In 2015, more than 1,000 natural disasters inflicted some $100 billion worth of economic damages around the world. These natural disasters included severe storms, flooding, extreme temperatures, droughts, and wildfires—all of which are expected to increase in frequency for years to come as a result of climate change. The annual number of such extreme weather events has been increasing, with almost three times as many occurring worldwide from 2000 to 2009 as in the 1980s.

Of the total economic losses endured last year from natural disasters, insurance covered only 30 percent. The majority of uninsured losses occurred in developing countries across Africa, Asia, and South America. In Asia, only 8 percent of losses from natural disasters were insured in 2015, and in Africa, only 1 percent of such losses were insured. Without such risk management tools, governments and individuals are less able to prepare for, respond to, cope with, and recover from climate-change-fueled weather events and natural disasters. While insurance can take many forms, risk management in particular includes a lack of access to innovative insurance instruments—such as parametric risk insurance, which is specifically designed to pay out quickly in the aftermath of a natural disaster. This gives countries a rapid injection of capital that can be vital in the early window before overseas assistance is effectively ramped up and delivered.

To help address this shortfall, the private sector, national governments, and international financial institutions and organizations are working to build new partnerships aimed at enabling countries that are particularly vulnerable to climate change and related natural disasters to gain access to climate-related risk insurance. These efforts were given a boost in 2015, when at its annual meeting, the G7 announced a goal of expanding access to climate-related risk insurance to 400 million additional people in the most vulnerable developing nations by 2020. This would quintuple the current level of coverage throughout the developing world from 100 million people to half a billion people. In order to meet this goal of making innovative insurance and climate risk-management tools available to so many millions of new people, a critical gap in high-resolution data and cutting-edge modeling needs to be bridged.

The opportunity for parametric insurance and catastrophe bonds

While insurance takes a variety of forms, one of the most promising for achieving the G7 goal is parametric risk insurance. Unlike traditional indemnity insurance—which prices premiums and payouts according to assessments of insured damages—parametric risk insurance offers preset payouts that can be disbursed in the immediate aftermath of a disaster when established environmental benchmarks, such as wind speed or rainfall levels, are exceeded. Other mechanisms—such as catastrophic bonds, or cat bonds—that can be bought and sold in financial markets rely on similar triggers. Since 2003, 43 countries have secured parametric coverage or begun to develop their own parametric risk insurance programs.

Fortunately, increased political attention is being paid to the positive role such insurance can play in helping the most vulnerable countries better cope with the effects of climate change. When President Barack Obama met with leaders of a number of highly vulnerable small island states at the international climate conference in Paris last December—formally know as the 21st Conference of the Parties to the U.N. Framework Convention on Climate Change—the administration announced that it would provide $30 million specifically to support parametric risk insurance programs operated by the Pacific Catastrophe Risk Assessment and Financing Initiative, the Caribbean Catastrophe Risk Insurance Facility, and the African Risk Capacity.

Still, achieving the G7 goal will be difficult without more leadership and resources from the G7. As discussed in the 2015 Center for American Progress report “Key Principles for Climate-Related Risk Insurance,” there are a number of design challenges that need to be worked out. But one thing that can and must be addressed immediately is the shortage of adequate risk modeling in developing countries—risk modeling that is a prerequisite for scaling up climate-related risk insurance system globally.

The need for expanded risk modeling

In 2006, the World Meteorological Organization completed a survey to evaluate the capacity, gaps, and needs of national meteorological and hydrological services in 139 different countries. Ninety percent of these countries indicated a number of shortcomings, including in their weather-observation networks; their maintenance capacities for hazard databases; and their methodologies for risk modeling to support development planning in different economic sectors.

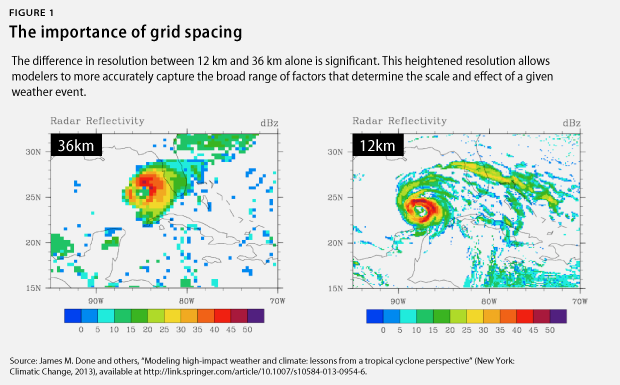

Modeling risk is no small task. Pricing for catastrophe insurance is both volatile and expensive, and insurance companies must collect exposure data from countries in order to model risk and establish policies. In many regions, aircraft and drone flybys mapping relevant territories have increased from weekly to daily affairs, capturing weather patterns, as well as the physical and economic landscape. Resolution has increased significantly, making models more accurate as inputs become more precise.

AIR Worldwide, one of the top catastrophe modeling companies, noted in late 2014 that it was “not aware of any market information system operating in a developing country that also incorporates agricultural risk modeling for risk management.” Nonmodeled disasters accounted for 30 percent of insurance claims as of 2015. In 2011—the costliest year for catastrophe losses yet, at $380 billion lost globally—60 percent of losses were from nonmodeled perils.

International financial institutions, development institutions, and national governments are currently making efforts to improve data needed for risk modeling and risk modeling itself in the developing world. For example, when the Caribbean Catastrophe Risk Insurance Facility—the world’s oldest multicountry parametric risk pool—launched in 2007, it did so with financial contributions from Canada, the European Union, the United Kingdom, France, Ireland, Bermuda, Japan, the World Bank, and the Caribbean Development Bank. These contributions totaled $50 million.

Furthermore, the World Bank has commissioned several catastrophic risk models, including awarding a grant to international risk management innovation company ImageCat to develop a physical exposure database for Ethiopia, Kenya, Niger, Senegal, and Uganda.

Nevertheless, data on natural disasters and disaster risk reduction are still severely lacking at the local level, which constrains improvements to reduce local vulnerabilities to extreme weather. Spatial coverage and database resolution are typically global and only retain state-level information, meaning that local levels lack specific data, which creates a wide degree of variation between loss estimates among subnational regions. Additionally, the threshold at which unique catastrophic events are catalogued often excludes smaller events with lower monetary losses. Other discrepancies between databases, such as nonmarket loss calculations—including health effects, natural asset/ecosystem damage, and the loss of historical and cultural assets—lack consensus on the physical effects of climate change and a nation’s adaptive capacity, as well as on the value of biodiversity and cultural heritage in risk assessments.

Expanding modeling to cover new geographic areas or new risks in a given area not only is a precondition to providing climate-related risk insurance to populations in those areas but also is critical to diversifying risk on the global scale, which would allow for expansion of coverage in areas where headway has already been made.

For instance, over the past decade, regional risk insurance pools have emerged to collectively pool and diversify the risk of countries in West Africa, the Caribbean, the South Pacific, and elsewhere. By occupying single regions, however, regional pools’ vulnerability to widespread disasters, such as hurricanes, typhoons, or droughts, increases. This can trigger payouts to multiple members of a risk pool, depleting a program’s capital reserves and resulting in higher premiums. Although these programs have attempted to ensure sufficient capital reserves against this risk, efforts to expand coverage beyond these programs will require greater geographic diversification.

As flooding in Southeast Asia is unlikely to be accompanied by drought in West Africa, for instance, including policies for both regions in a risk pool could reduce its overall risk exposure and could potentially lower premium costs for members. However, global risk diversification will require broad expansion of modeling to uninsured countries in order to adequately construct policies for new countries.

The G7 can and should play an important role in helping ensure that it meets its goal of expanding climate-related risk insurance in developing countries. Unfortunately, it was silent on the issue of risk insurance at its meeting this year. In 2017, the G7 should refocus its efforts on this task by advancing a public-private partnership between G7 nations, international insurers, and financial institutions to expand modeling capacity and eliminate the risk modeling gap. It can lift up and accelerate nascent innovative partnerships in this area, such as the Insurance Development Forum, which brings together the World Bank, the United Nations, and the insurance industry to focus on expanding insurance access to people in developing countries. The G7 also can provide additional financial and technical resources to provide expertise on weather patterns and projections, modeling design, and other important prerequisites for climate-related risk insurance expansion.

Conclusion

While the Paris Agreement marked a historic turning point in global efforts to combat climate change, the United States must nevertheless continue to ramp up efforts to help the world’s most vulnerable people and countries cope with the effects of climate change that it is already too late to avert. By providing additional tools and resources—and partnering with other countries, international financial institutions, and the private sector—the United States can drive progress toward this end by expanding access to climate-related risk insurance coverage in developing countries, in line with last year’s G7 goal.

Pete Ogden is a Senior Fellow at the Center for American Progress. Jerusalem Demsas is an intern with the Energy Policy team at the Center. Ben Bovarnick is a former Research Assistant with the Energy Policy team at the Center.