Introduction and summary

The Trump administration frequently pushes natural gas exports in high-level talks with Beijing. Most recently, after threatening to impose tariffs on Chinese technology imports, some administration officials are stating that the tariffs can be reduced if China buys more U.S. natural gas.1 The Trump administration is pitching a very simple argument: If China imports more natural gas from the United States, that will help rebalance the U.S.-China trade deficit—which rose to a record $375.2 billion during President Donald Trump’s first year in office—and generate American jobs.2 In reality, that argument reflects a deep misunderstanding about how today’s global energy markets actually work.

At first glance, the United States and China do have good synergies in this sector. China is consuming more natural gas than it can produce and seeking new imports; the United States is the world’s largest producer, and the Trump administration wants to send more of that production overseas. Trump routinely uses his meetings with President Xi Jinping and other Asian leaders to push natural gas export deals. That push played a role in preliminary U.S.-China deals inked last November and is generating excitement on both sides of the Pacific about a potential U.S.-China natural gas trade boom.

Behind the hype, however, market realities suggest this will not pan out as promised. This report covers the following five factors that American observers need to understand about the Trump administration’s push to export U.S. natural gas to China:

- Beijing is currently leveraging natural gas imports to fill a reform gap: Demand-side reforms have thus far been more successful than the supply-side. If Chinese leaders can push forward needed reforms on the supply side, the nation’s import dependence may decrease.

- China already has 26 supplier nations, and the shipments it receives from the United States are more expensive than 83 percent of its import supply chain.3

- The United States has a geographical disadvantage exporting to China and is better placed to serve other growing markets.

- The Trump administration is pushing U.S.-China natural gas investment deals that ignore current market trends.

- The Trump administration’s fossil fuel obsession risks forfeiting a much bigger strategic game in clean energy technology.

Chinese President Xi has big ambitions. His vision for an ideal future U.S.-China economic relationship is one in which the United States exports commodities to China while China steadily edges the United States out as the dominant player in global high-tech markets, including clean energy markets. In that scenario, the United States gets the lower end of the value chain and China dominates the higher end, thus winning the best jobs. Chinese leaders know that, globally, the world is already installing more new renewable energy generation capacity than new fossil fuel-based capacity.4 Even major oil and gas exporters such as Saudi Arabia and the United Arab Emirates are investing billions in renewables—they see where the market is headed and do not want to be left behind. Chinese leaders view clean energy as a major battlefield in their nation’s quest to surpass the United States as the new high-tech superpower, and entertaining the Trump administration’s fossil fuel export initiatives is a useful tactic for keeping the United States occupied on the sidelines while China runs the field.

There is little question that China’s rising natural gas consumption is an exciting trend. If Beijing leverages natural gas to replace coal and reduce the nation’s overall fossil fuel emissions—neither of which is guaranteed—that could be good for the planet. However, this trend is unlikely to generate game-changing jobs for the United States, and the Trump administration’s determination to promote fossil fuel exports at any cost undermines broader U.S. economic interests. If the administration accepts natural gas export promises from China in exchange for backing off from much broader U.S. trade complaints—as U.S. Secretary of Commerce Wilbur Ross is suggesting—that will undercut the U.S. economy even further.

Understanding these dynamics is critical for assessing what the current administration’s U.S.-China natural gas initiatives are likely to produce over the longer term.

Beijing is currently leveraging natural gas imports to fill a reform gap

Demand-side reforms have thus far been more successful than the supply-side

China is a major natural gas producer and consumer. For decades, Beijing controlled pricing and activity on both sides of the market—production and consumption—and those controls hindered natural gas development in China. Natural gas currently accounts for just 7 percent of China’s total energy consumption compared with 29.2 percent in the United States, 23.7 percent in Germany, and 22.5 percent in Japan.5 Over the past five years, Chinese leaders have rolled out a series of policy reforms designed to relax the old controls, create more room for market competition, and encourage more production and consumption.

Those reforms have been particularly successful on the consumption side. Beijing is aiming for natural gas to account for 10 percent of the nation’s energy mix by 2020—up from 7 percent at year-end 2017—and 15 percent by 2030.6 To make that happen, Beijing is rolling out an array of environmental policies that provide new incentives—and in some cases mandatory requirements—for switching to natural gas as a substitute for more emission-intensive fossil fuels. That effort began with the 2013 Air Pollution Control Action Plan, which required major urban areas along China’s eastern seaboard to reduce their overall coal consumption, close down coal-fired industrial boilers and power plants, and bring in natural gas and renewables as substitutes by 2017.7 That 2017 deadline, however, triggered major natural gas supply shortages last fall as some city planners—anxious to meet their 2017 deadlines—shut down coal-fired power before they had substitutes in place to cover winter heating needs.8

In addition, Chinese leaders are also rolling out policies to encourage natural gas use for transport. Transport emissions account for around 25 percent of air pollution in China, and Beijing views switching to natural gas vehicles—both liquid and compressed natural gas—as a key lever for reducing pollution.9 China had more than 5 million natural gas vehicles in 2017—accounting for more than 20 percent of the global total—and Beijing is pushing to double that to 10 million by 2020.10 To meet that target, local governments across China are providing consumers with a variety of subsidies for natural gas fuel and vehicle purchases.11

These demand-side policies are having an impact. Between 2013—when Beijing first launched the Clean Air Action Plan—and 2017, China’s total natural gas consumption grew 41 percent, averaging roughly 9 percent growth per year.12 As consumption rises, Beijing is also rolling out three major supply-side reforms to drive domestic production—China has both onshore and offshore reserves—and imports.

First and foremost, Chinese leaders are taking steps to liberalize natural gas pricing. The first big shift occurred in July 2013, when Beijing rolled out a new pricing model for industrial-use gas that linked city-gate prices—or municipal-level distribution prices—to international market rates for fuel oil and liquid petroleum gas.13 Central planners used those international rates to set price ceilings and then allowed buyers and sellers in China to negotiate up to that ceiling. Beijing then took an even bolder step with unconventional gas, which is generally more expensive to develop in China. Starting in the second half of 2013, Beijing fully liberalized pricing for shale gas, coal bed methane, coal-to-gas, and imported liquefied natural gas (LNG)—suppliers in those sectors could charge whatever buyers were willing to pay.14 Over time, Beijing has also gradually broadened the band in which conventional natural gas prices could fluctuate, allowing more room for buyers and sellers to negotiate prices based on supply and demand.15

China’s old natural gas price regime

Prior to the recent price reforms, government planners controlled prices at every step in China’s natural gas value chain. Beijing dictated the ex-factory or production price on the upstream side, city-gate or city-level distribution prices on the downstream side, and at every other point natural gas changed hands. Beijing’s primary goal was to keep natural gas affordable for end users, so prices varied by location and end use depending on what Beijing thought local people could pay. Producers could not charge higher prices during supply shortages and thus had no incentive to invest in additional exploration and development. Shortages were a persistent problem, and domestic production was particularly sluggish in unconventional gas plays—such as shale gas—that require significant upfront costs to get around unique technical challenges in China.16

Price reform is still a work in progress, but these measures are already having an impact. Before the reforms commenced, China’s city-gate prices were well below international rates.17 That was a serious problem for China’s oil and gas majors who were signing import contracts with foreign suppliers and, due to the price spread between international and domestic rates, selling the imported gas at a loss in China. In 2012, PetroChina lost $6.7 billion importing natural gas into the country and selling it at state-controlled rates.18 In 2013, PetroChina’s losses increased to $7.9 billion—including a $4.6 billion loss on pipeline imports from Central Asia, a $67 million loss on pipeline imports from Myanmar, and more than $3.2 billion in losses on imported liquefied natural gas.19 Those losses declined when Beijing implemented the price reforms and domestic prices began to more closely track international rates.20 On the consumer side, however, the initial reform-induced price increases dampened consumption, and that created an entirely different headache for Chinese leaders given their goal to expand natural gas use.21 Since 2014, a steady decline in global oil and gas prices has made it possible for Beijing to liberalize pricing while also maintaining affordability for end users.22 If global prices trend in the opposite direction, that will make things difficult for Beijing, but that is unlikely given that the global natural gas market appears to be entering a period of oversupply.23

Second, in addition to price reform, Beijing also opened up liquefied natural gas imports for private sector participation. China’s state-owned enterprises have a monopoly on pipeline imports and domestic production—they dominate the best gas plays—but private enterprises can now enter the upstream market via LNG. If those imports entailed the kind of multibillion-dollar losses PetroChina suffered in 2013, there would be few takers; however, from 2014 onward, the combination of declining global LNG prices and an increasingly liberalized domestic pricing regime made the LNG import business a more favorable proposition. From 2014 to 2016, China’s average LNG import price fell from an all-time high of $12.64 per thousand cubic feet to $7.05 per thousand cubic feet; in 2017, prices ticked up 12 percent to $7.91 per thousand cubic feet but remain much lower than previous years.24 Private companies have two options for market entry: utilize existing terminals or build their own. Beijing’s 13th Five-Year Energy Development Plan, issued in 2013, encouraged private companies to invest in the natural gas sector, with one private company even permitted to construct and operate its own import terminal beginning in 2012.25 In 2014, Beijing ordered the nation’s state-owned oil and gas majors to grant private companies access to their unused import terminal capacity so that more private companies could take advantage of falling global LNG prices.26 Back in 2012, China had just six import terminals across six ports with a total import capacity of less than 3 billion cubic feet per day (Bcf/d); by year-end 2017, China had 17 terminals across 14 ports with a total 7.4 Bcf/d of capacity.27

Third, Beijing is taking steps to gradually relax state-owned enterprise control over domestic production. If Chinese leaders can break open their nation’s upstream sectors, that will be the real game-changer. The U.S. Energy Information Administration estimates that China may have as much or more shale gas than the United States, but development has been sluggish.28 Overall, China’s annual domestic production growth has decelerated from more than 19 percent in 2005 to less than 12 percent in 2010 and just over 2 percent in 2015.29 Chinese leaders are hoping to turn that trend around. Beijing’s 13th Five-Year Plan for Natural Gas Development targets 7.3 trillion cubic feet of production by 2020, up from 4.8 trillion in 2015.30 In 2016, year-on-year growth in China’s reported domestic production bounced back to just more than 5 percent.31 In the United States, private sector competition played a key role in driving some of the technology and process innovations that unlocked shale gas development.32 For that to happen in China, Beijing will have to break down an array of market barriers that currently stifle competition in the nation’s upstream sectors. For example, state-owned companies control the best oil and gas plays and, in some cases, sit on them without either developing them or allowing other companies to do so. China’s geological data is classified, so private companies and investors have no idea how much natural gas the country has or where it is located. Plus, state-owned companies control the pipelines and often either deny pipeline access to private companies or charge exorbitant rates, thus making it hard to bring those extra supplies to market.

Beijing is taking steps to address these problems, but progress has been slow, so they are currently relying on imports to meet the nation’s rising demand.33 Going forward, however, if Chinese leaders get serious about supply-side reform, the next unconventional gas revolution could occur in China. As of 2017, China is already the third-largest global shale gas producer behind the United States and Canada.34 Natural gas exporters should take China’s production potential into account—and Beijing’s growing determination to unlock that potential—when making investments that hinge on a continued rise in Chinese import demand.

China already has 26 supplier nations, and U.S. shipments are more expensive than most

China has been a net natural gas importer since 2007, and the gap between domestic production and consumption has grown steadily since then. China imports natural gas via a combination of overland pipelines and seaborne tankers.35 In 2017, 55.7 percent of China’s natural gas imports by volume came in via LNG tanker and 44.3 percent via overland pipeline.36

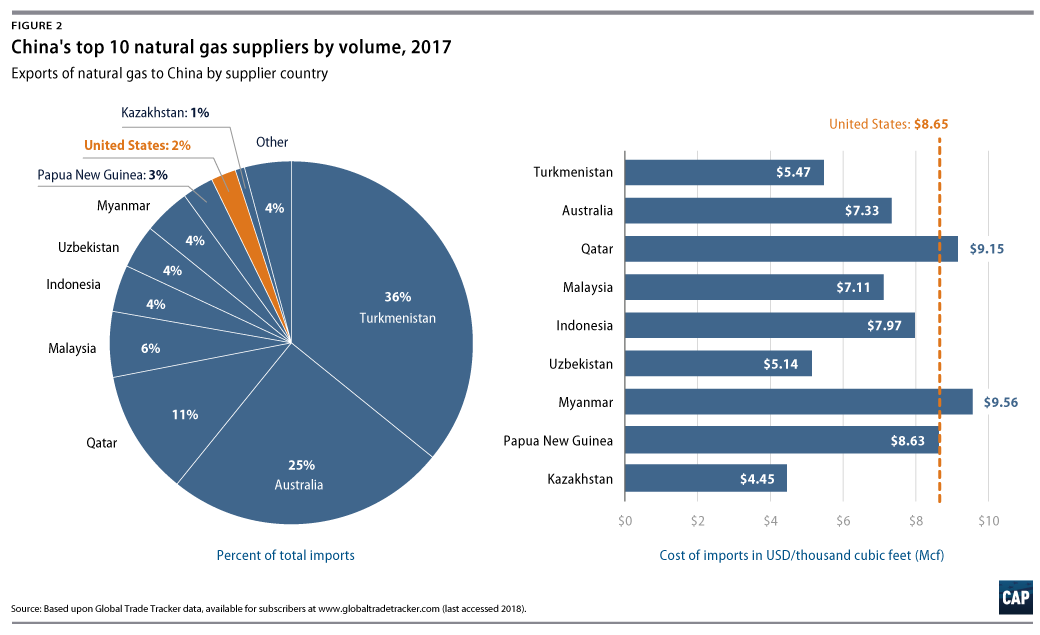

On the seaborne LNG side, China’s first imports came from Australia in 2006.37 In the late 2000s and early 2010s, smaller suppliers—including Algeria, Yemen, and Nigeria—also shipped LNG to China, but as of 2017, only Australia, Qatar, Malaysia, Indonesia, Papua New Guinea, and the United States occupy China LNG import market shares above 3 percent. The United States did not join China’s LNG supply chain in earnest until 2016. U.S.-to-China year-on-year LNG exports grew 217 percent in 2016 and 670 percent in 2017, at which point the United States edged out Nigeria to become China’s sixth largest LNG supplier. Australia has retained its position as China’s top LNG supplier by volume, except for the period from 2012-2015 when a bump in Qatari exports overtook Australia’s.38

On the pipeline side, China borders multiple onshore natural gas supply regions, and the nation’s state-owned energy companies have invested billions of dollars to bring in natural gas via overland pipeline.39 China generally pays less for pipeline gas than it does for seaborne LNG. For example, in 2017 China paid an average US$5.75 per thousand cubic feet for pipeline gas and an average US$7.91 per thousand cubic feet for seaborne LNG.40 Currently, China’s biggest pipeline supply route is from Turkmenistan, which supplied 80.5 percent of China’s piped natural gas imports in 2017. The rest of China’s pipeline natural gas imports come from Uzbekistan (8.5 percent), Myanmar (8.3 percent), and Kazakhstan (2.7 percent).41 Once the Myanmar and Kazakhstan pipelines came online in 2013, pipeline gas surpassed LNG as China’s primary import source but that reversed again in 2017, following Turkmenistan pipeline supply problems and a dip in global prices that narrowed the price gap between LNG and pipeline gas and thus made seaborne LNG more economical for Chinese buyers.42 China’s first pipeline from Russia is scheduled to come online in December 2019; once that pipeline is flowing, Russia is expected to become China’s top overland supplier, bumping Turkmenistan from the number one spot.43

Overall, in 2017, China imported 3.35 trillion cubic feet of natural gas—of which 1.48 trillion cubic feet came in via pipeline and 1.87 trillion cubic feet as LNG—making China the world’s second-largest natural gas importer, behind Japan.44 In 2017, China’s top five natural gas suppliers by volume—pipeline gas and LNG combined—were Turkmenistan (accounting for 36 percent of total imports), Australia (25 percent), Qatar (11 percent), Malaysia (6 percent), and Indonesia (4 percent). Beijing wants the nation’s supply mix to prioritize diversity—importing from multiple nations across a variety of transport routes and contract structures—and affordability.45 A diverse mix of suppliers and transport routes serves as a hedge against supply shocks and also provides multiple ports of entry to channel natural gas into different Chinese regional markets.46 When China first became a net importer in 2007, it received shipments from just four nations; today, 26 nations supply natural gas to China.47

U.S. natural gas exports to China did not begin in earnest until August 2016, when Houston-based Cheniere Energy began shipping LNG to Chinese buyers from its Sabine Pass liquefaction facility.48 In 2016, China imported 17.2 billion cubic feet of LNG from the United States.49 In 2017, that increased to 100 billion cubic feet,50 making the United States China’s ninth-largest natural gas supplier behind Papua New Guinea. All of the U.S.-to-China shipments departing in 2017—29 total cargoes totaling 100.01 billion cubic feet51—came from Cheniere’s Sabine Pass facility.52 Cheniere has a unique toll gate business model: The company is not directly involved in production. Instead, it purchases gas from U.S. producers, liquefies it at Sabine Pass, and sends it overseas. When Cheniere signs long-term contracts, it is not agreeing to produce a set amount of gas but rather to procure and liquefy it on the buyer’s behalf. In February, Cheniere Energy inked a long-term deal with China National Petroleum Corporation to supply up to 1.2 million tons—58.4 billion cubic feet—of LNG per year until 2043.53 Cheniere can fill those shipments with a combination of spot market purchases—taking advantage of price dips wherever possible—and longer-term supply contracts with producers willing to supply larger shipments to Cheniere at wholesale rates.

Although Cheniere’s unique business model is doing well exporting limited amounts of LNG to China, overall, the United States has not played a major role in China’s supply chain because U.S. LNG is generally not cost competitive in China. In 2017, China paid an average US$8.65 per thousand cubic feet for imports from the United States and an average US$6.95 per thousand cubic feet for all other natural gas imports. Based on 2017 pricing, U.S. imports are more expensive than 83.6 percent of the natural gas China obtained from other suppliers.54 Within China’s seaborne LNG supply chain alone—not including pipeline gas—U.S. imports are more expensive than 73.8 percent of China’s imports from other suppliers.55

The United States has a geographical disadvantage exporting to China

The United States is better placed to serve other growing markets

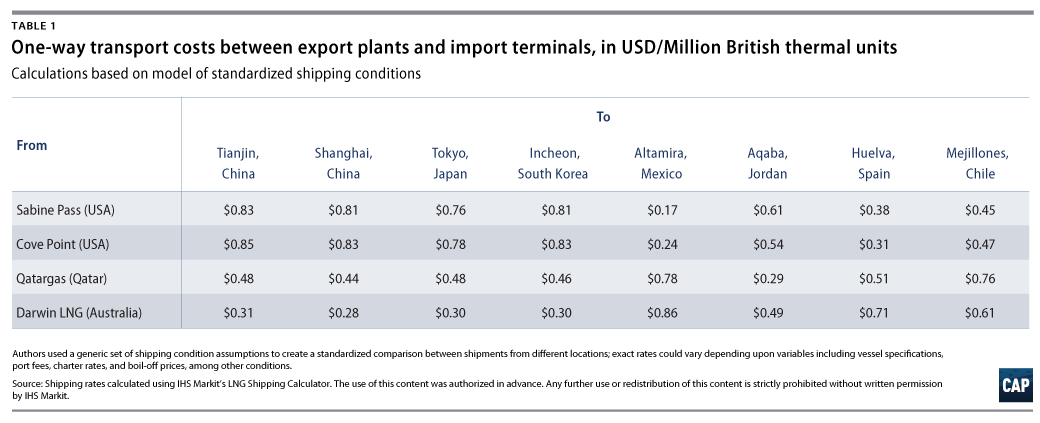

The problem is that, although U.S. production costs are relatively low—U.S. benchmark prices have averaged $3.14 per thousand cubic feet since March 2014 compared with $4.35 per thousand cubic feet in Australia—transport costs from the U.S. Gulf Coast ratchet up the price beyond what China would pay for comparable shipments from Australia. 56 U.S. LNG export infrastructure is clustered along the Gulf Coast because those ports are closest to the nation’s existing pipelines and other onshore natural gas infrastructure.57 Shipping LNG from the U.S. Gulf Coast to China, one way, currently costs approximately twice as much as it does from Qatar and almost three times as much as from Australia. Geographical distance is the problem: When transporting natural gas to Shanghai, tankers from the U.S. Gulf Coast travel 10 days longer than tankers from Qatar and 15 days longer than tankers from Western Australia.58 To reach Asian markets, tankers leaving Gulf Coast terminals must choose among four major maritime routes: Panama Canal, Suez Canal, Cape Horn in South America, or the southern tip of Africa. Even the shortest route from the Gulf Coast to Asia—through the Panama Canal—incurs substantial transit costs.59

In contrast to the challenges involved in sending natural gas to Asia, the United States has a geographical advantage exporting to Canada and Mexico—and that is where the bulk of U.S. exports currently go. Pipeline exports to Canada and Mexico accounted for 78 percent of total U.S. natural gas exports in 2017.60 Excluding continental pipeline trade, Mexico was also the leading export destination for U.S. LNG in 2017.61

Going forward, transport costs are likely to become even more important for U.S. export competitiveness because the capital costs required to bring new U.S. natural gas export terminals online are increasing, and that will make it harder for U.S. exporters to make a profit while also keeping their prices competitive in overseas markets. When the shale gas boom first made it possible for the United States to consider exporting natural gas in the mid-2000s, existing import terminals along the East and Gulf Coasts—which were already connected to the nation’s pipeline network—offered early, limited opportunities for companies to retrofit those facilities for export instead of building new terminals from scratch.62 There are a limited number of existing import terminals available to retrofit, however, so new companies entering the market today are more likely to construct new terminals from scratch. That doubles their upfront capital costs: Constructing a new terminal runs between $31 million and $52 million per billion cubic feet of capacity; retrofitting an existing facility runs $10 million to $12.5 million per billion cubic feet of capacity.63 Across the United States, there are currently 27 active terminal projects: two in operation—Cheniere’s Sabine Pass and, as of March 2018, Dominion Energy Inc.’s Cove Point in Maryland; six terminals or terminal expansions under construction; four approved but not yet under construction; and an additional 16 in the approval or pre-filing stage with relevant regulatory authorities.64 Of those 27 projects, only eight are retrofits.65

If U.S. LNG export tankers departed from the Pacific Coast instead of the Gulf Coast, that would lower maritime transport costs to Asia—thus potentially balancing other costs, such as terminal construction costs—but that is not where most U.S. natural gas production is located. If state and federal regulatory authorities approve the only LNG project currently proposed for the West Coast—the Jordan Cove project in Oregon—that would open up 1.04 billion cubic feet of West Coast export capacity with proximity to Asian markets.66 However, that project is facing substantial opposition from Native American tribes, environmental groups, property owners, and some state leaders along the feeder pipeline’s proposed route.67 Furthermore, adding substantial export capacity along the U.S. Pacific Coast would require sinking even more money into new pipeline infrastructure to connect those terminals to the closest production areas in states such as Wyoming or Colorado.68 Expansions into the U.S. northeast make more commercial sense. The recently operational Cove Point terminal project in Maryland and the Elba Island project under construction in Georgia are located at preexisting import terminal sites with good pipeline connections and geographical proximity to production areas such as the Marcellus and Utica shale plays in Appalachia.69 Once complete, those terminals will provide shorter transport distances to European and Mediterranean markets, but they will not lower transit costs to Asia.70

Overall, exporting LNG from the United States to Asia is an expensive proposition. That can make sense for import markets such as Japan that can pay high prices. Japan, for example, paid an average of $6.13 per thousand cubic feet for the LNG shipments it received from the United States in 2017. In comparison, China paid an average $4.32 per thousand cubic feet,71 and even at that rate, the shipments it received from the United States were among its most expensive, as mentioned above.

It is important to note, however, that China is not the only rapidly growing demand market. As natural gas prices continue to fall and technology innovations offer cheaper and more flexible options for import infrastructure, there has been a rush of new market entrants that—when taken together—outweigh China’s demand growth. Between 2014 and 2017, 12 emerging markets—many of which are leveraging floating infrastructure—cumulatively drove more global LNG demand growth than China. Demand is rising across Europe, the Middle East, and the Americas—all of which are geographically closer to the United States and thus offer more favorable transport rates for U.S. exporters.72 Impressive growth in closer-in markets makes it difficult to justify investing in expensive U.S. projects designed to send LNG to more distant, and thus more costly, East Asian markets where U.S. exports do not enjoy the same comparative advantage.73

If the United States has better export alternatives, why would the White House put so much political capital into pushing for deals with Beijing?

These trends raise an important question about the Trump administration’s China strategy: If the United States has better export alternatives, why would the White House put so much political capital into pushing for deals with Beijing? Furthermore, why would administration officials even consider accepting those deals as a major Chinese trade concession—as Secretary Ross is suggesting—instead of holding the line to demand Chinese action on much bigger trade policy issues?

The Trump administration is pushing investment deals that ignore current market trends

Many of the voices that are bullish on U.S. LNG exports to China are hoping for long-term infrastructure investment deals. With this business model, the buyer agrees to invest in production infrastructure and, in return, gains access to the natural gas the project produces at a set price over 10- to 20-year time horizons. Since prices can shift substantially over a decade and the upfront capital costs are spread out over a long time frame, this approach can make sense even when current price alignments are less than favorable.

In Australia, for example, Chinese investment has been key for developing some of that nation’s recent natural gas infrastructure.74 Australia’s natural gas resources are generally located in sparsely populated regions of the country or offshore, and the pipeline and processing infrastructure needed to link supply and demand would be costly relative to the country’s small population. To address that challenge, Australia actively courted overseas investors—including Chinese corporations—willing to bankroll development projects in exchange for long-term access to the gas those projects produce.

Chinese firms are also acquiring shares in specific Australian gas plays. For example, China National Offshore Oil Corporation (CNOOC) has invested more than US$8 billion in Australian LNG projects, including a 5.3 percent equity stake in Western Australia’s North West Shelf reserves and a 25 percent equity stake in the Queensland Curtis LNG project, which provides CNOOC a guaranteed 175.32 billion cubic feet per annum.75 Similarly, China’s Sinopec owns a 25 percent stake in the Australia Pacific LNG project—also in Queensland—which provides Sinopec a guaranteed 370.12 billion cubic feet per annum.76 In the Surat-Bowen Basin in Queensland, PetroChina, Sinopec, and CNOOC hold 12 percent, 8 percent, and 5 percent shares, respectively, of the basin’s approximately 36.6 trillion cubic feet of proven and probable natural gas reserves.77 Overall, as of 2017, these investments and related contracts—which are public—give China exclusive rights to 20 percent of Australia’s current annual natural gas export capacity of 2.99 trillion cubic feet per annum.78 When nonpublic contracts are included, the total amount is likely much higher.79

Chinese investors are also active in the United States. Since 2010, Chinese companies have invested $12.34 billion in American oil and natural gas companies, approximately $6.3 billion of which is invested in American companies solely working in natural gas.80 Both the United States and Australia have prevented China’s state-owned enterprises from controlling their domestic oil and gas resources: Those firms could make minority-share investments, but they could not control how much gas is pulled out of the ground or where it is sent. In the United States, however, President Donald Trump is aiming to change that arrangement.

When President Trump visited Beijing in November, the two presidents oversaw the signing of a preliminary agreement between Alaska and three Chinese state-owned enterprises—China Petrochemical Corp (Sinopec), China Investment Corp (China’s sovereign wealth fund), and Bank of China—in which the Chinese firms would bankroll Alaskan pipeline infrastructure in exchange for guaranteed access to 75 percent of the gas produced over the duration of the project.81 According to Platts reporting, Alaska’s state gas corporation, Alaska Gasline Development Corporation, “hopes to finalize the Sinopec contract by next December, begin construction in 2019 and to have LNG exports underway by 2024 or 2025.”82 That same trip produced a memorandum of understanding between state-owned China Energy Investment Corporation and West Virginia.83 The West Virginia deal is particularly light on details, but according to West Virginia Gov. Jim Justice (R), the state is hoping that China Energy Investment Corp. will invest around $83 billion in a suite of natural gas projects ranging from power stations to petrochemical plants—more than the state’s gross domestic product for all of 2016.84

In reality, these deals should be viewed with a healthy dose of skepticism, because global markets are shifting in ways that make fixed infrastructure investments of this nature increasingly unattractive. Two big trends are having a particularly important impact: shifts in market pricing and technical innovations in natural gas import and export infrastructure.

On the pricing front, LNG markets are shifting from oil-linked to hub-based pricing, and that is making long-term infrastructure investment contracts less attractive. When trade first began in 1964, there was no standard pricing model for natural gas, so buyers and sellers generally used crude oil prices as a commonly accepted benchmark.85 At that time, long-term contracts were a useful strategy for locking in price security against the volatile price of crude oil.

When the United States began to enter the global market on a large scale, that brought about a new approach to pricing. In the United States, natural gas trade developed primarily to serve domestic use. Since buyers and sellers were operating within the same domestic market, they could negotiate prices based on actual supply and demand rather than a crude oil benchmark.86 The U.S. Henry Hub—the Gulf Coast trading platform where several pipelines intersect—allowed natural gas to compete with natural gas rather than with oil.87 Now other regional markets are following that example and shifting toward hub-based trading, which is making prices more commoditylike and transparent. Buyers can now leverage hub-based trading to take advantage of low-price, short-term, or spot contracts for natural gas rather than relying only on long-term contracts designed to insulate natural gas deals from fluctuations in crude oil.88 Long-term contracts still dominate global LNG trade, but short-term and spot-market contract shipments are rapidly gaining market share: They accounted for 28 percent of global trade volume in 2016, up from 16 percent in 2010. More than half of the spot-market activity is occurring in Asia.89

Technology innovations are yet another force pushing the market away from long-term infrastructure investments. Instead of sinking billions of dollars into fixed import and export terminals—which can quickly become useless if markets shift the wrong way—technical innovations are making it possible to deploy cheaper and more flexible floating units. Floating liquefaction units—otherwise known as floating export terminals—can be constructed using retrofitted tanker ships, new near-shore barges or purpose-built vessels. These units cost $12.5 million to $20.8 million per billion cubic feet of capacity to construct, which is less than half the cost of building a new fixed export terminal in the United States.90 Worldwide, there are already four of these projects under construction—with a total 423 billion cubic feet of capacity—and another 24 in the proposal pipeline, potentially adding another 7.6 trillion cubic feet to the supply side.91

Floating storage and regasification units—import terminals—are also showing up on the demand side of the market. They are less expensive than onshore import facilities by a factor of 4 for new vessels or up to 12.5 for retrofitted LNG tankers.92 New import market entrants—including Colombia, Egypt, Jordan, Pakistan, and the United Arab Emirates—are already utilizing floating terminals. As of January 2017, total floating regasification capacity reached 4 trillion cubic feet across 21 terminals, a significant addition to the demand side.93

As more floating terminals come online, they will have a big impact on the global market. For one thing, they will make expensive fixed export infrastructure investments—such as those under discussion in the United States—an even less attractive proposition. They will also bring in an array of new market entrants. When utilized for export, floating units still rely on proximity to natural gas supply, either via connection to onshore pipelines or offshore reserves; when utilized for import, floating units unlock potentially great demand from a new host of countries in regions closer to U.S. export facilities.94 Nations keen to either buy or sell LNG in relatively small amounts—that is to say, amounts that do not justify sinking billions into fixed infrastructure—can do so more cheaply using floating units. A rush of smaller buyers and sellers can have as big or more of an impact as the movements of one big player such as China. Between 2014 and 2017, 12 countries, taken together, drove more demand growth than China, and floating import terminals enabled three-quarters of that growth.95

These market and technical shifts—combined with unfavorable U.S.-to-China transport rates—explain why, as China’s Vice Minister of Finance Zhu Guangyao put it: “The U.S. is more eager than China to sign long-term LNG contracts.”96 The economics are just not as favorable for China as they used to be, and that is one reason President Trump’s November 2017 Beijing trip only produced vague memorandums rather than binding deals. The West Virginia deal provides almost no detail, and the Alaska deal is basically just a feasibility study.97 It is worth noting that Exxon Mobil, ConocoPhillips, BP Plc, and TransCanada Corp. have already walked away from this same development project in Alaska based on estimates that it would cost up to US$65 billion and take over a decade to construct.98

If private companies are walking away from these infrastructure projects, that raises potential red flags about China’s intentions. One senior Chinese government official interviewed by the authors of this report stated that China’s only reason to sign LNG contracts of this nature with the United States is to win political concessions from President Trump. If Beijing is willing to pay more than $100 billion—the combined costs of the Alaska and West Virginia projects—to get those concessions, the American public will need to know exactly what we are giving China in return.

Even if Beijing’s only intention in potentially bankrolling U.S. infrastructure is to add to their nation’s supply diversification—unlikely, given that China already has 26 suppliers—there are still valid concerns about giving China a controlling stake in U.S. production. Chinese state-owned enterprises, including oil majors, answer to the Chinese Communist Party. Those firms are tools of the state and behave accordingly.99 If those firms obtain massive shares in U.S. natural resources—large enough to potentially control how those resources are used and effectively bankroll the state and local economies in which they operate—that raises important questions about how that might affect U.S. national security.

Alaskan LNG prospects: High costs despite market proximity

The first U.S. LNG exports departed from Kenai, Alaska, in 1969.100 The Kenai terminal exported LNG primarily to Japan. During its heyday from 2000 to 2006, Alaska exported more than 60 billion cubic feet on average per year.101 Starting in the mid-2000s, however, Kenai encountered commercial headwinds. The state has a natural advantage in proximity to Japan and other Asian markets—including open ocean access rather than the necessity of transit through congestion points—but that does not overcome other market disadvantages it faces.

Alaskan natural gas is generally more expensive to develop than lower-48 shale gas due to the costs involved in transporting it to the coast for export. It is also disconnected from lower-48 pipeline networks and thus from the U.S. Henry Hub. Alaskan natural gas is an entirely separate market: Prices are pegged to global oil prices, and it is only profitable when oil prices are higher than $75 per barrel.102 Kenai exports fell to zero in 2013; the last shipments departed the terminal in 2015.103 Kenai simply does not appear to be commercially viable due to the combination of new LNG export terminals coming online in the Gulf Coast, declining global oil prices—particularly in late 2014 and 2015—and a global oversupply of natural gas. Despite receiving approval for non-FTA exports from the U.S. Department of Energy (DOE), ConocoPhilips has sought to sell its Kenai LNG export terminal and announced in July 2017 that it would mothball the facility.104 Based on current market conditions, the proposed $50 billion Alaskan natural gas pipeline and associated export infrastructure may not be commercially feasible.105

Trump administration’s natural gas export obsession risks forfeiting a much bigger game

If individual American companies find good commercial opportunities to export natural gas to China or other buyers, they should go forth—provided, of course, the United States has the regulatory structure in place to make sure those resources are extracted, processed and transported without damaging American health and property.

Problems arise, however, when the White House throws massive political capital into pushing deals that do not make good commercial sense. Those problems are magnified when the federal government does so at the expense of American companies and technologies that do have great commercial potential. Unfortunately, that is exactly what is currently happening on the clean energy front, and the ramifications could significantly undercut U.S. competitiveness over the longer term.

The Trump administration claims that boosting natural gas exports will create new American jobs, but that claim is problematic on multiple fronts. For one thing, the upstream side of the natural gas business—the production side—is becoming increasingly automated, so companies are hiring fewer workers to produce the same amount of gas. In the United States, new drilling technology is reducing labor needs by around 40 percent in the oil and gas business.106 Oil and gas production is shifting toward remote monitoring and management, automation, and data analytics to streamline operations; those shifts improve efficiency but support a much smaller workforce than in years past.107 For example, the World Economic Forum estimates that, industrywide, next-generation automation will displace 38,000 upstream jobs between 2016 and 2025 and the adoption of wireless sensors and other connected devices will displace another 76,000 jobs.108

It is also possible that boosting exports will undermine other sectors of the U.S. economy. If the United States starts sending more natural gas overseas, that may reduce the supply available on the domestic market and drive up prices here at home. U.S. companies who utilize natural gas as a key manufacturing input benefit when domestic U.S. prices are low because that gives them an edge over their competitors in overseas markets. According to one study commissioned by Dow Chemical, natural gas supports eight times more American jobs when it is used for manufacturing instead of export.109 Of course, domestic price increases would also affect American consumers. In 2015, the Center for American Progress analyzed Energy Information Administration data on LNG exports and domestic natural gas prices and found that high levels of LNG exports may lead to $7 billion in additional annual costs to consumers by 2020.110 One could argue that ratcheting up U.S. domestic natural gas prices via exports would make renewable power even more competitive and thus support renewable job growth; however, the Trump administration is disinvesting in renewables and seeking subsidies for coal, a sector that is facing its own job displacement problems due to automation and other market-induced job-loss trends that exceed what is happening in oil and gas.111

Although there is no clear evidence to support claims that boosting natural gas exports will benefit the U.S. economy, it is becoming abundantly clear that clean energy is the real jobs generator. As of 2017, renewable energy is the cheapest source of electricity in the United States.112 Even without taking pollution into account, fossil fuels simply cannot compete with declining renewable energy costs. As renewables become increasingly affordable, that expands use and jobs. At year-end 2016, there were 572,881 renewable electricity generation jobs and 398,235 natural gas-fired electricity generation jobs in the United States.113 In 2017 nearly half of all U.S. utility-scale generation capacity additions came from solar or wind, and the Federal Energy Regulatory Commission expects U.S. renewable generation to more than double over the next three years—despite the fact that the Trump administration is promoting fossil fuels at the expense of other energy sources.114 Globally, the world is already installing more new renewable capacity than fossil fuel capacity, and that gap is steadily expanding.115

This is why Beijing is launching an all-out effort to dominate global clean energy markets. Chinese leaders view clean energy as a key battlefield in the nation’s much broader aim to become the new global high-tech superpower. Power generation and new-energy or energy-efficient vehicles are key focus areas for Beijing’s Made in China 2025 initiative, which is channeling hundreds of billions of dollars in state-funded and state-directed capital to help Chinese companies take over these key technology markets.116 Beijing knows that more than 200 nations are gearing up to invest $13 trillion in renewable energy over the next decade to meet their targets under the Paris climate agreement, and falling renewable energy prices are likely to generate even more investment as more and more nations—even the world’s biggest oil producers—transition to renewables.117 Chinese leaders want the bulk of those technologies and products to come from China. They expect this global renewable push to generate 13 million new Chinese jobs by 2020, and they are pulling every policy lever they can reach to make that happen.118

Unfortunately, at the very moment when the United States should be gearing up to face Chinese competition in the energy technology sectors of the future, the Trump administration is undercutting U.S. clean tech innovation on multiple fronts.119 Trump’s budget proposals openly attack investment in clean energy and energy efficiency technologies: Across the DOE, clean energy research and development faced proposed cuts up to 70 percent in fiscal year 2018 and up to 66 percent in fiscal year 2019.120 These cuts undermine not only the integrity of the individual offices focused on researching and developing efficiency, solar, wind, carbon capture, grid, and nuclear technologies but also the national laboratories that support that work. Each budget proposal has also called for the termination of vital research, development, and commercialization programs such as the DOE’s Advanced Research Projects Agency-Energy (ARPA-E) and Loan Programs.121 Furthermore, by terminating the Clean Power Plan, the Trump administration has removed carbon pollution standards for power plants that would have increased the amount of renewable energy and efficiency technologies in use in the United States.122 Secretary of the Department of Energy Rick Perry also proposed a rule to the Federal Energy Regulatory Commission that would have subsidized coal and nuclear power plants had it not been rejected by the commissioners.123

When Trump administration officials frame natural gas exports as a major demand in U.S.-China trade talks that risks undercutting the U.S. economy even further. Beijing is deploying an array of nationalist economic policies—including the Made in China 2025 initiative—that leverage state resources to help Chinese companies push American competitors out of global high-tech markets. The Trump administration recently threatened to retaliate by levying tariffs against $50 billion in Chinese imports. The tariff approach is problematic on multiple fronts—it will likely hit U.S. consumers as hard if not harder than China—but the Trump administration will wade into truly dangerous waters if it first threatens China with tariffs and then offers to reduce them if China buys more LNG from the United States. When the administration announced the new tariffs, U.S. Commerce Secretary Wilbur Ross stated that “we will end up negotiating these things rather than fighting over them.”124 According to Secretary Ross, President Trump has asked President Xi for a $100 billion reduction in the U.S. trade deficit, which, according to Secretary Ross, China can partially fulfill by shifting its natural gas supply chain from other nations to the United States. In addition to the fact that—as outlined above—that does not make good commercial sense for either nation, if the administration accepts LNG deals as a major trade concession that will give Beijing a pass on much bigger trade issues that, if not adequately addressed, will undermine U.S. competitiveness for decades to come.

Conclusion

Natural gas consumption is rising in China. That is a good thing for China’s energy transition and emission-reduction efforts. If individual American firms find commercial opportunities to provide some of that natural gas, they should go forth. At a national level, however, the U.S. federal government should not push export deals that do not make good commercial sense and risk undermining broader U.S. competitiveness vis-a-vis China.

Unfortunately, that is exactly what the Trump administration is currently doing. As Beijing is well aware, clean energy is the real battleground, and while China is doing everything it can to help its own companies dominate that rapidly growing global market, the Trump administration is undercutting U.S. clean-tech innovation and wasting federal government political capital pushing for natural gas deals that the United States does not actually need. If the administration takes this a step further—as Secretary Ross is recommending—by accepting U.S.-China natural gas deals in exchange for backing off on much broader U.S. trade concerns with China, that will further undercut the U.S. economy and play right into Beijing’s hands.

About the authors

Melanie Hart is a senior fellow and the director for China Policy at the Center for American Progress.

Luke H. Bassett is the associate director for Domestic Energy Policy at the Center.

Blaine Johnson is the policy analyst for China and Asia Policy at the Center.

Appendix A: U.S. LNG export shipments to China as of year-end 2017

For a table of U.S. LNG shipments to China as of year-end 2017, see the PDF.

Appendix B: China’s natural gas reform timeline

Leveraging incremental liberalization to increase production and consumption growth

January 2013—12th Five-Year Plan for Energy Development (2010-2015), State Council:125 Sets new natural gas production and consumption targets for 2015, including: increasing the share of natural gas in the nation’s energy mix from 5.3 percent at year-end 2010 to 7.5 percent by 2015; increasing natural gas production capacity 10.5 percent annually through 2015; increasing natural gas-fired electricity generation capacity 16.2 percent annually through 2015; and increasing the number of residential natural gas users by 6.8 percent annually to reach 250 million total users by 2015.

June 2013—Notice Adjusting Natural Gas Prices, National Development and Reform Commission:126 Implements a net-back pricing model that pegs domestic city-gate rates to the market rates for fuel oil and liquid petroleum gas. Fuel oil accounts for 60 percent of the new price-guiding basket and liquid petroleum gas for 40 percent. Divides natural gas consumption into two buckets defined by volume: base and incremental. Rate increases for base gas—volumes equal to or less than 2012 consumption—are capped at 400 Chinese yuan per thousand cubic meters. Rates for incremental gas—for volumes exceeding 2012 consumption levels—follow the new pricing scheme. Grants special rate exemptions to the chemical fertilizer industry and residential users. The price increase for fertilizer industry purchases is capped at 250 Chinese yuan per thousand cubic meters, and local governments can provide additional financial relief if needed. Prices remain unchanged for all existing residential natural gas consumers; new users will pay the new city-gate rate for base gas. Liberalizes ex-factory prices for imported liquefied natural gas (LNG) and unconventional gas—including shale gas, coal-bed methane, and coal-based liquefied gas—except in cases where such gas is mixed with other sources in long-distance transmission pipelines, in which case city-gate rates apply to the mix.

September 2013—Air Pollution Prevention Action Plan, State Council:127 Orders major urban areas along China’s eastern seaboard to reduce coal consumption; close down coal-fired industrial boilers and power plants; and bring in natural gas and renewables as substitutes to meet new 2017 air pollution reduction and control targets. Calls for expanded natural gas pipeline capacity. Directs relevant ministries, agencies, and subnational governments to give residential users and coal-replacement projects priority access to new natural gas infrastructure and supplies.

February 2014—Trial Supervision Measures for the Fair and Open Access to Oil and Gas Pipeline Networks, National Energy Administration:128 Orders state-owned oil and gas pipeline operators with surplus capacity to provide pipeline access and services—including transport, storage, gasification, liquefaction, and compression—to third-party entities in a fair and nondiscriminatory manner according to the order in which contracts are signed. The National Energy Administration will supervise the opening of oil and gas pipeline network facilities and will establish regulations on information disclosure and other issues relating to fair access.

February 2014—Natural Gas Infrastructure Construction and Operation Management Measures, National Development and Reform Commission:129 Encourages both state-owned and private companies to invest in, construct, and integrate national gas infrastructure. Orders those activities to comply with relevant development plans—such as the national natural gas infrastructure development plan and the national main functional area plan—and to fit market supply and demand conditions. Imposes new information transparency requirements: Companies that own and operate natural gas infrastructure must publish their capacity and services available to third-party users as well as the conditions and procedures for third-party access. Orders infrastructure operators to provide third-party access in a fair and equitable manner.

March 2014—Guiding Opinion on Establishing and Improving the Progressive Pricing Mechanism of Natural Gas for Residential Consumption, National Development and Reform Commission:130 Launches a new three-tier pricing mechanism for residential natural gas that bases residential rates on household consumption levels. Gives local governments the flexibility to determine whether to assess household consumption on a monthly, seasonal, or annual basis. Based on that assessment, high-volume users will be placed in a high-rate bucket, mid-volume users in a mid-rate bucket, and low-volume users in a low-rate bucket. Cities with existing natural gas connections are to roll out this new system by the end of 2015.

August 2014—Notice Adjusting the Price of Nonresidential Base Natural Gas Use, National Development and Reform Commission:131 Further liberalizes pricing for imported liquefied natural gas and unconventional gas including shale gas, coal-bed methane, and coal-based liquefied gas. Where such gas is mixed with other sources—such as domestic or imported conventional gas—prices for the entire mix can be negotiated according to supply and demand. Raises city-gate ceiling prices for base-use conventional natural gas. Exempts the chemical fertilizer industry from these price reforms until the fertilizer market improves.

June 2014—Energy Development Strategic Action Plan for 2014-2020, State Council:132 Signals that Beijing is significantly increasing its focus on the nation’s natural gas development. Calls for natural gas to account for at least 10 percent of the nation’s primary energy mix by 2020. Orders vigorous production development on all fronts: onshore and offshore; conventional and unconventional. Orders producers to develop eight large-scale natural gas production bases with annual outputs of more than 10 billion cubic meters. Calls for producers to increase the nation’s conventional proven natural gas reserves to a cumulative 5.5 trillion cubic meters and reach a total annual output of 185 billion cubic meters by 2020, which would amount to an annual production growth rate of more than 6 percent. Encourages import expansion and calls for new demand-side measures including support for natural gas vehicles and ships.

February 2015—Notice on Rationalizing the Price of Nonresidential Natural Gas, National Development and Reform Commission:133 Decreases the incremental rate by 440 Chinese yuan per thousand cubic meters and increases the base rate by 40 Chinese yuan per thousand cubic meters to create one unified natural gas rate for each province or municipality. Officially removes the prior pricing distinction between base and incremental gas. Implements pilot marketization for natural gas consumers—not including the chemical fertilizer industry—who purchase directly from producers. Those direct purchase rates can be negotiated based on supply and demand.

November 2015—Notice on Reducing the City-Gate Price of Natural Gas for Nonresidential Use and Further Promoting Market-Oriented Price Reform, National Development and Reform Commission:134 Reduces nonresidential city-gate gas rates by 700 Chinese yuan per thousand cubic meters. Switches the price management regime from ceiling to benchmark, meaning prices can be negotiated below the benchmark and up to 20 percent above it. Exempts the chemical fertilizer industry from these changes.

October 2016—Trial Natural Gas Pipeline Transportation Price Management Measures, National Development and Reform Commission:135 Sets principles for pipeline transportation price management based on permissible cost, reasonable return, transparency, and ease of operation. Orders pipeline operators to separate their pipeline transportation business from other business units and implement independent financial accounting. Defines a standard for annual allowable pipeline transportation revenue based on “permitted cost plus reasonable return.”

October 2016—Trial Natural Gas Pipeline Transportation Pricing Cost Supervision and Auditing Measures, National Development and Reform Commission:136 Establishes new guidelines for pipeline transport cost supervision. Pipeline operators must set up an independent cost accounting system for gas transmission services; the State Council Pricing Department is responsible for organizing the implementation of pipeline transportation pricing supervision and inspection work.

November 2016—Notice Promoting Marketization Reform of Chemical Fertilizer Gas Use Prices, National Development and Reform Commission:137 Fully liberalizes pricing for natural gas sales to chemical fertilizer producers. Prices are to be negotiated between producer and consumer based on supply and demand.

December 2016—13th Five-Year Plan for Natural Gas Development, National Development and Reform Commission:138 Sets new targets and calls for vigorous market development across all fronts. By 2020, annual production must reach 207 billion cubic meters per year, including 120 billion cubic meters of conventional gas; 37 billion cubic meters of tight gas; 10 billion cubic meters of offshore gas; 30 billion cubic meters of shale gas; and 10 billion cubic meters of coal bed methane per year. Calls for national pipeline infrastructure to reach 104,000 kilometers by 2020—with a total capacity of 400 billion cubic meters—and underground natural gas storage capacity to reach 14.8 billion cubic meters by 2020. Calls for LNG import infrastructure projects to prioritize large demand centers in the Bohai Rim, Yangtze River Delta, and southeastern coastal areas. Promotes LNG fuel for transport use and sets multiple 2020 transport targets including: reaching a total of 10 million LNG vehicles, 12,000 gas stations, and more than 200 docking stations for ships. Calls for specific natural gas infrastructure expansions designed to support coal-to-gas switching such as small-scale LNG storage tanks in rural areas. Calls for multiple policy incentives to support natural gas supply and demand development projects, including preferential tax policies to support natural gas production and new market-based procedures for transferring exploration and development rights.

June 2017—Opinions on the Acceleration of Natural Gas Use, National Development and Reform Commission, Ministry of Science and Technology, Ministry of Industry and Information Technology, Ministry of Finance, and Others:139 Sets 2030 natural gas targets. Calls for natural gas to account for 15 percent of China’s energy mix by 2030 and for China to expand underground natural gas storage capacity to 35 billion cubic meters by 2030. The 2020 targets are 10 percent of the energy mix and 14.8 billion cubic meters of storage capacity. Outlines a cross-ministerial effort for meeting China’s natural gas development goals, with a particular focus on addressing persistent market bottlenecks. Calls for new engineering and development projects to support natural gas use for winter heating, gas-fired electricity, industrial use, and expanded consumer access to natural gas filling and docking stations. Calls for additional environmental regulatory tightening to incentivize increased natural gas use, particularly coal-to-gas switching. Calls for additional progress toward national gas market liberalization and additional financial support to incentivize production and consumption growth.

August 2017—Notice Reducing the Nonresidential Natural Gas Reference City-Gate Prices, National Development and Reform Commission:140 Lowers the baseline city-gate natural gas rate by 100 Chinese yuan per thousand cubic meters. States that city-gate prices will be progressively reduced going forward and open trading will be promoted.

December 2017—Letter Requesting Good Work on Integrated Coal Management to Ensure the People Stay Warm Through the Winter, Ministry of Environmental Protection Department of Air Environment Management:141 Permits localities to continue using previous coal-fired heating methods—which were to be phased out by year-end 2017—and other alternative heating methods on an interim basis to prevent heating shortages where required coal phaseouts are not yet complete. Orders local officials to give residential natural gas users priority over industrial users and gas-fired power stations when shortages emerge. Warns officials that the Ministry of Environmental Protection will monitor winter heating conditions and hold localities accountable for disorderly pollution management work.

December 2017—Notice Regarding the Issuance of a 2017–2021 Winter Clean Heating Plan for Northern Regions, National Development and Reform Commission, National Energy Administration, Ministry of Finance, Ministry of Environmental Protection, and Other Relevant Agencies:142 Orders northern regions to fill winter heating gaps—from the phase-out of small coal boilers—with a range of clean-heating sources to avoid triggering seasonal natural gas supply shortages. The northern region targeted by this plan includes Beijing, Tianjin, Hebei, Shanxi, Inner Mongolia, Liaoning, Jilin, Heilongjiang, Shandong, Shaanxi, Gansu, Ningxia, Xinjiang, Qinghai, and portions of Henan. This region also covers the “2+26” key cities of the Beijing-Tianjin-Hebei air pollution transmission channel, including Xiong’an New District. States that, as of 2016, 83 percent of floorspace in China’s northern regions is served by coal-fired heating and 17 percent by a mix of alternative heating sources, including natural gas-fired heating—which accounts for 11 percent total—electric power, geothermal, biomass, solar, and industrial waste heat. States that 34 percent of the total heat generation can be considered “clean” heating—including clean coal—as of 2016. Sets a new target to expand clean heating to cover 70 percent of the region’s total heated floor space by 2021. Northern regions are to meet that target by bringing new clean heating sources online to replace 150 million tons of dispersed coal, including low-efficiency small boiler coal use. Total clean-heating capacity targets for 2021 include: expanding biomass heating capacity to cover 2.1 billion square meters; expanding electric heating capacity to cover 1.5 billion square meters; expanding geothermal heating capacity to cover 1 billion cubic meters; expanding waste industrial heat to cover 200 million square meters; and expanding solar heating to cover 50 million square meters. The plan puts particular emphasis on clean coal heating, targeting the construction of 10 gigawatts of new back pressure combined heat and power units and retrofitting 120 gigawatts of existing units to reach 11 billion square meters of clean coal heating capacity. The “2+26” key cities are prioritized for new construction of natural gas heating: Between 2017 and 2021, new construction of natural gas heating capacity in these key cities should cover an additional 180,000 square meters. This plan also includes an annex, “General plan for winter coal-to-gas source protection for clean heating in key northern regions,” which formulates a safeguard plan for the six provinces/municipalities of the “2+26” key cities of the Beijing-Tianjin-Hebei air pollution transmission channel and orders the other northern region provinces to create their own natural gas resource guarantee policies for the “coal-to-gas” clean heating program based on this plan. This annex includes targets for the natural gas volume supplied by China’s three oil majors to the abovementioned six provinces/municipalities during 2021, in addition to targets for the construction of new natural gas storage capacity, LNG receiving station capacity, gasification output capacity (from 82 million cubic meters per day in 2017 to 165 million cubic meters per day by 2021), and pipelines.