Read the fact sheet

This report contains a correction.

Introduction and summary

Americans from all backgrounds and politics agree: The rent is too damn high, and so are home prices.1 Housing affordability continues to rank as a top concern for the American people.2 In recent years, Americans have paid a growing share of their incomes toward rent or mortgages;3 roughly one-third of all American households—including half of all renters—are now considered “housing cost burdened,” meaning they spend more than 30 percent of their income on rent and mortgage payments.4 Home prices have risen nearly 55 percent since the start of the pandemic, and rent is up more than 30 percent nationwide,5 and even higher in many markets.6 The median first-time buyer age increased to 40 in 2025, the highest on record and up from 31 in 2014.7 Simply put: Housing is too expensive, and for too many Americans, owning a home feels like an impossible dream.8

Support work like this and advance bold, progressive ideas

The burden of soaring housing costs is primarily driven by the fact that the United States does not have enough housing to meet demand.9 Home construction in the United States fell significantly after the Great Recession, and we have not returned to pre-2008 levels.10 Figure 1 shows that housing completion plummeted in the 2010s and that the current completion level remains below the historical average. After years of underbuilding, we’ll need sustained, above-average production to bring supply back in line with demand and ease the affordability crisis.

Our biggest housing challenge is the lack of affordability, particularly in regions with the strongest job markets and economic growth, as well as in lower-income communities with high rates of poverty. Restrictive zoning and land-use rules that block multifamily and modest-lot homes; high financing costs that make new construction prohibitively expensive; and rising labor, materials, and regulatory expenses have together created a chronic undersupply of housing. At the same time, high insurance rates, rental market junk fees, excessive closing costs, and other unfair charges, along with the use of algorithmic rent-setting software that enables price collusion by landlords, are squeezing renters and homeowners alike, compounding the affordability crisis.11

Our proposed strategy recognizes the important role of demand-side measures, including rental assistance and efforts to boost first-time homeownership. But it is built on the fact that we cannot make headway on housing affordability over the long run without seriously scaling up home building at the same time. As Bernstein and Mahoney argue in a recent article on the economics of affordability, subsidies work “best in settings where supply is elastic enough to accommodate the increased demand. In supply-constrained markets, subsidies primarily result in higher prices.”12

The agenda that follows is not intended to be comprehensive; it does not include, for example, critical investments in rental assistance and public housing or offer policies to prevent and address the unacceptably high rates of homelessness. Rather, the plan considers a set of new policies that could surge new housing production over the next five years and deliver much-needed relief to renters and homeowners.

The Center for American Progress’ plan has three major components:

- Take down barriers that make it harder to build homes.

- Build more affordable homes at a lower cost.

- Protect consumers and lower other housing costs.

The plan invests federal dollars in models that are proved to build housing quickly and efficiently, while catalyzing state and local policy reforms that would unlock hundreds of thousands of additional homes at minimal or no cost.

To get a sense of the savings to renters and homeowners from the proposals that follow, consider the following scenarios:

- Renter in a high-cost area. A typical middle-income family renting in a high-cost, low-supply area could save $1,000 per year, with savings derived from direct rent relief, supply effects for added units, reduced junk fees, and preventing collusive pricing.

- First-time homebuyer. A family buying a typical home could save $24,000 on their first home, with savings derived from cheaper construction costs from exempting building materials from current tariffs, regulatory changes that increase supply and thereby lower future prices, lower insurance and title costs, and, in the case of modular housing, cost-saving productivity advanced from standardized building methods.

Overall, we project that this agenda could close the United States’ 2 million housing supply gap in five years, at a cost of roughly $95 billion (see Appendix for more detail).

Section I: We are not building enough homes in America

Though considerable geographic differences exist, on average, Americans are paying a larger share of their incomes for housing, with median home prices relative to median incomes climbing from about four times in the mid-1980s to about five times today.13 Moreover, the rent-to-income ratio has reached its highest level since 1980, and the average monthly mortgage payment as a share of new homebuyers’ income remains near historic highs.14

This rising cost burden is driven by insufficient supply of affordable homes. There is a well-established link between the price of a home or rent charged and the supply of available homes. According to one recent analysis covering homebuilding from 2017 to 2024, a 10 percent increase in a market’s housing supply correlated with a 5 percent decrease in rent growth, with the steepest declines in older and less expensive units.15 Other analyses have found that new home construction reduced the rents of nearby units of housing compared with those that are farther away.16

Figure 2 shows that, after facing a surplus 15 years ago, the nation now suffers from a deficit of about 2 million homes, with 1.2 million due to “pent-up households” that would have formed if housing had been more affordable and an additional 800,000 homes needed based on historical vacancy rates.17 This inclusion of pent-up households is important because it captures the fact that more than 1 million households would move if affordable housing were available. A census tract-level analysis by Moody’s Analytics and the Urban Institute found that the biggest supply shortfall exists for “middle-income” tracts where the average income is 80 percent to 120 percent of the median income for the metropolitan area.18

As the interactive maps below show, there are wide disparities at the local level when it comes to supply gaps and the extent of housing affordability challenges.

The Trump administration is making the housing affordability crisis worse

The Trump administration has worsened the nation’s housing shortage and made it harder for families to find and keep stable homes through a series of misguided actions, including withholding federal housing funds, cutting staff at the U.S. Department of Housing and Urban Development (HUD), and proposing to eliminate key programs that expand affordable housing and reduce rent burdens.19 It has also raised costs on key inputs: According to one estimate, the Trump administration’s broad tariffs on materials such as lumber, gypsum, and steel, along with fixtures like kitchen cabinets and bathroom vanities, will add roughly $135 billion to the costs of residential construction over the next five years.20 Further, the administration’s immigration policies will further slow and raise the cost of construction.21 Immigrants make up more than one-quarter of the construction workforce—and even higher shares in the skilled trades facing the most acute shortages.22 Already, nearly one-third of construction firms report being affected by current immigration enforcement activities, and 10 percent report losing workers.23

According to one estimate, the Trump administration’s broad tariffs on materials such as lumber, gypsum, and steel, along with fixtures like kitchen cabinets and bathroom vanities, will add roughly $135 billion to the costs of residential construction over the next five years.

Brookings Institution, "Recent tariffs threaten residential construction" (2025).

Bad local policies are a big problem, though fixing them alone is not sufficient

The shortfall in both rental and owned housing is, in part, a policy failure. The recently published book Abundance, by Ezra Klein and Derek Thompson, has helped spark a broad and robust discussion around barriers in place across the country that get in the way of building the housing that communities need.24 Land restrictions limit the building of new homes and significantly increase the cost of construction: About 75 percent of land in American cities is zoned for single-family homes, and many communities restrict certain types of construction, such as manufactured housing, limiting affordable access to higher-income neighborhoods.25 Zoning laws also often include detailed restrictions that limit density, including specifying minimum lot sizes, floor-area ratios, setbacks, height restrictions, and parking ratios.26

At the same time, addressing the housing affordability crisis at the speed needed by the American people means that cutting so-called red tape is not sufficient. Efforts to reduce barriers to production often take many years to bear fruit. Most studies of zoning reform, for example, typically estimate increases in housing supply 3 years to 10 years after the changes are made.27 Further, as Daniel Hornung and Aaron Shroyer write, “Zoning reform without better financing tools leaves housing production dependent on market cycles and unable to reach many rent-burdened households.”28 Thus, the plan below proposes policies both to incentivize the removal of needless barriers and to introduce new financing and other tools to accelerate the construction and preservation of affordable homes.

At the same time, addressing the housing affordability crisis at the speed needed by the American people means that cutting so-called red tape is not sufficient.

Section II: A plan to quickly build more housing and lower housing costs

The following proposals would help communities build more housing quickly—closing our housing gap over the next five years and delivering short-term relief for renters and homeowners.

Take down barriers that make it harder to build homes

Launch the Rent Relief for Reform (R3) program to provide rent relief to residents and push high-cost communities to remove barriers to building

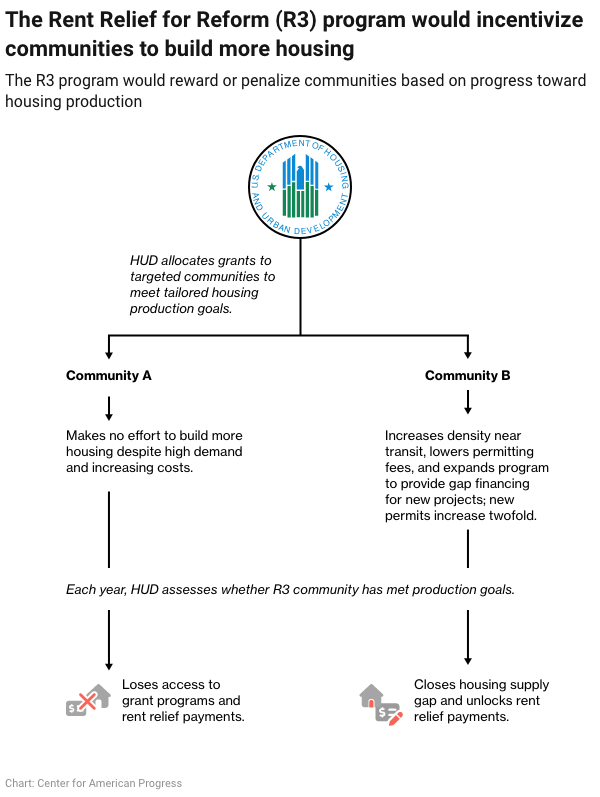

CAP is proposing the R3 program, a three-year effort to accelerate housing production and preservation and bring down the burden of rent in communities across the country. The R3 program would identify Housing Cost Crisis Zones (HCCZs)—jurisdictions across the country where rents are exceptionally high or rising rapidly and where housing supply has failed to keep pace with demand. The initiative is designed as both a “carrot” and a “stick”: In HCCZs, if local governments take timely action to expand housing supply—steps that have been shown to lower costs over time—the federal government will provide all renter households with annual rent relief payments to reduce their rent burdens right away. Communities that fail to meet identified production targets, on the other hand, will lose access to key discretionary, competitive grant programs (many of which are typically oversubscribed with applicants) for transportation, economic development, and other priorities.29 By offering concrete, short-term financial gains for communities that expand housing—and penalties for those that don’t—the program will motivate jurisdictions to pursue ambitious growth while ensuring residents experience the upside of needed new housing development in the short term.

Program details

While housing affordability is a growing challenge nationwide, it is especially acute in certain communities—particularly places with rapid job growth, restricted land supply, or long-standing disinvestment. The map below provides county-level information on key metrics that could inform program targeting, including housing affordability and rates of housing production.

Under the proposed R3 program, HUD would enter into “affordability contracts” with targeted HCCZ jurisdictions, for whom HUD would set housing supply targets based on local shortages, density, growth potential, and other factors, and put in place a plan for addressing them. At the outset, HUD would provide grant funding to HCCZs to support local planning and the establishment of new financing tools. While communities must demonstrate real progress in building more homes, they would retain flexibility to pursue the strategies that work best locally. These could include zoning and land-use reforms, streamlined permitting, reduced fees, and limits on the ability of local officials to block projects. Participating communities could also launch or expand proven initiatives to accelerate affordable housing development, such as through tax credits, targeted subsidies, or innovative financing models.

Over the course of the program, cities would be required to show measurable progress toward closing their housing supply gaps. By the end of the first year, progress would be assessed based on concrete steps to remove barriers to housing production. In succeeding years, jurisdictions would be evaluated on quantitative outcomes, including increases in permitted or completed housing units.

Over the first three years of R3, renters would receive up to $1,000 rent relief payments for each year that their communities meet their targets—directly linking local results to tangible savings for renters. The size of the grant—and therefore the size of rent relief payments—could be tied to the extent of progress in housing production. By making both the availability and size of rent relief contingent on housing production and only available for a limited amount of time, policymakers can better safeguard against the risk that landlords will simply raise rents in response to the program. Many renters in the HCCZs that deliver on building new homes could effectively see reductions in rent burden over the first three years of the initiative. Then, as new homebuilding ramps up, housing costs are likely to grow at a slower rate or decline over the longer term. Conversely, communities that fail to make reasonable efforts to meaningfully expand housing supply would not only be denied funding to provide rent relief payments for residents but also lose access to certain discretionary federal grant programs to improve local infrastructure and advance economic development priorities.

![]()

By targeting metropolitan areas most in need of supply, R3 could save a typical renter household up to $1,000 per year, when coupled with savings on junk fees and preventing rent-setting collusion as outlined elsewhere in this report.30 The chart below shows the potential benefit to renters in hypothetical examples from Cook, Los Angeles, and Philadelphia counties.

In addition to the R3 program, which targets high-cost, low-supply places across the country, CAP supports new incentives for state and local governments, including those that are not participating in the program, to reduce barriers to homebuilding. Building on the innovation fund contained in the bipartisan ROAD to Housing Act,31 the federal government should incentivize high-impact state and local reforms through new competitively awarded grants that can be used to help communities manage the impacts of greater housing density through investments in roads, transit, sewer and water systems, and schools.32 Grants could be awarded to states and jurisdictions that advance pro-housing policies resulting in the highest levels of housing production and preservation. In addition, absent new federal funding, the federal government can give more weight in competitive grant opportunities to applications from localities that streamline the process for building homes.

Build more affordable homes at a lower cost

The federal government should do more to promote the development of more affordable homes by catalyzing factory-built homes and components and investing in programs proven to build affordable housing at a lower cost.

Drive down the costs of construction by scaling up factory-built homes

CAP recommends that the federal government accelerate the growth of off-site building and drive innovation in housing construction. A manufactured home is a factory-built residence constructed on a permanent steel chassis and built to HUD code, whereas modular and panelized homes are factory-built dwellings produced in sections or panels, transported to the site, and permanently assembled on a foundation in compliance with the same state and local building codes that apply to site-built homes. Despite being one of the most cost-effective ways to expand homeownership, manufactured housing often faces local zoning and land-use barriers that limit where these homes can be located. And because many manufactured homes are titled as personal property rather than real estate, most buyers must rely on chattel loans, which typically have higher interest rates and shorter terms than traditional mortgages.33

Further, construction as a sector has seen a long-term productivity lag: Between 1970 and 2020, U.S. construction labor productivity fell by more than 30 percent even as overall economic productivity roughly doubled. Despite significant gains following World War II, the number of homes built per construction worker has been trending down since roughly 1970—underscoring the need for modernization and process innovation.34

CAP proposes the following actions to help accelerate production, lower costs, and increase access for factory-built homes:

- Catalyze housing innovation. CAP recommends a new federal initiative—called Advanced Research Projects Agency-Home (ARPA-Home)—to fund, incubate, and scale innovations that can dramatically expand housing production, cost-reducing energy efficiency and resiliency, and affordability. Modeled on the successful ARPA framework that launched DARPA in defense, ARPA-E in energy, and ARPA-H in health, this new entity would back “big-bet” technologies and approaches to lower costs and speed up homebuilding nationwide. The effort would build on Operation Breakthrough (1969–1974), an effort by then-HUD Secretary George Romney that demonstrated the potential of modular construction, producing nearly 20,000 units across nine cities.35 Under ARPA-Home, the federal government would provide financing to support innovation in building processes, materials, and factory capacity, while states and regions could form compacts to address outdated zoning and land-use rules that limit this type of housing. And the federal government could help the industry achieve better economies of scale by leveraging its purchasing power.36 Through traditional procurement authorities or tools such as the Defense Production Act, the federal government can help scale and expand the modular industry, which has yet to reach sufficient scale and broad enough geographic scope to bring down construction costs.37 For example, the Department of Defense could launch an effort to upgrade its aging military base housing stock through modular home production.38

- Modernize HUD building codes for manufactured homes to reduce costs. CAP recommends changing federal law to remove a decades-old requirement that every manufactured home has a permanent, steel chassis base beneath it. This requirement, intended to ensure portability despite the fact that the vast majority of these homes are never moved, increases costs, reduces flexibility of design, and precludes basements and upper-floor construction.39 This policy change, which is included in the bipartisan ROAD to Housing Act,40 would reduce the cost of these homes by $5,000 to $10,000, by one estimate.41

- Make it easier to buy a manufactured home. CAP proposes that federal housing insurance and guarantee programs expand access to affordable financing for manufactured homes to ensure greater parity between financing options for purchasers of manufactured housing and purchasers of site-built homes. The government-sponsored enterprises (GSEs) should help create a secondary market for personal property loans.42 This would expand lender participation, increase access to lower-cost credit, and make home purchases more affordable for manufactured homebuyers.

Invest in programs that build middle-class homes at a lower cost

Affordable financing remains a major barrier to new housing production. CAP proposes that Congress act to authorize and fund two approaches to building new homes for middle- and low-income households.

First, Congress should pass the bipartisan Neighborhood Homes Investment Act to build and preserve affordable owner-occupied family homes. The proposal would provide federal tax credits to developers and investors to cover the gap between construction or rehabilitation costs and a home’s market value in distressed neighborhoods, making it financially feasible to build or renovate owner-occupied homes.

Second, Congress should authorize dedicated federal funding to support the expansion of a fast-growing model of affordable housing development, where the public sector acts as an investor and owner in building mixed-income developments, as adopted by states and communities such as Massachusetts, Michigan, and Montgomery County, Maryland.43 This approach features a public entity—such as a land bank or public development authority—that leverages a revolving loan fund, capitalized in part by public funds, that provides lower-cost capital to finance the construction phase of projects.44 The construction phase for market-rate projects is the costliest phase,45 with banks typically offering higher rates and shorter-term loans that do not cover the full cost,46 leading many developers to turn to private equity for higher-cost loans. Rising interest rates have led to a major spike in the number of stalled private multifamily projects that are permitted but are not yet built.47 In August 2025, this number was roughly 115,000, up from 81,000 at the same point in 2019, providing policymakers with an opportunity to rapidly scale up housing development if lower-cost construction capital can be put on the table.48

Under this model,49 the public entity offers lower-cost lending—often targeting projects that are permitted but not yet built due to the cost of capital—and ensures that a portion of the units are affordable for working families.50 Once the project is complete, the public entity retains a controlling ownership stake in the building, often with a private partner managing the property, and rents collected fund operations and help recapitalize the revolving fund to support future projects.51 Federal funds can scale up these programs further and compel other governments to follow their lead.52 A focus on unlocking stalled market rate development projects,53 with a portion of units set aside as affordable as a condition of cheap construction financing, would ensure more bang for the buck in terms of units produced for every federal dollar. A host of states and cities are in the process of launching programs,54 including Atlanta, Chicago, Seattle, Chattanooga, and Raleigh, along with the states of Rhode Island and Hawaii.

Protect consumers and lower other housing costs

Despite many tools at its disposal to lower housing costs in the short term, the Trump administration has proved unable or unwilling to use them. While this report has thus far focused on increasing the supply of housing, this section highlights missed opportunities to lower housing costs now.

Exempt building materials from the Trump administration’s tariffs

The Trump administration should exempt building materials from its overly broad tariffs, a move that would quickly reduce the costs of building a new home by nearly $11,000 by some estimates,55 as 7 percent of all goods used in new construction are imported.56 Exempting building materials could generate substantial savings. Based on analysis from the Urban Institute-Brookings Tax Policy Center, CAP estimates that exempting building materials would result in savings of $135 billion in construction costs of new homes and apartments over five years.57 This exemption would also boost homebuilding, as some experts estimated that the Trump administration tariffs would reduce construction output by nearly 4 percent over time.58

Prevent misguided GSE ‘reforms’ that would increase mortgage costs

The GSEs serve as critical, behind-the-scenes pillars of the U.S. housing finance system, supporting access to the 30-year fixed-rate mortgage and enhancing housing affordability by adding liquidity to the mortgage-lending market.59 In the run-up to the 2008 housing crisis, the GSEs became severely undercapitalized due to excessive risk-taking, leading to government intervention and their ongoing placement in federal conservatorship, where their regulator acts as a caretaker to keep them financially stable and ensure they can continue to support vital access to mortgage credit for homeowners and rental housing owners.60

The Trump administration is considering ending Fannie and Freddie’s conservatorship and conducting an initial public offering-like process where investors are invited to purchase shares in the companies.61 This strategy could compromise critical changes made to the two companies since the 2008 crisis and is highly likely to lead to higher mortgage rates—moving the wrong way on housing affordability. Analysts estimate that the floated Trump reforms to the GSEs, depending on the proposal, could raise mortgage rates by 0.2 percentage points to 0.8 percentage points for the typical homebuyer, translating into an increase in payments of $500 to $2,000 per year for the typical homebuyer.62

Therefore, while ending the decades-long conservatorship may be desirable, we would not endorse any such plan that raised mortgage rates, which are already elevated relative to their levels over the past decade. Any reform must maintain at least the current level of affordability,63 and in fact should go further.

Put Fannie and Freddie to work to speed up housing construction

CAP proposes that the GSEs permit the upfront purchase and securitization of “single-close” construction-to-permanent loans. While Fannie Mae and Freddie Mac already allow single-close construction-to-permanent loans, they do not currently buy or securitize them until construction is complete—leaving lenders to hold the loan on their balance sheets.64 To manage any additional risk from guaranteeing the construction phase of the loan, the GSEs could model a pilot program after existing renovation loan structures, such as Fannie Mae’s HomeStyle Renovation Mortgage program, that already manage a degree of construction risk through tighter approval processes.65 Allowing for upfront securitization will reduce financing costs and increase lender participation in new construction finance.66 The Mortgage Bankers Association has called on the GSEs to pilot a securitized one-time close construction loan product.67

Crack down on costly frictions in housing transactions

Federal agencies could save homebuyers thousands of dollars in closing costs with a few targeted reforms. Today, buyers are required to pay for services such as lender’s title insurance and home appraisals, even though these products primarily protect the lender, not the borrower.68 Title insurance premiums cost more than $2,000 for a median home but pay out just 3 percent to 5 percent of premiums in claims—far below the 70 percent or more typical of other types of insurances, such as health and auto insurance.69 The Consumer Financial Protection Bureau (CFPB) should propose a rule requiring lenders to cover these costs themselves. Since borrowers can shop around for a mortgage, lenders would face competitive pressure to absorb the cost rather than pass it on to consumers. The Federal Housing Finance Agency (FHFA) should also act on title insurance by expanding the pilot it launched in 2024 to waive title insurance on a limited number of refinance transactions.70

Prevent the use of rent-setting software platforms to collude to jack up prices

CAP recommends federal legislation to make it unlawful for property owners to use software that facilitates collusion by setting rents that leverage rental pricing and supply data gathered from landlords that would otherwise compete for tenants. A 2024 analysis by the White House Council of Economic Advisers found that renters of apartments in buildings covered by these algorithmic pricing software platforms pay more than $800 per year in additional rent compared with renters in buildings that do not use these platforms. Federal agencies, including HUD and the FHFA, should also take action to combat algorithmic rent-setting in properties they control.71

Ensure homeowners can access affordable insurance

To help homeowners afford rapidly increasing home insurance premiums and address the exit of insurers from some geographic areas,72 CAP recommends a federal reinsurance program to stand behind state insurers of last resort. Congress should enact a federal reinsurance plan to back up state-run nonprofit Fair Access to Insurance Requirements (FAIR) plans, which help homeowners who are unable to find private homeowners’ insurance due to high risk in 34 states and the District of Columbia.73 As private insurers increase their premiums and move out of high-risk areas,74 an increasing number of homeowners are turning to FAIR plans. Federal reinsurance of these plans would bring down costs for homeowners and for private insurers, who bear the cost of FAIR plan shortfalls, making it less likely that insurers will exit the state and avoiding inefficiencies and disincentives associated with direct subsidies to homeowners or direct interference in the private insurance market.75 Acceptance into the federal reinsurance program should be contingent upon both state government and private insurer actions to improve resiliency and lower costs.

Eliminate junk fees in rental housing

Renters encounter surprise and unfair fees at every step of the rental process.76 Even searching for an apartment can be costly: Prospective renters often spend $35 to $75 or more just to apply; in a hot rental market in which people often apply to many apartments, this can add up to hundreds of dollars without any guarantee of success.77 Once in a new home, renters pay up to hundreds of dollars in fees for sorting mail or simply paying rent online.78 CAP proposes capping credit check fees at the actual cost of running the check—typically around $20 or more79—and allowing renters to pay once and use a single, reusable rental application for multiple properties. CAP also supports action by the Federal Trade Commission to broaden its junk fee rule to ban hidden fees that show up on leases.

Conclusion

Americans face a deepening crisis of opportunity and economic mobility. Rising housing costs, driven by a deep and persistent gap in housing supply, are pushing individuals and families to their limit, making it harder to cover basic expenses—let alone take the first step of achieving homeownership. Addressing this crisis demands bold and urgent action. This report provides new recommendations for policymakers to rapidly increase the production and preservation of affordable homes while providing relief to renters and homeowners right away.

Acknowledgments

The authors would like to thank Daniel Hornung, Mark Zandi, Cristian deRitis, Jim Parrott, Sarah Brundage, Aaron Shroyer, and Megan Cheney for their thoughtful feedback on this report.

The authors would also like to thank Emily Gee, Lily Roberts, Mimla Wardak, and Corey Husak for their valuable contributions and support, as well as Kyle Ross, Aurelia Glass, and Brian Keyser for their fact-checking of this report. A particular thank you to Amina Khalique, who provided significant project management and research support, as well as Kennedy Andara, who prepared the visualizations and graphics. The authors would also like to thank the production team involved in the preparation of this report, including Will Beaudouin, Meghan Miller, Bianca Serbin, Bill Rapp, Anh Nguyen, and Chester Hawkins.

Appendix: Estimated costs and impacts of CAP’s housing supply recommendations

Based on the initiatives detailed in this report, CAP’s plan to close the supply gap is estimated to cost roughly $95 billion over five years. Note that the indicative housing unit counts detailed in the table below do not capture interaction effects between the policies included in this plan.

The renter scenario is estimated based on a renter household in a high-cost, low-supply area where the area is fully compliant with requirements to expand housing supply, meaning that the household qualifies for the full rent relief payments in years 1 through 3. Rental savings are estimated based on an indicative reduction in rental cost growth in years 3 through 5, drawing on recent studies that estimate how increased housing supply affects rents and the time taken for additional supply to be added to the market. This amount is expected to increase over time, beyond the five-year time period. Indicative savings on junk fees are based on an example of a renter applying to four separate properties, with an application fee of $20 rather than $35 to $100.

The homebuyer scenario applies to a first-time homebuyer purchasing a median home in year 5, following the implementation of this plan. Savings on purchasing a home are estimated based on an indicative reduction in house price growth in years 3 through 5, drawing on recent studies that estimate how increased housing supply affects prices and the time taken for additional supply to be added to the market. This amount is expected to increase over time, beyond the five-year time period. Tariff savings assume an 80 percent pass-through of reduced construction costs to consumers.