, tax provisions that provide special treatment to one interest group or another remain in the tax code following enactment of the new law. Even worse, new special interest provisions were added.

The carried interest loophole is still there for private equity firms

During his campaign and many times since he was elected, President Trump promised to close the so-called carried interest loophole.11 For years, private equity fund and hedge fund managers have used the loophole, claiming that a large portion of the fees they earn are investment income eligible for the 20 percent capital gains tax rate rather than ordinary income subject to the top marginal rate: 39.6 percent in 2017 and now, 37 percent under the new tax law. Despite President Trump’s promise, the carried interest loophole remains intact, with only a minor change—investment management firms will have to hold assets for at least three years before being able to use the 20 percent long-term capital gains tax rate. For most private equity fund managers, the three-year rule is virtually meaningless because they hold assets for five years on average.12 Meanwhile, those who tend to hold assets for shorter periods of time are looking for ways to get around the new rule, such as by arranging to have their fees paid to separately-created S corporations, which, because of ambiguous language, may not be subject to the three-year holding period.13

Fossil fuels win big

The new tax law fails to eliminate a number of decades-old tax breaks that are specifically aimed at the oil and gas industry and, considering the industry’s profitability and the recent rise in crude oil prices, are definitely not justified.14 Those tax breaks include the oil depletion allowance, which effectively enables an independent oil and gas firm to write off more costs than it incurs, as well as a tax break for intangible drilling costs.15 Also untouched is the 15 percent tax credit for enhanced oil recovery and a provision that enables huge oil and gas pipeline companies to use master limited partnerships (MLPs), a form of business organization that enables them to avoid the corporate income tax. The investors in MLPs will now also enjoy a reduced tax rate on their profits under TCJA. Also, under the new tax law, big oil and gas corporations will benefit from reduced tax rates on previously untaxed earnings they have been holding offshore, as well as the reduction in the corporate tax rate for future profits and the new international tax regime, which generally exempts dividends from foreign subsidiaries of a U.S. corporation. All of these firms also benefit from the 100 percent expensing for business purchases allowed in the bill for the next five years. And the largest exploration and production firms ultimately will benefit from a provision in the tax law that reverses four-decade policy by allowing the Interior Department to lease land in the Arctic National Wildlife Refuge for gas exploration activities.16

Commercial real estate developers get even more than before

While the increase in the standard deduction and the limitation on the mortgage interest deduction may have some effect on the residential real estate market, the industry that made President Trump rich—commercial real estate—retained and, in fact, increased its special treatment under the tax code.17 To begin with, large corporate real estate operating firms will reap large benefits from the cut in the corporate tax rate to 21 percent as well as the elimination of the corporate alternative minimum tax. But the many real estate businesses organized as partnerships or S corporations—so-called pass-through entities because their income is not subject to the corporate income tax, only the individual income tax—will benefit overwhelmingly from the many special rules for real estate in the new tax law.18

- Special low rate on real estate business income. Real estate is favored under the new 20 percent deduction for income from a partnership, S corporation, or sole proprietorship. The deduction effectively lowers the tax rate on this type of business income from the new top individual tax rate of 37 percent down to 29.6 percent. While many service businesses are expressly prohibited from this new deduction, real estate businesses are not on the list of those excluded. Moreover, a special rule was added to the law during eleventh-hour negotiations that effectively enables real estate businesses (and other businesses with depreciable tangible property) to sidestep a limitation on the deduction designed to channel the tax benefit toward businesses that employ more workers.

- Favorable treatment for REITs. Real Estate Investment Trusts (REITs) are companies that hold ownership shares in commercial real estate ventures and receive income from rental properties. They must distribute most of their earnings as dividends each year to the shareholders. A number of provisions in the new law provide special new treatment for REITs. For example, REIT shareholders may deduct 20 percent of qualified dividend income from the REIT regardless of the amount of their income. In addition, wealthy individuals who take out a loan to invest in a REIT can deduct the interest on that loan against their ordinary income, which provides relief from the top 37 percent tax rate.19 Yet, those same individuals can treat the income from the REIT investment as business income against which they can take the 20 percent pass-through deduction, resulting in a maximum tax rate of 29.6 percent.

- Special treatment under limit on deductibility of interest expense on business debt. For businesses with average annual gross receipts of $25 million or more, the new law limits the amount of interest expenses on business debt that can be deducted but excludes an “electing real property trade or business,” which is defined broadly to include any “real property development, redevelopment, construction, reconstruction, acquisition, conversion, rental, operation, management, leasing, or brokerage trade or business.”20 A real estate firm that elects not to be subject to the interest expense limitation may not avail itself of the temporary provision allowing full expensing of capital purchases, but the latter expires after five years anyway while the election out of the interest expense deduction appears to be permanent.

- Like-kind exchange retained for real estate. Normally, when a business sells property, it must recognize as taxable income any net gain from the sale. Up until now, Section 1031 of the Internal Revenue Code permitted businesses to instead exchange property for similar assets without recognizing any gain, so long as they met certain requirements. The new tax law eliminated the ability of businesses to make tax-free exchanges of business property under IRC Section 1031. But the provision was retained for real property, allowing those in the real estate investment business to continue trading properties without tax consequences. So, for example, now rental car businesses can no longer roll over their vehicle fleet tax-free, but rental housing owners can exchange their properties tax-free.

Big alcohol

The TCJA provided a two-year reduction in excise tax rates on beer, wine, and spirits. The cuts were described as benefitting small craft brewers and distillers, but in reality, they also extend to large industrial producers as well as importers. In fact, out of the $4.2 billion cost of the alcohol excise tax cuts, only about $100 million will go to American craft producers.21 And, since those small craft producers already enjoyed a lower rate than larger producers, the provision seems clearly intended for the big producers and importers. The wisdom of these excise tax cuts is even more questionable given the costs of alcohol consumption. According to a Centers for Disease Control and Prevention study, excessive alcohol consumption costs the U.S. economy $249 billion annually, including losses from workplace productivity, health care expenses, law enforcement-related expenses, and vehicle crashes.22

Wealthy heirs keep their stepped-up basis loophole along with weaker estate tax

Normally, when a person sells an asset, they pay income tax on any net gain over their basis in the asset, that is, what they originally paid for it. But, when a person holds onto a valuable asset until they die, no income tax will ever be due on the gain that accrued during their lifetime. This is because their heirs are permitted to step up their basis in the asset to the market value at the time they inherit it. If the heir subsequently sells the asset, they will only pay income tax on any gain since the date they inherited it. This is referred to as stepped-up basis. But the estate tax acts as a backstop or limit on this benefit because it imposes a separate tax on those assets to the extent their value exceeds a specified amount. That amount was roughly $5.5 million per individual or nearly $11 million per couple prior to the TCJA. Previously, when estate tax repeal has been proposed, law makers have correspondingly proposed repealing the stepped-up basis rule to ensure that gain on assets held by very wealthy people are taxed at some point. But the TCJA doubled the estate tax exemption amounts without changing stepped up basis. Less than 1 in 1,000 estates will be subject to the estate tax, at least until 2026, as the estate tax will only apply to the amount that an estate exceeds $11 million per individual or $22 million for a married couple.23 And because the stepped up basis rule was left untouched, any gain on estate assets that accrued during the decedent’s lifetime will pass completely free of income tax.

New loopholes for legal tax avoidance

It is challenging to create a tax system that has no loopholes at all, especially given the complexity of investments made by the wealthy and of business transactions generally. Thus, it is important for drafters of tax legislation to engage the assistance of neutral tax experts and to vet draft tax legislation broadly so that potential problems can be identified and eliminated before the bill becomes law. Occasionally, loopholes will occur even from the best process, but where good tax policymaking process is absent, loopholes can proliferate. Such is the case with the TCJA. Even some loopholes that tax academics managed to identify in the course of the rushed process of passing the TCJA were ignored. What follows are examples of loopholes in the tax code post-TCJA.

The big pass-through loophole just got bigger—much bigger

Large pass-through businesses already enjoyed a much lower effective tax rate overall than similar businesses organized as C corporations,24 so it is discouraging that the TCJA creates a hefty new tax break for these businesses. Structured as a deduction of 20 percent of pass-through business income, the provision has the effect of reducing the top tax rate on pass-through income from the pre-2018 rate of 39.6 percent down to 29.6 percent.25 The rules outlining which businesses can take the deductions and which cannot are illogical and needlessly complex. Nevertheless, since the new top individual income tax rate is 37 percent, this creates an enormous incentive for higher-income individuals to recharacterize their ordinary income as pass-through business income. Experts already have identified many ways that this potentially could be accomplished.26 For example, law firms could create a separate pass-through entity that would own their office buildings, then the firm could make lease payments to the real estate entity. The real estate entity could use the 20 percent pass-through deduction to lower tax on the lease income; meanwhile, the law firm could deduct the lease payments as a business expense.27 In fact, approaches like this could become so popular that consulting firms could begin promoting quick business conversions for a fixed fee.28 Another possible loophole would involve a business that does not qualify for the deduction combining with one that does, in hopes that all of the income will qualify. For example, a business based primarily on the reputation of the owner, which the law expressly states does not qualify, could combine with a real estate business, which does qualify, thus making it appear that all of the income qualifies for the deduction.29

In yet another loophole under the new pass-through business deduction, owners of S corporations have to subtract their reasonable compensation in calculating the amount of the deduction, but partnerships and sole proprietorships apparently do not. Unless and until fixed, this loophole means that partnerships may be the preferred pass-through for anyone considering setting up a business to avail themselves of the deduction, as this may result in a larger tax deduction.

C corporations as tax shelters—again

In the 1970s, when the top individual tax rate was much higher than the tax rate on corporations, high-income individuals could create a corporation and hold their assets so that gains are taxed at the lower corporate rate.30 This loophole could end up costing the Treasury a great deal more than anticipated, since large pass-through businesses, which can easily switch to being taxed as C corporations, currently earn most business income.31

Offshoring operations and jobs

Perhaps the most complex provisions in the new tax law are those governing offshore profits of U.S.-based multinational corporations. The law eliminates most tax on offshore profits but then sets up several new tax regimes affecting offshore profits. Proponents of the bill claim that they have adopted a territorial tax system in which no U.S. tax is imposed on profits that U.S.-based multinationals earn abroad. But at the same time, the law creates additional tax measures supposedly designed to prevent U.S. companies from shifting profits offshore to avoid U.S. tax; impose tax on very high offshore profits; and encourage companies to keep their patents and other intangible assets in the United States. In reality, the new system fails to create the incentives its drafters promised.32 Countless tax experts have highlighted the perverse incentives from this new approach to international taxation.33 While the statutory corporate tax rate is indeed lower, analysis of the effective tax rates applicable to domestic and foreign profits shows that the effective rates on the latter are somewhat lower. And, since the legality of the provisions under World Trade Organization rules has been questioned by the EU and others,34 corporations uncertain about their future seem unlikely to move operations in response to the new law. In fact, the new law creates a new incentive—or loophole—for moving real operations offshore to shelter more offshore intangible income.35

Conclusion

The U.S. tax system was flawed before passage of the TCJA. However, the law addresses very few of these preexisting flaws, and in many cases exacerbates them. Numerous special interest provisions that existed in the tax code before are still there—and new ones have been added. Loopholes that enabled the wealthy and big business to legally shirk their taxes have been left in place or widened, and new ones have been created. If these special breaks and loopholes had been eliminated, the tax bill would not have added $1.5 trillion to federal budget deficits over the next decade. Both the cost of these provisions and the perverse incentives they create will undermine any claims by the law’s drafters that it will make the United States more competitive and create more jobs.

The result of this colossal failure to enact positive policy reforms to the tax code almost certainly will be a decrease in fairness for the working and middle class and an increase in complexity and confusion for individuals and businesses alike. Additionally, it will encourage corporations to shift jobs offshore and exacerbate the already substantial income and wealth inequality that exists in our country.

Alexandra Thornton is the senior director of Tax Policy for Economic Policy at the Center for American Progress.