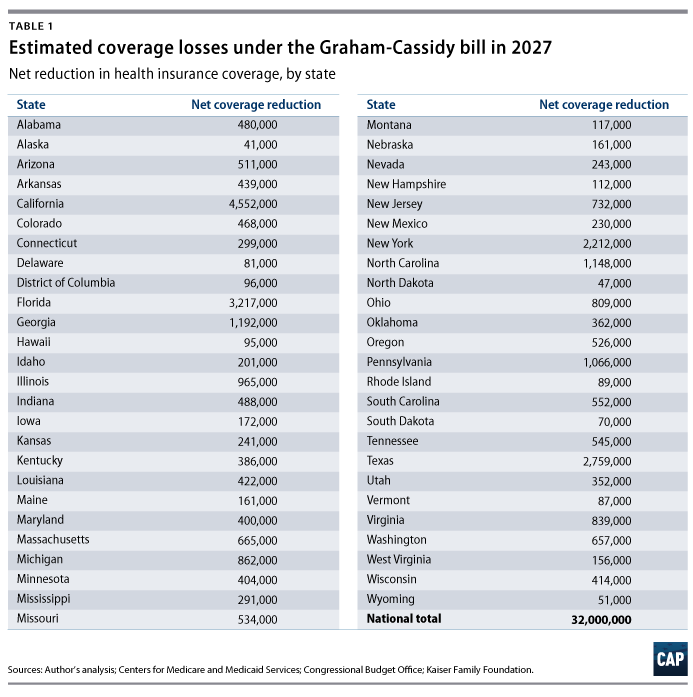

With only two weeks left to move forward with a partisan health care repeal bill, some Senate Republicans are trying one last time to rip coverage from millions of Americans. Their latest effort, introduced by Sens. Lindsey Graham (R-SC) and Bill Cassidy (R-LA), would make devastating cuts to Medicaid and cut and eventually eliminate funding that helps people in the individual insurance market afford coverage, leading to at least 32 million fewer people having coverage after 2026.

Those who did not lose coverage would see their premiums increase significantly. In the first year, premiums would increase by 20 percent. But the increases would be even greater for people with pre-existing conditions because the bill would let insurers in the individual market charge a premium markup based on health status and history, which could increase their premiums by tens of thousands of dollars.

Huge premium markups for pre-existing conditions

As with a previous Affordable Care Act (ACA) repeal bill in the House, the American Health Care Act (AHCA), Graham-Cassidy would allow states to eliminate protections for people with pre-existing conditions. And just as with that previous proposal, this would increase premiums for people with certain health conditions by tens of thousands of dollars.

Before the ACA, insurers evaluated potential enrollees’ health and medical information, a process known as medical underwriting, and raised premiums, excluded conditions, or declined coverage for people with pre-existing conditions. One study found that insurers quoted premiums as much as 50 percent higher for depression and 100 percent higher for breast cancer. And one underwriting manual showed that simply being overweight resulted in a 25 percent premium increase for some plans. But such examples are not fully representative of the increased premium costs for people with pre-existing conditions, as many of the costliest people were likely to be rejected.

The ACA prohibits insurers from charging higher premiums based on factors such as health status or pre-existing conditions. Graham-Cassidy would let states eliminate that requirement so carriers could impose surcharges on premiums based on health status and medical history.

The Center for American Progress estimated what surcharges would be for various medical conditions in states that eliminate pre-existing condition protections. We drew upon data that the Centers for Medicare & Medicaid Services (CMS) uses to calculate transfers between insurers based on enrollees’ expected costs—this is called the risk adjustment program. We compared the plan liability for total costs for a healthy 40-year-old to the plan liability if that individual had certain medical conditions, as shown in Table 1 below.

Based on our analysis, we estimate that individuals with even relatively mild pre-existing conditions would pay thousands of dollars above standard rates to obtain coverage. For example, an individual with asthma would face a premium surcharge of $4,340. The surcharge for diabetes would be $5,600 per year. Coverage could become prohibitively expensive for those in dire need of care: Insurers would charge about $17,320 more in premiums for pregnancy, $26,580 more for rheumatoid arthritis and other autoimmune disorders, and $142,650 more for patients with metastatic cancer.

And this analysis does not account for surcharges that would result from individuals’ previous health conditions. Scarce data exist on pre-ACA rate-ups, but insurers raised premiums for individuals based on health history, not just current health status. Without pre-existing condition protections, cancer survivors now free of the disease or patients who underwent successful surgery years ago could find themselves facing significant surcharges as well.

And this analysis does not account for surcharges that would result from individuals’ previous health conditions. Scarce data exist on pre-ACA rate-ups, but insurers raised premiums for individuals based on health history, not just current health status. Without pre-existing condition protections, cancer survivors now free of the disease or patients who underwent successful surgery years ago could find themselves facing significant surcharges as well.

Conclusion

Graham-Cassidy would be devastating for individuals with pre-existing conditions. In looking at a similar provision in the AHCA, the nonpartisan Congressional Budget Office (CBO) projected that half the population would live in states that waived protections for pre-existing conditions by allowing insurers to charge more based on health status or exclude coverage for certain types of services, a backdoor method gutting protections for people who need care for conditions such as pregnancy or mental health issues. It’s time for the Senate to put an end to its efforts to strip millions of Americans of their coverage, and start focusing on bipartisan improvements to the individual insurance market, such as those being discussed by Sens. Lamar Alexander (R-TN) and Patty Murray (D-WA), among others.

Sam Berger is the senior policy adviser at the Center for American Progress. Emily Gee is the health economist of Health Policy at the Center.

Methodology

Under the ACA, insurers can vary premiums according to standard age rating curves but cannot vary them by health status. To estimate how rating up would affect premiums without pre-existing condition protections, we used relative cost factors from the CMS risk adjustment program, which is calibrated to the costs of the individual market population.

Our starting point for our estimate is a CBO score of the AHCA, which projected that the premium for an individual of age 40 would be $6,050 per year in 2026. Because the CBO estimate assumed community rating, such that all individuals at a given age would pay the same premium regardless of health status, and because 40 is the average age in the exchanges, we believe that $6,050 is a good approximation of what the average premium would cost in that year for the exchange population. We therefore assume that $6,050 would be the premium for someone with average plan liability risk, or a score of 1.0. This person would be of average health status and therefore not perfectly healthy.

We applied just the CMS risk adjustment factors for age and sex in order to represent the plan liability for a healthy individual. We took the risk factors for a male ages 40 to 44 (score of 0.221) and a female ages 40 to 44 (0.455), to generate a weighted average risk score for a 40-year-old (0.347) using the current male-to-female ratio in exchange enrollment. Multiplying the risk score by the average premium implies that $2,100 would be the actuarially fair premium for a 40-year-old with no health conditions.

Health plans would set premiums at the time of application and would need to price in unforeseen conditions among apparently healthy people. For example, enrollees may not become pregnant or receive a cancer diagnosis until after enrollment. Because current diagnoses and medical history are not perfect predictors of future health status, we assume that the risk score for an enrollee with no conditions at the time of application would be 0.674, halfway between the average among all enrollees (1.0) and that of a person who remains healthy all year (0.374). This equates to a standard rate premium of roughly $4,020 annually for individuals healthy at the time of application.

We then used the CMS risk adjustment factors to estimate the relative cost of selected health conditions relative to the cost of a healthy individual, then converted these into dollar amounts representing premium surcharges. For example, an asthma diagnosis adds 0.717 to an individual’s risk score, increasing it by 106 percent. The asthma patient would therefore pay a surcharge of $4,340 on top of standard rates for coverage because of that condition. Metastatic cancer adds a factor of 23.6 to an enrollee’s risk score, such that a patient with advanced cancer would pay an additional $142,650 for coverage.

Note that because the risk adjustment program calculates scores using each year’s current diagnoses rather than medical history, we were unable to apply our method to estimate the rate-ups that individuals would face for prior health conditions. Our method also does not account for the adverse selection that would occur if community rating were repealed. The surcharges for pre-existing conditions would likely deter some relatively healthier sufferers of each condition to forgo insurance. Actual surcharges would, therefore, reflect the cost of treating the more severe cases of each condition and be higher than the amounts we estimate.