To download a spreadsheet showing estimates of the effects of full ACA repeal by state and congressional district, click here.

Yesterday, despite the faulty legal reasoning of the Republican attorneys general and governors who initiated the Texas v. United States health care repeal lawsuit, as well as the clear partisan nature of the case, the U.S. Court of Appeals for the 5th Circuit ruled that the Affordable Care Act’s (ACA) individual mandate was unconstitutional following enactment of the so-called Tax Cuts and Jobs Act of 2017, which zeroed out the individual mandate penalty. The 5th Circuit also remanded the case back to the U.S. District Court for the Northern District of Texas to determine what other parts of the ACA can stay in place given its decision that the individual mandate is now unconstitutional. Not only does this ruling increase uncertainty and threaten health care coverage for millions, but it also places power over the U.S. health care system back into the hands of Judge Reed O’Connor—a man who legal scholars say was handpicked “for his partisan loyalties” and who previously ruled that the entire law must be struck down.

After several failed attempts by congressional Republicans to repeal the ACA, President Donald Trump’s allies—with the support of his Department of Justice—are taking a circuitous route through the judiciary to advance their assault against the ACA.

A ruling that invalidates the ACA or core features of the law would have a devastating impact on the American people. The Trump administration seems well aware of this, as it has previously said that it would request a stay to delay repeal if the courts strike down the entire ACA and may try to slow down any appeal to the U.S. Supreme Court. Yet by backing the lawsuit without any replacement plan, Trump is essentially gambling for “repeal and delay,” a proposal that was too unpopular and damaging to pass Congress.

While the case continues to move through the judiciary, the uncertainty of a future Supreme Court decision will create chaos and harm throughout the health care system in the near term—especially in the individual market. Insurers price plans based on expected costs, and the added uncertainty about the fate of the ACA’s marketplaces and consumer protections could drive them to hike premiums dramatically or withdraw from the individual market altogether.

Ultimately, the consequences for the U.S. health care system depend on the rulings of the district court and Supreme Court. Under the most devastating scenario, a ruling that invalidates the entire ACA would upend the health care system as Americans know it, including by eliminating coverage for millions of people, rolling back consumer protections, and increasing costs for millions more.

Repealing the ACA would lead to the loss of not only well-known coverage-related provisions such as Medicaid expansion and the health insurance marketplaces but also important ACA programs and protections for Americans with other types of coverage. For example, the district court could end federal rules preventing insurance companies from discriminating against people with preexisting conditions, as well as a rule allowing young adults to remain on their parents’ employer-based insurance plans until age 26. Even seniors covered by Medicare could be harmed; some beneficiaries may see their premiums and out-of-pocket costs rise and therefore risk falling back into the prescription drug coverage gap.

Below are just five of the key consequences of the 5th Circuit’s decision to remand:

- Uncertainty about ACA repeal will disrupt the individual market, hike premiums, and limit plan options.

- Approximately 20 million people could become uninsured.

- Federal funding for health coverage could drop by nearly $135 billion.

- Approximately 135 million people with preexisting conditions could face discrimination from insurers in the individual market.

- Consumers could be hurt by the rollback of the ACA rule preventing insurers from overcharging for premiums, which has forced insurance companies to rebate $1.37 billion in 2019 alone.

Chaos in the insurance market

While the 5th Circuit’s decision pushes back the date that possible ACA repeal would occur, it cannot prevent uncertainty about repeal from wreaking havoc in the individual market. The annual rate submission process requires insurers to lock next year’s rates months ahead of open enrollment; they must file rates with their state insurance commissioner starting each spring, then submit final rates to the Centers for Medicare and Medicaid Services in August. Unless the Supreme Court resolves the case in the next few months, the ACA’s financial assistance will remain in jeopardy and the regulatory environment will be in flux; insurers are likely to hike premiums for 2021 in order to hedge against scenarios in which enrollment drops, subsidies disappear, or only the sickest enrollees remain in the risk pool. As a result, consumers seeking comprehensive coverage are likely to see much higher premiums for 2021 regardless of what eventually becomes of the ACA. Moreover, subsidized enrollees who need comprehensive benefits could be stuck with unaffordable coverage if the ACA is ultimately repealed by a Supreme Court ruling.

Some risk-averse insurers may simply flee the ACA market altogether, scrapping plans to participate in 2021. When “repeal and delay” proposals were on the horizon in 2016, the American Academy of Actuaries warned Congress that “increased uncertainty and instability” could cause insurers to exit, leading to “severe market disruption and loss of coverage.” If the 5th Circuit’s decision and the forthcoming declaration from the lower court end up spooking insurers out of the marketplace, consumers in some areas of the country may have limited options for individual coverage other than skimpy short-term plans that charge more for preexisting conditions and set limits on benefits.

20 million Americans could become uninsured

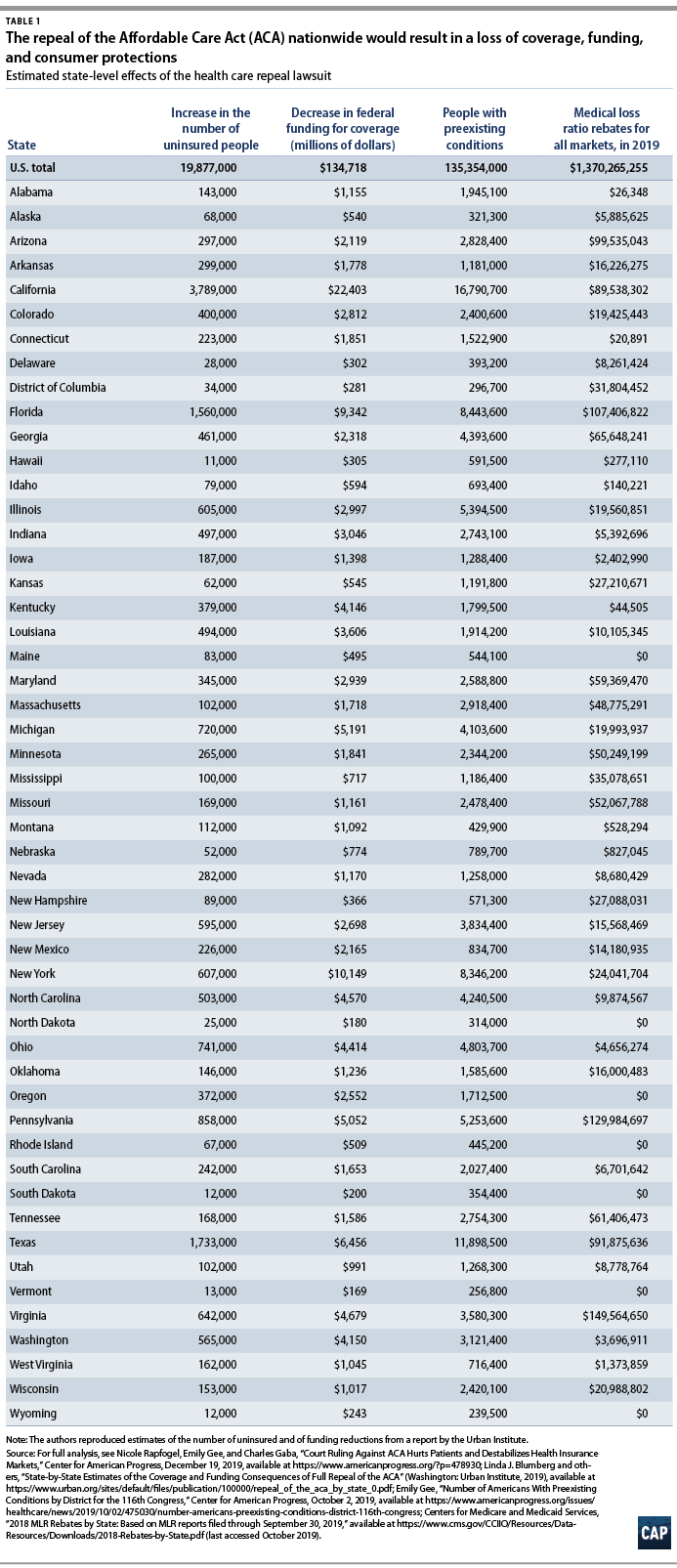

According to an Urban Institute study, without the ACA’s protections and financial assistance, an estimated 20 million Americans would become uninsured. (see Table 1) Breaking those numbers down by congressional district, the Center for American Progress estimates that an average of approximately 45,600 people would become uninsured in each district and Washington, D.C., if the ACA were fully repealed nationwide. (see downloadable spreadsheet) Another Urban Institute report finds that 5.4 million Latinx and 3.2 million Black Americans are among those who would lose coverage as a result of ACA repeal.

Many of the people at risk are lower-income individuals and families that are enrolled in Medicaid, including those covered by both preexpansion Medicaid programs and the ACA’s Medicaid expansion, in which the federal government pays at least 90 percent of the costs. In fact, more than half of those projected to become uninsured have family incomes of less than 138 percent of the federal poverty level. Cutting off the ACA’s tax credits and cost-sharing assistance for low- and middle-income families in the marketplace would leave enrollees without affordable options for coverage.

Federal funding could drop by $135 billion

According to the Urban Institute, a full repeal of the ACA would reduce federal funding for coverage by nearly $135 billion. This is the equivalent to losing an average of $309 million of federal funding in each congressional district. Moreover, these funding cuts translate to a 35 percent decrease in federal spending for marketplace subsidies, Medicaid, and the Children’s Health Insurance Program (CHIP). These federal dollars help people obtain coverage and, without them, working-class children and families across the nation will face devastating coverage losses. Based on the Trump administration’s budget for fiscal year 2020, this funding isn’t likely to be redirected toward other social and economic services; rather, President Trump’s fiscal focus remains on tax cuts for the wealthy and corporations.

No ACA means discrimination against people with preexisting conditions

The district court ruling could eliminate protections for the estimated 135 million nonelderly people with preexisting conditions. Under the ACA, individual market insurers cannot refuse to cover a person based on health status, a provision that nearly 3 in 4 Americans feel is “very important” to keep in place if the ACA is repealed, according to polling by the Kaiser Family Foundation earlier this year. Additionally, the ACA established community rating, prohibiting insurers from charging higher premiums for people based on their health needs or medical histories. Without these protections, however, insurers are likely to return to medical underwriting, discriminating against the less healthy when setting pricing, exclusions, and limits. Only seven states have pre-ACA laws on the books prohibiting medical underwriting.

In addition, there are other ACA provisions that are critical for people with preexisting conditions. For example, without the ACA, health plans would no longer be required to cover essential health benefits (EHBs). These 10 basic categories of services include hospitalization, maternity care, and mental health and substance use disorder services. Without the EHB requirement, insurers could refuse to cover certain costly services that many policyholders are likely to need; for example, an insurance company could refuse to cover cancer treatment in order to avoid policyholders with a history or high risk of cancer. People who needed coverage for nonincluded benefits would be forced to pay extra. In its analysis of the House’s ACA repeal bill, the Congressional Budget Office estimated that adding a coverage rider for maternity care would cost an enrollee more than $12,000 annually. Surcharges for other conditions could be even costlier. According to CAP analysis of an earlier ACA repeal plan under the Graham-Cassidy bill, if the legislation had passed, enrollees with drug dependence could have been charged an extra $20,450 and those with breast cancer could have been charged an extra $28,660 on top of standard premiums in 2026.

Many people outside the marketplaces, including those with employer-sponsored coverage, would also suffer if the ACA is ultimately repealed. Millions of Americans could face the return of annual or lifetime limits on the amount of medical care their insurance will cover. Furthermore, without the ACA, insurers would not have to offer preventive services—ranging from contraception to cancer screenings to vaccinations—at no cost to the patient, a change that has implications for both individual and population health.

Despite President Trump’s promises to protect people with preexisting conditions, none of the conservative options he backed in the congressional push for “repeal and replace” would have actually protected them. Insurance plans that lack basic benefits, as well as cruel tactics to keep profits in insurance corporations’ already full pockets, are likely to proliferate without ACA protections. The American people—particularly the roughly half of nonelderly adults with preexisting conditions—could be hurt by this disregard for their well-being.

Without ACA rules, insurers could charge Americans more for less coverage

If a full repeal takes place, the quality of individual coverage and the stability of the market will further degrade. In addition to the return of medical underwriting, there would be no national safeguard to prevent insurers from raising premiums while providing less coverage. Under the ACA’s medical loss ratio (MLR) rules, insurers must pay rebates to consumers if they overprice premiums relative to actual medical costs. Moreover, insurance companies that do not spend at least 80 to 85 percent of premium funds on medical care must issue rebates to consumers. Since 2011, insurers have returned approximately $5.3 billion in excessive premiums to policyholders, averaging $663 million per year. MLR rules protect consumers in all markets, including those covered by employer-sponsored insurance. In 2019, insurance companies have paid out a total of $1.37 billion in rebates, including rebates for 2.3 million people with large-group coverage through an employer. In Texas alone, insurers have paid $91.9 million in rebates.

Without the ACA, however, insurers could charge exceedingly high prices and use the revenue for executives’ salaries, advertising, marketing, and other means of maximizing profits at the expense of enrollees. Such practices are already common among short-term, limited-duration plans that do not have to comply with the MLR rules—also known as “junk” insurance plans. For an idea of what pricing might look like without ACA protections, some junk plans spend as little as 9 cents per premium dollar on medical care. Assisted by looser rules under the Trump administration, insurers have been trying to sell more of these plans in order to benefit their bottom lines, often using deceptive marketing tactics to dupe consumers into purchasing plans they think will provide comprehensive coverage. In the absence of ACA regulations, these junk plans and their damaging impact on Americans’ access to health care would only proliferate.

Conclusion

The 5th Circuit’s decision in the Texas v. United States health care repeal lawsuit furthers Trump’s commitment to putting partisan rhetoric over the livelihoods and health of the American people. The Trump-backed repeal lawsuit has pushed the nation closer to a reversal of preexisting condition protections and the coverage gains made under the ACA and, even with uncertainty about the ultimate outcome, will likely have near-term effects on the stability of insurance markets. The court’s decision is a brazen attack on health care. If the district court—and ultimately the Supreme Court—strikes down large portions of the ACA, there will be devastating impacts on health care for Americans across the nation.

Nicole Rapfogel is a special assistant for Health Policy at the Center for American Progress. Emily Gee is the heath economist at the Center. Charles Gaba is a health care analyst and the founder of and editor for ACASignups.net.