Author’s note: This report is not associated with Right to the City’s Homes for All campaign. The opinions and analyses contained in the report are those of the author and the Center for American Progress.

Introduction and summary

Housing affordability in the rental market is an essential determinant of whether a family is able to achieve economic stability. At the same time, the availability of affordable rental units is critical for the development, retention, and expansion of a local workforce and for economic competitiveness. Yet, rental housing is a pressing public issue for families at all income levels, particularly for those in the extremely low- to moderate-income brackets. Rental markets across the nation have become tighter, and as rent continues to outpace incomes, a substantial portion of renters are finding it increasingly difficult to meet nonshelter-related expenses and to build their savings. Forty-four percent of the nearly 30 million renters in the United States—excluding high-income households—have unaffordable rents; In other words, they spend more than 30 percent of their income on housing costs. Significant gaps in the supply of rental units that are affordable for households in different income brackets are largely due to the inadequate production of homes, particularly in the lower-income spectrum of the housing market. As the supply of low-rent units has decreased, additions to the rental housing stock have shifted to the high end—more specifically, to the very high end. High-end developments do not encourage enough supply to ensure that affordable housing trickles down to low- and moderate-income renters.

The private housing market and the government’s decadeslong experiment with a laissez-faire approach to supply have not worked well to fill the affordable housing gap. The federal government provides more than $120 billion annually in tax benefits for homeownership, particularly benefiting the wealthy.1 At the same time, despite the continuing effort of programs such as the Low-Income Housing Tax Credit (LIHTC), it does not adequately address the increasing gaps in affordable rental housing. The federal government cannot afford to downplay the importance of rental housing for its citizens and the economy. It is time for the federal government to contribute more aggressively to the U.S. supply of affordable rental housing, as it did in the past. However, re-evaluating historical practices in the direct government provision of affordable housing and learning from past mistakes are necessary first steps toward tailoring a viable, equitable, and sustainable response to the rental housing crisis.

This report recommends a Homes for All program, by which the federal government will engage in the large-scale construction of affordable and good-quality homes while avoiding the mistakes made in the past several decades in the construction and management of public housing. Homes for All emphasizes an active role in the production of affordable units for renters who are in need of affordable housing, under the assumption that supporting this type of housing will meet three goals: challenge private-market development practices that greatly influence home prices; encourage long-term affordability; and promote a process by which housing costs will better match household incomes, especially in proximity to employment centers and areas experiencing rapid job growth.

After a discussion of the current shortage of affordable rental housing and a brief account of past federal government practices in the direct provision of affordable rental units, this report outlines the Homes for All program, which features the following elements:

- Construction: The federal government will direct capital grants to the construction and management of new government-funded housing.

- Design: Unlike past government-produced housing, Homes for All will feature the following attributes:

- Homes will be available to a mix of incomes, while preserving the ability to target assistance to those with the greatest need, and the socioeconomic status of residents will be impossible to distinguish by the exterior appearance of buildings through uniform design standards.

- In large metropolitan areas experiencing rapid job growth and featuring a large transit and/or rail system, units will be part of transit-oriented developments (TODs).

- Mixed-use development and commercial uses on ground floors will be encouraged to serve residents and neighbors; to stimulate job and small-business creation; and to provide an added income stream.

- Building heights will be consistent with surrounding built areas, and units will be scattered throughout the region.

- A variety of units will be produced to accommodate several types of households, although single people are the most common type of renter household.

- Structures and units will feature universal design principles in order to promote access for and use by all people regardless of their age, family size, or ability.

- Units will be equipped with broadband internet access.

- Construction techniques will promote energy efficiency and recycling. Construction will also explore novel building techniques and quality construction materials, such as modular construction.

- Land acquisition: Under the Homes for All program, the federal government will produce housing units on publicly owned land, where possible, and otherwise on acquired sites that will be converted into community land trusts (CLTs).

- Management: Upon completion, the housing stock created under the Homes for All plan will be managed and operated by local nonprofit, mission-driven organizations and CLTs.

- Eligibility: The Homes for All program will not be means-tested and will be aimed at a broad spectrum of individuals and families who are in need of affordable housing. Homes for All will offer a variety of housing types to people based on what they need. A point system based on need will be established locally for the allocation and transfer of units to families and individuals. Priority in unit allocation will be determined based on a variety of factors which include, but are not limited to, the following: current housing cost burden; distance to jobs and educational opportunities; accessibility; overcrowding; and presence of young children and older adults.

- Long-term affordability and security of tenure: Publicly financed housing will be permanently held in some form of social ownership, such as CLTs.

This report proposes the production of 1 million homes over the next five years through the Homes for All program. The construction program will require a minimum of $20 billion in funding annually over the next five years. This would be a worthy capital investment in the lasting economic stability of American families.

The shortage of affordable rental units

The rental market presents a critical challenge for a vast proportion of Americans. More than 36 percent of Americans are renters,2 and housing affordability in the rental market is a major determinant of whether a family is able to achieve economic stability. It is essential for enabling families to save for their children’s education, purchasing a home, and retirement. Access to adequate affordable rental opportunities can also determine whether a family will be able to move to a new place in search of good job opportunities.

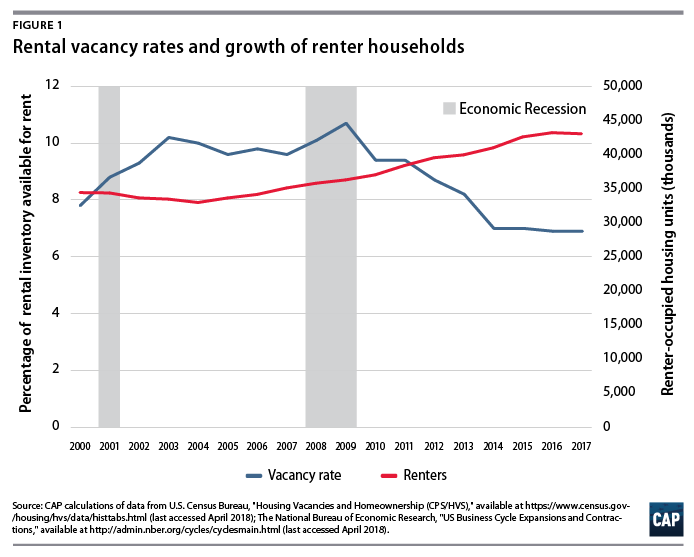

In the years following the Great Recession, rental markets across the nation have become tighter due to the drop in homeownership; the increase in rental demand; and inadequate production of homes, particularly in the lower-income spectrum of the housing market. Since 2010, the number of renter households has increased by nearly 1 million a year and a large part of the growth in rental demand has been driven by the increase in high-income renters.3 At the end of 2017, 43.1 million households rented their homes; this number is projected to increase by nearly 500,000 annually over the next decade. (see Figure 1)4 Reflecting the increased demand for rental units, the national rental vacancy rate has decreased from 10.7 percent in the fourth quarter of 2009 to 6.9 percent in the fourth quarter of 2017. Vacancy rates vary geographically. The New York City Housing and Vacancy Survey, for example, reports that in 2017, the citywide vacancy rate was 3.63 percent.5

Since 2000, rent of primary residences has increased, on average, by 15 percent in real terms, while the median income of renter households has decreased by 2 percent.6 As rent continues to outpace incomes,7 families across all income brackets are finding it increasingly difficult to meet nonshelter-related expenses and to build their savings. This problem is becoming more common among middle-income renters but it is particularly critical for those low-income households spending more than half of their income on housing. These households cannot meet other basic necessities—such as food, transportation, and medical costs—after paying for housing.8 Every year, millions of people are evicted—in many cases, because they cannot afford their rent.9 The National Low Income Housing Coalition indicates that across the nation, it is impossible for a person working full time at the federal minimum wage to afford a two-bedroom rental unit at the fair market rent.10 Furthermore, people of color are disproportionately represented among renter households, and 1 in 5 renters is foreign-born.11 Lack of sufficient affordable housing, combined with other barriers such as housing market discrimination, reduces the range of residential options for these groups.

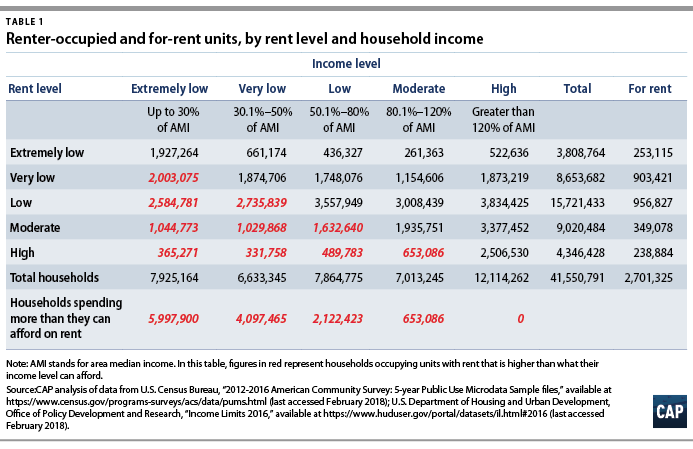

Table 1 shows the significant gaps in the supply of rental units that are affordable for households in different income brackets, even after subtracting units that are for rent.12 (see Methodology) Excluding high-income households, 44 percent of nearly 30 million renters have unaffordable rents—in other words, they spend more than 30 percent of their income on housing costs. Nearly 8 million renter households—19 percent of all U.S. renters—live on extremely low incomes, or an income level defined by the U.S. Department of Housing and Urban Development (HUD) as at or below 30 percent of the family area median income (AMI).

Furthermore, only about 4 million units in the United States—including those that are available for rent—rent at a price that is affordable to the extremely low-income bracket. (see Table 1) And only about 2 million extremely low-income renter households occupy units that are affordable to them. The remaining 1.9 million units renting at extremely low rates are occupied by higher-income households. About 6 million extremely low-income renter households—76 percent of all extremely low-income renters in the United States—occupy units that cost more than 30 percent of their income. Similarly, two-thirds of very low-income renter households, another HUD-defined income bracket, occupy units that are unaffordable to them, partly because a large number of the available units that would be affordable are occupied by households with higher incomes. (see Methodology for definitions of income brackets)

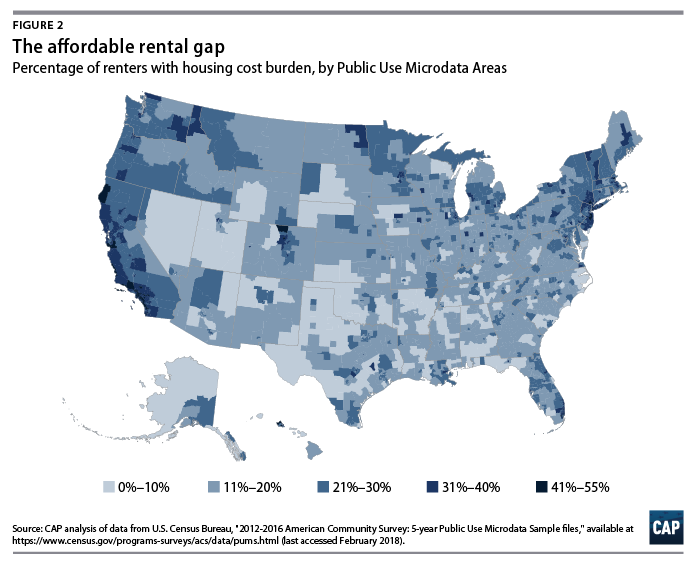

The affordability problem for renters is particularly severe in large metropolitan areas across the nation. As Figure 1 indicates, large clusters of cost-burdened families are located in the Northeast, in the Midwest, along the Pacific Coast, and in the South Atlantic regions. In states such as California, New York, and Florida, nearly one-third of all renters are severely burdened, spending more than half of their income on housing costs. The availability of affordable housing is critical for the development, retention, and expansion of a local workforce and for economic competitiveness,13 and the cost of housing represents an important barrier to geographic labor mobility.14 Across America, the shortage of affordable housing blocks families looking to move in search of good jobs. This affects not only those families but also struggling communities and the workers who wish to remain in them, as those localities may be able to adjust more easily if their labor supplies were not out of line with market needs.

The affordability problem for renters is particularly severe in large metropolitan areas across the nation. As Figure 1 indicates, large clusters of cost-burdened families are located in the Northeast, in the Midwest, along the Pacific Coast, and in the South Atlantic regions. In states such as California, New York, and Florida, nearly one-third of all renters are severely burdened, spending more than half of their income on housing costs. The availability of affordable housing is critical for the development, retention, and expansion of a local workforce and for economic competitiveness,13 and the cost of housing represents an important barrier to geographic labor mobility.14 Across America, the shortage of affordable housing blocks families looking to move in search of good jobs. This affects not only those families but also struggling communities and the workers who wish to remain in them, as those localities may be able to adjust more easily if their labor supplies were not out of line with market needs.

Unfortunately, federal rental assistance programs continue to fall short of meeting the increasing need for affordable rental units among low-income households. Despite a growing demand for housing assistance, the deep cuts in funding that Congress has made to HUD programs in recent years have intensified the shortage of subsidized housing resources.15

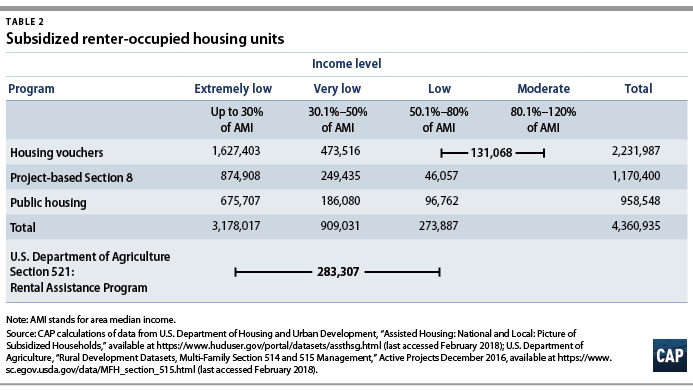

HUD’s most recent report on the United States’ worst housing needs16 indicates that the gap in rental assistance relative to need is widening. Federal rental assistance programs currently serve about 4.5 million low- to moderate-income households, and they have not kept pace with the growing need.17 Only a small fraction of the 44 million households who rent their homes receive some form of rental assistance. (see Table 2) From 2001 to 2015, the share of renter households eligible for federal housing assistance and receiving rental subsidies decreased from 28 percent to 25 percent.18 Center for American Progress analysis indicates that a large proportion of extremely low- and very low-income renter households—60 percent and 86 percent, respectively—do not receive any rental assistance in the form of housing vouchers, public housing, or project-based Section 8 subsidies. Housing authorities across the nation have extremely long waiting lists of families seeking housing assistance.19

Currently, the LIHTC program, which was established by the Tax Reform Act of 1986, represents the largest federal subsidy addressing the limited supply of affordable rental units for low-income families. Since its inception, the program has financed the development and preservation of 3.05 million housing units.20 The LIHTC program alone, however, is not filling the affordable housing gap. And market forces have proven insufficient to meet the need for affordable housing—not only among those in the lowest brackets of the income distribution but for the middle brackets as well. Much of the expansion of the rental stock over the past 10 years can be attributed to the conversion of formerly owner-occupied single-family homes—largely a response to the foreclosure crisis—and the recent boom in multifamily construction.

The Joint Center for Housing Studies of Harvard University indicates that as losses in the supply of low-rent units have continued, additions to the rental housing stock have shifted to the high end—more specifically, to the very high end.21 In 2016, 40 percent of newly constructed rental units targeted higher-income households, compared with 15 percent of newly built units in 2001.22 The New York City Housing and Vacancy Survey, for example, indicates that the number of units renting for more than $2,000 per month increased by nearly 100,000 units from 2014 through 2017, whereas the number of units renting for less than $1,500 per month dropped by more than 165,000 during that same time frame.23 As research on filtering indicates,24 the construction of luxury rental units does not spur a filtering down process that is sufficient and fast enough to move the housing stock from higher- to lower-income households. This is particularly true in tight, high-cost markets such as San Francisco.25

In summary, rental markets across the nation have become tighter and continue to display significant gaps in the supply of rental units that are affordable for households in different income brackets, particularly among those at the bottom of the income distribution.

Lessons learned from previous direct government involvement in housing construction

During the Great Depression, Modern Housing, a book by public housing advocate Catherine Bauer, became the manifesto of a movement that called for the federal government’s direct involvement in the large-scale development of good-quality, affordable, and decentralized housing available to all American workers.26 Inspired in part by government-supported residential programs that were being developed at that time in Western Europe, the book called for innovative architectural design and low-interest capital that would cut costs and promote a more efficient production of housing, along with amenities and vibrant neighborhoods that everyone could enjoy.

Bauer and her fellow housing and labor activists had an important influence on early direct federal housing activity in the New Deal era, when the Great Depression created momentum for programs that focused on the production of housing for middle- and lower-income Americans. Indeed, the New Deal established a few homebuilding programs, none of which were officially referred to as public housing. As part of these programs, the federal government bought land and built dwellings, predominantly outside cities.27 Forty of the 99 communities built during the New Deal were rural or suburban.28

New Deal housing initiatives often assisted labor unions in the development of low-rent housing for American workers.29 The establishment of the Public Works Administration (PWA) Housing Division programs—created by Title II of the National Industry Recovery Act of 1933—sponsored slum clearance and housing construction as a job-creating measure. From 1934 through 1937, the PWA Housing Division produced 51 public housing projects that contained 21,800 units in total.30 Design standards were very high, and PWA housing was typically greeted by public approval. The Carl Mackley Houses in Philadelphia, which were completed for the American Federation of Hosiery Workers, are a well-known example of such endeavors. Like other developments completed under the PWA, this complex featured generous amenities such as apartments with porches, a pool, playgrounds, an auditorium, underground garages, a nursery school, rooftop laundries, and rooms for tenant activities.31 Other well-known examples are the Harlem River Houses in New York City and Lakeview Terrace in Cleveland.

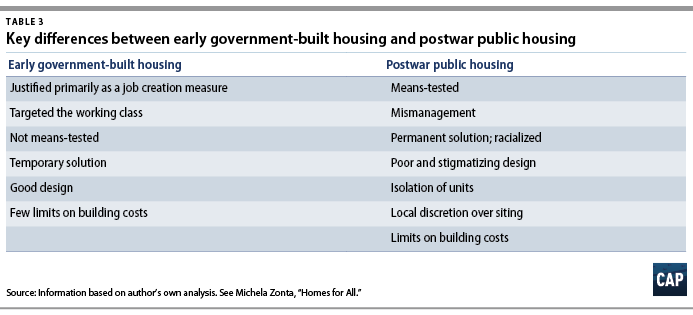

Public housing differed from private-market stock in its financing, development, and occupancy. Public housing entailed government ownership and was not means-tested.32 At first, PWA housing was available to anyone who desired to apply. (see Table 3) As historian Gail Radford argues, “programs limited to only the poorest have debilitating long-range problems. Their narrow constituency makes them more susceptible to budget cuts, and participants are often stigmatized.”33 With the George-Healey Act of 1936, however, income ceilings for PWA housing were established, and housing directly built and owned by the government became a residential option only for families of modest means.34

From the beginning, the PWA was regarded as a temporary agency. PWA housing, therefore, was not immediately perceived as a substantial threat to the private housing market.35 Resistance to public housing intensified when proposals emerged for a permanent public housing program.36 That permanent program was established when the Housing Act of 1937—also known as the Wagner-Steagall Act—authorized local public housing authorities (PHAs) to issue bonds to cover the costs of constructing public housing units.37 The program operated on a much larger basis than the PWA Housing Division, and decisions as to whether and where to build and locate public housing were left to individual localities, many of which never participated in the program.

Often, city councils would take control of the siting process, and public housing units would be spatially isolated from the mainstream market, particularly in neighborhoods with large concentrations of low-income people of color.38 Unlike PWA housing, the public housing program established under the Housing Act of 1937 was carried out by keeping construction costs minimal and by making units available only to the lowest-income groups. Cuts in public housing construction costs were detrimental to the quality and safety of units and buildings: Often, closets did not have doors, kitchens were not separate from other living quarters, and high-rise developments featured skip-stop elevators.39 In addition, the law’s equivalent elimination provision ensured that the public housing program would not constitute a significant threat to the private housing market. Public housing construction was linked to slum clearance and the replacement of substandard units, because slum buildings were razed and replaced with public housing buildings in the same areas. This clause had profound implications in terms of residential segregation: Public housing tended to be built where slums had been previously located and where people of color were concentrated due to the absence of any other residential options because of racial discrimination.40

After being temporarily derailed by World War II, the public housing program was reauthorized by the Housing Act of 1949. Subsequently, the public housing program was largely used to support the urban renewal program.41 Public housing, as it was redesigned and repurposed in the postwar era, has been hotly debated, despite some lasting successes, which include those of many small housing authorities.42 Many factors have led to the stigmatization and perceived deficiencies of government-built housing, including mismanagement; the means-tested and racialized nature of the program; poor design; limits on capital and operating costs; the placement of units and tenant allocation practices; and local discretion over siting.43

The Housing Act of 1949 limited public housing to very low-income families44 and set ceilings on rents and construction costs. When income exceeded the maximum allowed, many working-class families who had previously been eligible for public housing could no longer receive this subsidy and were often evicted. Many took advantage of low-cost mortgages insured by the Federal Housing Administration to purchase homes in suburban areas. As a result, the median income of public housing tenants has fallen considerably since 1949, and the public housing population has become increasingly destitute. This has had important implications for local PHAs’ ability to cover maintenance and operating expenses with rental revenues.45

New units continued to be built in less desirable areas, often in the same areas where prewar public housing projects emerged, and tenants typically reflected the racial composition of the surrounding neighborhood.46 In addition, public housing was no longer regarded as a Depression-stimulated response for the temporarily and deserving poor. By now, public housing was viewed as a permanent housing solution for poor people who were separated from mainstream society, particularly people of color. A shift in architectural design, particularly in large cities, reflected this view. New public housing projects in cities such as Chicago and Cleveland featured a massive scale, severity, a minimum number of amenities, and a distinctive appearance.47 Housing officials claimed that the construction of high-rise structures was cost-effective and that by building up, they would be able to provide more space for playgrounds. Yet this approach turned out to be costlier than expected, largely because of the cost of land in central cities, construction labor and materials, and maintenance. In addition, the institutional appearance of high-rise public housing contributed to the stigmatization of tenants.48

The public housing stock reached its peak in 1994, with 1.4 million units. As of 2012, only a small portion of all public housing units—9 percent—had been constructed after 1989, and those that had were largely constructed to replace older ones. Since 1994, the number of public housing units has declined, and most of the funding appropriated for public housing has been devoted to the preservation and redevelopment of existing units.49 As of 2017, the public housing stock consisted of 1,041,888 units.50 The reduction of the public housing stock in the past three decades has been largely due to the demolition of troubled projects, as well as the sale of public housing units, often as part of HUD’s HOPE VI program.51 The program’s efforts to dismantle distressed projects and convert them into mixed-income communities have often resulted in the displacement of families. These efforts have also contributed to the net loss of public housing units throughout the nation, thus reducing the supply of affordable housing for extremely low-income individuals and families.

In 2018, access to public housing units continues to be means-tested. Eligible tenants must have an income lower than 80 percent of the family AMI, and at least 40 percent of new tenants in any year must be extremely low-income—meaning that they must have either an income below 30 percent of the AMI or the state poverty level adjusted for family size, whichever is greater.52

As the brief account of public housing presented above indicates, the direct federal government provision of affordable housing has been characterized by both successes and pitfalls over the past several decades. The history of public housing provides some invaluable lessons for policies designed to increase the supply of affordable rental units, and the proposed Homes for All program—described next—takes these lessons into serious consideration.

Recommendation: Create a Homes for All program

The supply of affordable rental units is not sufficient to address the housing needs of a substantial portion of Americans, from the extremely low-income to those in the moderate-income brackets. The private housing market is not filling the gaps in the supply of affordable units for rent, and it is time for the federal government to contribute more aggressively to the U.S. supply of affordable housing, as it did in the past. However, re-evaluating historical practices in the direct government provision of affordable housing and learning from past mistakes are necessary first steps toward tailoring a viable, equitable, and sustainable response to the rental housing crisis.

CAP proposes the establishment of a Homes for All program that would avoid past mistakes in its efforts to reinvigorate the government’s role in addressing the shortage in the affordable rental housing supply across the nation. The approach emphasizes an active role in the production of affordable units for families of all income levels, while preserving the ability to target assistance to those with the greatest need, under the assumption that supporting this type of housing will accomplish three goals: challenge private-market development practices that greatly influence home prices by prioritizing luxury apartment construction; encourage long-term affordability; and promote a process by which housing costs will better match household incomes, especially in proximity to employment centers—areas of the country where many people are employed—and areas that are experiencing rapid job growth. The Homes for All program is designed to complement both existing rental assistance programs and current and future rehabilitation programs that address the preservation of existing affordable housing stock. These programs need additional investment to meet the needs of the population, and Homes for All would be an important complement.

Homes for All is characterized by the features discussed in the following subsections.

Construction

The federal government will direct capital grants to the construction and management of new government-funded housing.53 Modeled on the design of early New Deal housing initiatives, this action will spur local construction of supply according to local circumstances, while minimizing dependence on credit and debt, which can contribute to higher rents. The federal government currently runs programs that address operating and capital funds for existing public housing, as well as programs—including the Low-Income Housing Tax Credits (LIHTC), the Community Development Block Grants, and the HOME Investment Partnerships programs—that assist local communities in the development and preservation of affordable housing units. But no funding has been directly provided for the construction of public housing since the mid-1990s.54 Under the Homes for All program, funds will be allocated geographically according to housing needs, expected amount of private development, and long-term growth. In addition, areas featuring rapid job growth will have funding priority. Community input will be encouraged, and special protections will ensure that housing serves the needs of all, including workers, communities of color, LGBTQ households, seniors, and people with disabilities.

Design

Design quality is a crucial component of good affordable housing.55 As in the past, the federal government will use local architectural firms and building contractors in the design of new housing units.56 Unlike past government-produced housing, however, housing created under the Homes for All program will feature the following attributes:

- Homes will be available to a mix of incomes, and uniform design standards will make it impossible to distinguish the socioeconomic status of residents by the exterior appearance of buildings. Like HOPE VI, the program encourages the development of mixed-income communities. Unlike HOPE VI, however, the program will not induce displacement, since it will boost the overall supply of affordable housing.

- In large metropolitan areas experiencing rapid job growth and featuring a large transit and/or rail system, units will be part of TODs.57

- Where appropriate, mixed-use development and commercial uses on ground floors will be encouraged to serve residents and neighbors, to stimulate job and small-business creation, and to provide an added income stream.

- Building heights will be consistent with surrounding built areas, and units will be scattered throughout the region to avoid segregation patterns.

- A variety of units will be produced—including microunits, larger units, and cohousing options—to accommodate several types of households. Although single people are the most common type of renter household,58 the number of other types of renter households is on the rise, including extended and multigenerational families.59 The types of structures will also vary based on geographic location. For instance, apartment buildings will be favored in large and dense metropolitan areas.

- Structures and units will feature universal design principles60 in order to promote access for and use by all people regardless of their age, family size, or ability. Universal design anticipates future needs and makes homes safer for tenants to use throughout their lifespans, making it easier for older adults to age in place. Some of the features of universal design include—but are not limited to—no steps at entrances; a minimum space at entry doors; at least one accessible bedroom and one accessible bathroom on a ground floor; minimum clear door opening widths and clear floor space; and mechanically adjustable counter segments, such as adjustable cooktops to allow someone to cook from a seated position.61

- Units will be equipped with broadband internet access. Broadband access contributes to the quality of life of individuals and families in many ways, from improving connectivity to supporting education and access to health care services. Yet, a digital divide between the rich and the poor persists in U.S. society and affects particularly people of color.62 Equipping homes with broadband access can help reduce this divide and promote tenants’ quality of life.

- Construction techniques will promote energy efficiency and recycling. Energy efficiency reduces long-term operating costs while containing tenants’ utility expenses.63 Construction will also explore novel building techniques and quality construction materials, such as modular construction. Industrial approaches, uniform building codes, permit streamlining, and improved purchasing could support large-scale developments and reduce building costs.64

Modular construction

The construction costs of apartment rental units continue to increase.65 The price of materials and the cost of labor, in particular, have driven construction costs.66 Modular construction is an alternative way of building in which individual components or modules are manufactured in an off-site, climate-controlled facility before being transported on-site, where they are assembled on a foundation.67 These units are permanent and, after assembly, look very similar to conventional units.

There are several benefits associated with modular building that can translate into significantly lower rents. These include cost savings, as off-site construction can save up to 20 percent of the cost of building a three- to four-story multifamily apartment building. Labor and production efficiency can also be enhanced.68 Economies of scale can be achieved through standardization, and procurement costs can be reduced. In addition, off-site construction reduces time costs, as many of the construction steps can be performed simultaneously and often while site infrastructure and foundations are prepared.69

Several countries have adopted this method for housing production.70 But there are relatively few factories in operation in the United States and at-scale production of housing has yet to be achieved, partly because of a series of challenges related to materials, design, regulation, and construction site conditions. All these challenges could be addressed through shifts in production and design and changes in zoning laws.71

Land acquisition

Land costs represent an important element of the cost of housing construction.72 Under the Homes for All program, the federal government will produce housing units on publicly owned land, where possible, and otherwise on acquired sites that will be converted into CLTs.73 Jurisdictions across the nation have identified a variety of opportunities for the development of affordable housing on public land.74 These opportunities include different types of sites, from vacant, publicly held land and underutilized sites such as parking lots, to lots where existing public facilities are no longer needed. To maximize the assembly and acquisition of land, especially in dense urban areas, the federal government will consider infill development,75 underused land in proximity to public transportation, the repurposing of older infrastructure, innovative vacant land regulation, and zoning changes.

In addition, the joint development of housing and public facilities on public land through a mixed-use development model can lead to cost savings and better access to public services.76 One of the main challenges associated with the utilization of public land is related to the fact that, in most communities, public land is controlled by several separate agencies, such as school boards or hospital boards, or fire, police, or transportation departments. The Homes for All plan will encourage the establishment and authorization of a formal federal agency to develop and consolidate the inventory of public land holdings.77

Management

Upon completion, the housing stock created under the Housing for All plan will be managed and operated by local nonprofit, mission-driven organizations, and CLTs. These will be responsible for setting rents to cover operations and maintenance, though the federal government will continue to provide an appropriate stream of operating subsidies and funding for capital needs. Since construction costs will be reduced by building units on publicly owned land, homes will be more affordable, allowing families to save and inject money into local economies.

Eligibility

The Housing for All program will not be means-tested and will target individuals and families based on their housing needs. The program will be designed following the example of early New Deal programs and some social housing programs in Western Europe, which have historically targeted a wider spectrum of citizens than U.S. rental assistance programs.78 A point system based on need will be established locally for the allocation and transfer of units to families and individuals. Priority in unit allocation will be determined based on a variety of factors which include, but are not limited to, the following: current housing cost burden; distance to jobs and educational opportunities; accessibility; overcrowding; and presence of young children and older adults. The mix of incomes in these developments will have the potential of cross-subsidizing units for lower-income families. To allow for deeper income targeting while encouraging mixed income housing, the program will adopt a split-subsidy approach by which developments will be required to set aside several units for housing voucher holders, as is currently done in LIHTC projects.

Long-term affordability and security of tenure

Publicly financed housing will be permanently held in some form of social ownership, such as CLTs. Security of tenure will be ensured through enhanced tenant protections, such as protections against discriminatory practices, retaliation for complaints, and unjustified evictions.

How many homes?

CAP proposes the production of 1 million homes over the next five years through the Homes for All program.79 This is a conservative figure, given the gaps illustrated in Table 1. At the same time, it is important to consider four possible side effects: With the provision of new units, some shifting—filtering up and down—of the existing stock can be expected; a large-scale development such as the proposed program may influence market rents downward; the program is designed to complement current programs devoted to the production and rehabilitation of affordable housing and the preservation of public housing; and with an increase in rental units that are affordable for lower-income households currently receiving Housing Choice Vouchers (HCV), the program will encourage a shift of these allowances to renters who are not currently served by the HCV program despite their eligibility.

How much would it cost?

The Homes for All program will entail the construction of housing units of different types and sizes to serve a variety of households in different markets. Preliminary estimates are based on three figures and calculations: CAP analysis of the characteristics of households with a cost burden across different income levels; the national average size of a two-bedroom apartment; and current building costs for apartments of different quality classes and building sizes.80

Most cost-burdened households currently reside in apartments and include one to four people. These households are of different types, though female-headed households and singles tend to be prevalent across all income brackets. Households with at least one senior represent 20 percent of cost-burdened households across all income levels.

Meanwhile, the national average size of a two-bedroom apartment is approximately 900 square feet. The average building cost for a 900-square-foot unit in a building containing at least 10 units of good quality is $111 per square foot.81 This cost does not include land acquisition.

Based on these data and excluding the cost of land acquisition, the construction program will require a minimum of $20 billion in funding annually over the next five years.82 This would be a worthy capital investment in the lasting economic stability of American families.

Conclusion

Unlike programs supporting the private housing market and homeownership, the federal government’s direct involvement in the production of rental housing has never earned widespread popularity. Nonetheless, public housing has long provided affordable housing for very low-income families whose needs the private market could not meet. Much of the controversy around and the unpopularity of public housing can be attributed to the compromises inherent in the laws and policies discussed above that have constrained the program’s implementation and quality over time.

Much can be learned from past mistakes in housing policy. This is especially the case with regard to the design and implementation of a government-sponsored program that addresses the supply of much-needed affordable rental housing. While complementing existing affordable housing initiatives, the adoption of the Homes for All program would represent a first step toward reinvigorating the government’s role in directly and equitably addressing the supply of affordable housing across the United States.

About the author

Michela Zonta is a senior policy analyst for Housing and Consumer Finance Policy at the Center for American Progress. She has extensive research, teaching, and consulting experience in housing and community development. She has published work on the government-sponsored enterprises, mortgage-lending practices of ethnic-owned banks in immigrant communities, jobs-housing imbalance in minority communities, residential segregation, and poverty and housing affordability. Zonta holds a bachelor’s degree in political science from the University of Milan, as well as a master’s degree and a doctorate in urban planning, both from the University of California, Los Angeles.

Acknowledgments

The author thanks Andy Green, Marc Jarsulic, Rejane Frederick, and Heidi Schultheis for their very thorough and helpful feedback on early versions of this report. The author also thanks Melissa Boteach, Jim Carr, Seth Hanlon, Jacob Leibenluft, Silva Mathema, Ben Olinsky, Paul Ong, Joe Valenti, and Mark Willis for their invaluable input.

Data and methodology

The statistical analysis presented in this study was performed with data from the American Community Survey’s (ACS) Public Use Microdata Sample (PUMS). ACS PUMS files provide estimates of socioeconomic and housing characteristics at the household and person levels. The data are produced annually by the U.S. Census Bureau and are available in one-year, three-year, and five-year files. The multiyear files combine data from each year’s one-year file and thus feature a larger sample size, which increases the statistical reliability of the data and yields more precise estimates for subpopulations and small geographic areas. This analysis is based on household-level information on housing tenure, income, and housing costs from the 2012–2016 ACS five-year PUMS data set. The study focuses on single-family and multifamily housing units that are either renter-occupied, vacant, and available for rent, or rented but not occupied, excluding structures that are mobile homes, boats, recreational vehicles, or vans.83 Household income and monthly rent data are adjusted for inflation to reflect 2016 dollars.

Renter households were classified into five income brackets based on county-level income limit data from HUD.84 Since PUMS data do not report information by county—instead reporting it by Public Use Microdata Areas (PUMAs)85—it was necessary to transform the data to assign the correct county-level HUD family AMI information to each household record. PUMAs were matched to counties through the Missouri Census Data Center’s MABLE/Geocorr 14 online crosswalk.86 PUMA-level 2016 family AMI cutoffs for a four-person family were derived using two methods: determining the portion of counties corresponding to PUMAs based on a housing unit weight; and weighting HUD family AMI data based on the number of families residing in each PUMA. After adjusting family AMI cutoffs by the number of people in each household,87 the analysis categorized households by their income relative to the adjusted family AMI cutoff. Households reporting an income of $0 or a negative income were omitted from the analysis. The cutoffs were as follows:

- Extremely low income: up to 30 percent of HUD family AMI

- Very low income: 30.1 percent to 50 percent of family AMI

- Low income: 50.1 percent to 80 percent of family AMI

- Moderate income: 80.1 percent to 120 percent of family AMI

- High income: greater than 120 percent of family AMI

The affordability cutoff of a given rental unit was defined as the minimum percentage of family AMI that a family would have to earn in order to spend no more than 30 percent of its income to rent a housing unit, adjusted by the number of bedrooms in that unit.88 Housing units were categorized as extremely low rent, very low rent, low rent, moderate rent, and high rent based on their cost relative to affordability cutoffs.

A geographic information systems (GIS) analysis was performed to illustrate the distribution of renters spending more than 30 percent of income for housing by PUMA.89