Introduction and summary

“Where different groups of people live and the homes in which they live are not simply neutral or random demographic phenomena. They profoundly influence the allocation of rewards in the United States.”

– Gregory Squires, 20071

Last year marked the 50th anniversary of the release of the Kerner Report2 and the passage of the Fair Housing Act. Spurred by race-related unrest that broke out in more than 100 U.S. cities between 1965 and 1968, the Kerner Report denounced the structural barriers to economic equality afflicting black communities in the United States.3 The report pointed to the role of white racism and the pervasive discrimination against and segregation of African Americans in housing, employment, and education in the creation and perpetuation of two societies: “one black, one white—separate and unequal.”4 The Fair Housing Act, which was passed in April 1968 as Title VIII of the Civil Rights Act, was meant to eliminate overt discrimination and disparities in the housing market and ultimately end residential segregation. Specifically, it prohibited discrimination in the sale or rental of housing; the financing of housing; and the provision of brokerage services based on a person’s inclusion in a protected class, including race, color, and national origin.5

Despite the economic and political gains that African Americans have achieved since the passage of the Civil Rights Act, significant disparities still exist between African Americans and non-Hispanic whites in terms of access to homeownership, quality education, and employment, among other assets. These disparities are reflected in persisting residential segregation and a racially segmented housing market—and they have significant implications for African Americans’ economic mobility. Segregation, disparate access to credit and homeownership, and the consistent devaluation of homes in black neighborhoods6 combine to constrict the ability of African Americans to build equity and accumulate wealth through homeownership.

This report focuses on the residential patterns of black and non-Hispanic white home mortgage borrowers and the racial disparities in home appreciation in neighborhoods where these borrowers purchase their homes. Throughout the report, the author uses the terms “African American” and “black” as well as “non-Hispanic white” and “white” interchangeably. The neighborhoods where homebuyers purchase their homes contribute to their home’s worth and its chance of appreciating over time, which has important implications for the long-term financial returns associated with homeownership. Before presenting original analysis of home mortgage lending to black and white homebuyers prior to and after the 2008 financial crisis, this report discusses the government policies and other factors that have led to and continue to contribute to persisting African American segregation. The report also provides an overview of the Fair Housing Act in addressing housing discrimination and segregation. Despite some progress in achieving integration, weaknesses in fair housing enforcement have undermined the ability of the Fair Housing Act to dismantle segregation and combat discrimination. The forms of discrimination that were common in the past have been shifting over time, and housing discrimination—along with persisting residential segregation—continue to hamper African American homebuyers’ ability to build equity. African American home mortgage borrowers remain concentrated in residentially segregated areas where homes have failed to appreciate at the same pace as those in neighborhoods where white borrowers more predominantly buy their homes.

The report concludes with recommendations on how to strengthen fair housing enforcement, even as the Trump administration is rolling back fair housing policies and integration remedies. The recommendations include:

- Make local jurisdictions once again responsible for planning to achieve fair housing. In particular, the Affirmatively Furthering Fair Housing (AFFH) rule should be fully reinstated.

- Empower federal, state, and local governments and nonprofits to fully enforce the Fair Housing Act. More funding should be appropriated for the Fair Housing Initiatives Program (FHIP) and for staffing in the U.S. Department of Housing and Urban Development’s (HUD) Office of Fair Housing and Equal Opportunity (FHEO).

- Catch and stop systematic discrimination, rather than perpetuating it. Specifically, it is essential that HUD firmly enforce—rather than reconsider and dilute—the Fair Housing Act’s disparate impact rule.

Residential segregation is not a coincidence

Despite a steady decline since the peak levels of the 1960s and 1970s, residential segregation still persists in U.S. metropolitan areas, and African Americans continue to experience the highest segregation levels among all racial and ethnic groups.7 Empirical studies show that today, the typical African American resides in a neighborhood that is only 35 percent white. That is not any better than what was common in 1940, when the average black resident lived in a census tract where non-Hispanic white residents represented 40 percent of the total population.8

The patterns of residential segregation observed today have not emerged by chance. As Richard Rothstein wrote in his book, The Color of Law: A Forgotten History of How Our Government Segregated America, “the public policies of yesterday still shape the racial landscape of today.”9 This is particularly true in the housing realm, as legal forms of discrimination and racially biased federal government policies have played a critical role in the creation and endurance of segregated African American neighborhoods during a significant portion of the 20th century.10 In particular, a two-tier approach to housing policies that emerged as a response to the Great Depression functioned largely in favor of white middle-class families, while intentionally harming people of color.11 On the one side, the federal government sought to stabilize financial conditions for homeownership by establishing the Home Owners’ Loan Corporation (HOLC), the Federal Housing Administration (FHA), and the secondary mortgage market. The introduction of publicly backed, low down payment, fully amortizing, long-term, fixed-rate home mortgage loans promoted the demand for housing and boosted the construction and lending industries. On the other side, the establishment of the Public Works Administration (PWA) Housing Division programs sponsored public housing construction and slum clearance to improve the housing conditions of low-income families and boost employment in the building trades.

But this two-tier approach to housing policy promoted residential segregation in important ways. The federal government’s support for homeownership systematically targeted white borrowers and excluded African Americans and other people of color. The HOLC, in particular, institutionalized redlining as a way to evaluate the quality of neighborhoods based on their racial and ethnic makeup. Neighborhoods with a large population of African Americans and other people of color typically received the lowest ratings and were deemed too risky to secure government-backed mortgages.12 Investment money was consistently deflected away from central cities where people of color were concentrated.13 At the same time, slum-clearance projects displaced minority residents and typically forced them to relocate deeper into the slums, because most government-sponsored housing units were unaffordable for very low-income families of color, and restrictive covenants prevented them from moving to integrated neighborhoods.14 In addition, the PWA program established specific rules for housing unit allocation. In particular, the Neighborhood Composition Rule required housing projects not to alter the racial character of their surrounding neighborhoods.15

The segregative patterns thus institutionalized were reinforced by the Housing Act of 1937, which introduced the enactment of the first major public housing program . Local housing authorities had discretionary control over where they would develop public housing projects and who those projects would target. This early public housing effort received intense public opposition, especially from the National Association of Real Estate Boards.16

As a concession to opponents of public housing, the so-called equivalent elimination rule contained in the 1937 Housing Act required housing authorities to eliminate a substandard dwelling unit for each new unit of public housing built. In order to not interfere with the private housing market, public housing was not to increase the overall supply of housing. As a result, public housing projects were built predominantly in inner-city locations to replace preexisting slums and thus helped contain African American and other minority neighborhoods.17

The two-tier approach to housing policy was consolidated in the postwar years, when the demand for new housing prompted the federal government to buttress existing programs and design new ones. These programs played a key role in the solidification of racially segregated neighborhoods.18 The FHA and the Veterans Administration loan programs adopted the HOLC rating system. These programs denied credit to inner-city communities of color, served predominantly white buyers, and spurred white flight and suburbanization.19 The FHA “Underwriting Manual,”20 in particular, provided specific guidelines for the evaluation of properties and neighborhoods in a way that would reinforce racial segregation.21 Federal Housing Administration, “Underwriting Manual.”] White flight was also supported by massive federal investment in highway construction, which was often deliberately planned to create racial barriers between white neighborhoods and areas featuring a large presence of African Americans and other racial and ethnic minorities.22 At the same time, the 1949 Housing Act limited public housing to the very low income, and public housing projects became a permanent housing solution for very low-income people of color, who were increasingly separated from mainstream society.23 The urban renewal program, introduced in 1954 as an amendment to the 1949 Housing Act, was intended to attack blight, stimulate downtown investment, and promote highway construction. As a result of the program, however, entire black neighborhoods in close proximity to key white neighborhoods and institutions—such as newly planned universities and hospital complexes—were bulldozed, and massive public housing projects were built in order to contain displaced black residents.24

The Fair Housing Act at 50

The Fair Housing Act of 1968 was the first open-house legislation designed to right the wrongs of the racially biased laws and policies that had purposefully created segregated communities across the United States. Specifically, the law prohibited housing discrimination in public and private housing transactions. The law also required the federal government to administer all federal housing and community development programs in a manner that would affirmatively further the fair housing purposes of the act.25 As a condition of receiving HUD-administered funds, program participants were required to take active steps to undo historic patterns of segregation.26 Among the discriminatory housing practices that the Fair Housing Act outlawed were refusing outright to rent or sell; refusing to negotiate; deceptively denying the availability of housing; refusing to make home mortgage loans; providing limited advertisements; and coercing, intimidating, and threatening based on membership in a protected class.27 The law gave the secretary of HUD the statutory authority to enforce the nondiscrimination provisions of the act and required the secretary to ensure compliance with the Fair Housing Act’s AFFH mandate. In addition, the law provided for enforcement actions brought by the U.S. Department of Justice (DOJ) and for private causes of actions in federal court to individual victims of housing discrimination.28

The law was passed at a time of significant turmoil, as cities around the nation were experiencing a wave of race-related unrest due to longstanding discrimination against African Americans. President Lyndon Johnson had already attempted to introduce fair housing legislation in 1966. President Johnson’s early proposal for the universal ban of discrimination in the sale and rental of housing, however, was met with significant opposition by the National Association of Real Estate Brokers and was prevented by a Senate filibuster.29 It was not until the release of the Kerner Report and the assassination of Dr. Martin Luther King Jr. that the first fair housing legislation was enacted. The Fair Housing Act was quickly pulled together behind closed doors following King’s assassination, without any Senate hearings, markups, scrupulous debate, or the documentation of congressional intent necessary to guide future courts and litigants.

Rushed negotiations and significant compromise largely shaped the final statute. The Fair Housing Act’s coverage was originally limited to race, color, religion, and national origin. It also included an exemption according to which a dwelling was not covered by the statute if it had fewer than five rental units and its owner lived in one of them. Most importantly, the legislation lacked critical enforcement provisions. Civil penalties were missing, and HUD did not have any cease and desist powers to temporarily hold a housing unit off the market during a conciliation process.30 During the first 20 years after the passage of the act, HUD and the DOJ did not have the ability to forcibly seek relief for individual victims of housing discrimination,31 in part because they lacked political support, staff, and resources.

To address the inadequacy of the statute’s enforcement provision, Congress amended the Fair Housing Act in 1988. The amendments added two new protected classes—disability and familial status—created a new administrative complaint process, and enhanced the penalties that came with violating the Fair Housing Act. In addition, HUD authorized state and local human rights commissions with “substantially equivalent” fair housing laws to perform conciliations.32

Two major developments in the Fair Housing Act were introduced during former President Barack Obama’s tenure. In 2013, HUD published a final rule, entitled “Implementation of the Fair Housing Act’s Discriminatory Effects Standard,” under which practices with an unjustified discriminatory effect, including those without a discriminatory intent, are deemed liable.33 Under the legal doctrine of disparate impact, actions can be considered discriminatory if they have a disparate effect on protected classes even if that was not the intent of those actions. In 2015, the U.S. Supreme Court, in Texas Department of Housing and Community Affairs v. Inclusive Communities Project Inc., ruled that claims of disparate impact are cognizable under the Fair Housing Act.34 Furthermore, in 2015 the Obama administration introduced a AFFH rule that strengthened the AFFH mandate of the Fair Housing Act and made it enforceable.35 Over the years, due to the lack of clear implementation and enforcement guidance, many recipients of HUD funds failed to meet the existing AFFH obligation. The 2015 AFFH rule provided HUD program participants with a tool for analyzing local and regional fair housing issues and identifying patterns of segregation and access to opportunity.

Despite some progress, residential segregation and housing discrimination persist

Some progress in achieving integration and combating discrimination has been made since the passage of the Federal Housing Act. For example, there is greater black-white integration today compared with in 1968.36 Up until the late 1960s, high levels of residential segregation were widespread across U.S. metropolitan areas. Douglas S. Massey and Jonathan Tannen indicate that in 1970, immediately following the passage of the Fair Housing Act, nearly half of the black population in the United States resided in 1 of 40 hypersegregated metropolitan areas.37 Hypersegregation—a notion developed in 1989 by Massey and Nancy A. Denton38—occurs when a racial or ethnic group is highly segregated on at least 4 of 5 dimensions of segregation, including unevenness, isolation, clustering, concentration, and centralization.39 The number of hypersegregated areas dropped to 21 by 2010. Average segregation in these areas, however, had fallen only modestly, and hypersegregation is still common in metropolitan areas that feature some of the United States’ largest African American communities. These include Baltimore and Chicago, among other cities.40

The root causes of residential segregation have been and continue to be widely explored and debated in scholarly studies. Some argue that residential segregation is the result of nonracial demographic and socioeconomic circumstances, whereas others attribute the separation of racial groups in the residential landscape to racist attitudes and practices such as prejudice and discrimination in the housing market. A comprehensive summary and critique of recent evidence on the causes of black-white residential segregation concludes that although racial prejudice and racial differences in homebuyers’ income, taste, and housing information play a role in the perpetuation of residential segregation, these factors contribute to just a small portion of the observed segregative residential patterns that are still visible across the United States.41 Recent evidence provides more convincing support for a fifth hypothesis, according to which discrimination in the housing market continues to drive black-white segregation and reinforces a vicious structural cycle that puts black homebuyers at a clear disadvantage compared with similarly situated white homebuyers.42

There is little doubt that the legal challenges brought to discriminatory housing practices have resulted in greater compliance with the law, especially since the Fair Housing Act’s amendments of the late 1980s.43 Prior to the Federal Housing Act of 1968, it was legal for real estate agents to deny African Americans and other people of color access to rental units and homeownership because of their race. As a series of national housing discrimination studies that the Urban Institute conducted for HUD indicate, the most overt forms of housing discrimination have declined over the course of the past few decades.44 However, evidence shows that racial discrimination in the housing market still exists and, as Massey cautions, racial discrimination is a moving target,45 as the forms of discrimination that were common in the past have been shifting over time.

New forms of racial bias in housing have thus emerged. Racial steering, for instance, has become more common. Under this practice, real estate agents deliberately steer African Americans away from desirable neighborhoods and toward areas featuring larger concentrations of people of color, higher poverty levels, and lower housing quality compared with neighborhoods to where whites relocate.46 The Urban Institute’s 2012 audit study proves that minority homebuyers are consistently offered fewer residential options than white homebuyers. 47 In particular, real estate agents tend to favor white homebuyers by providing information on and showing more available homes than in the case of equally qualified black homebuyers. In addition, black homebuyers are 2.4 percent more likely than equally qualified white homebuyers to be denied an in-person appointment. Furthermore, the neighborhoods where white homebuyers are recommended and shown homes tend to be characterized by a larger presence of white residents than the neighborhoods where black homebuyers are recommended and shown homes. The 2012 HUD study indicates that “whites hear more positive comments about white neighborhoods and more negative comments about minority neighborhoods than do blacks, potentially steering them away from mixed or minority neighborhoods.”48 Recent investigations and litigation cases indicate that housing industry agents—realtors, landlords, and brokers—who intend to violate fair housing laws have become more skillful in disguising their discriminatory behavior in order not to be detected.49 Housing providers often do not advertise available units. In particular, with the proliferation of social media and online housing advertising, discriminatory digital marketing has become more common.50 After a 2016 ProPublica investigation51 revealed Facebook’s practice of allowing its advertisers to exclude Facebook users from seeing housing ads based on their race and ethnicity, the National Fair Housing Alliance and other civil rights advocates took legal action against the company. As a result of the litigation, in March 2019, Facebook agreed to stop allowing landlords, creditors, and employers, among other advertisers, to discriminate against people of color and other protected classes.52 During the same month, HUD also filed charges against Facebook for violating fair housing laws.53

The forms of discrimination against home mortgage applicants that were prevalent before the Equal Credit Opportunity Act of 1974 and the Community Reinvestment Act of 1977 have similarly diminished but have not disappeared, shifting from the outright denial of mortgages to potential borrowers of color to predatory practices, subprime lending, and unfavorable loan terms.54 Racial discrimination is often present at various stages of the home sales and mortgage lending processes,55 and home mortgage lending discrimination often materializes in algorithmic scoring. Recent evidence shows that financial technology lenders typically charge borrowers of color eight basis points higher interest rates than they charge white borrowers.56 In addition, in the wake of the financial crisis, redlining has reemerged as a common—although less overt than in the past—form of discrimination among lenders that have pulled back from minority neighborhoods by placing branches, brokers, and mortgage services outside these communities.57

Segregation continues to harm the ability of African American homebuyers to build equity

Discrimination in the housing market reinforces the patterns of residential segregation that have been largely shaped by decades of racially biased housing policies. Most importantly, housing discrimination and residential segregation hamper the ability of African American homebuyers to build equity. Homes in primarily African American neighborhoods typically feature more volatile demand and prices than those in predominantly white areas, where resources such as access to well-paying jobs and quality schools are concentrated and contribute to higher housing demand and prices.58 In contrast, past and present racial biases and discriminatory practices in real estate markets59—such as redlining,60 steering,61 variations in appraisal methods, and appraisers’ racialized perceptions of neighborhoods,62 among others—contribute to a lower housing demand in African American neighborhoods.63 A low housing demand in these neighborhoods depresses their home prices. Research shows that, even after taking housing characteristics into consideration, homes in neighborhoods where there is a large concentration of African Americans as well as neighborhoods that are racially transitioning typically are worth less and appreciate at a lower rate than those in predominantly white neighborhoods.64 A new study by the Brookings Institution indicates that in neighborhoods where African Americans represent the majority of the population, homes are valued at about half the price of homes in neighborhoods where there are no African American residents.65 The devaluation of African American-owned homes is particularly evident in previously redlined neighborhoods.66 Further, since the peak of the housing boom, neighborhoods with a large African American population have depreciated more and have been less likely to recover than predominantly white neighborhoods.67 Between 2003 and 2009—that is, during the housing boom and the subsequent foreclosure crisis—black homeowners who remained in their homes accrued less home equity than white homeowners and were more likely to end the period with negative equity.68

As homebuyers tend to look for housing options in communities where they anticipate greater capital gains, discrimination and low housing appreciation disproportionately harm largely black neighborhoods.69 Meanwhile, due to decades of racially biased policies and practices in U.S. real estate and labor markets and a limited access to credit, African Americans continue to lag behind white people in the homeownership market.70 Not only are African Americans receiving proportionally fewer home mortgage loans, obtaining more costly and riskier loans, and less likely to own their homes than white people,71 but they are also constrained in their residential options and continue buying in predominantly African American neighborhoods where they have fewer chances than similarly situated white homebuyers to acquire assets that appreciate quickly.

This vicious cycle puts African Americans at a disadvantage in their ability to build equity and accumulate wealth.72 For black homeowners, home equity represents a greater part of their net worth than it does for white homeowners. Center for American Progress analysis of Federal Reserve data indicates that primary residences account for 58 percent of African Americans’ net worth, compared with 40 percent of whites’ wealth portfolio, which is more diversified than that of nonwhite households.73 Yet, in 2016, the mean net housing wealth of white homeowners was $215,800, compared with only $94,400 among black homeowners.74

African Americans continue to buy homes in predominantly nonwhite neighborhoods

Mortgage data show that while lending to African American borrowers has continued to expand after the housing crash of 2007, harmful segregation patterns persist.75 Specifically, in postrecession years, African American and non-Hispanic white home mortgage borrowers have continued buying properties in separate neighborhoods.

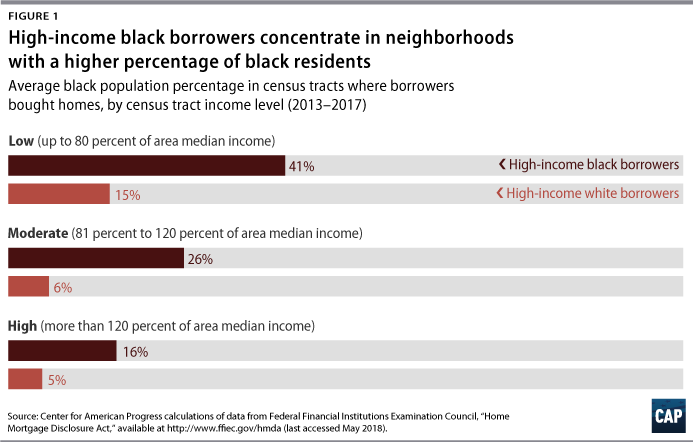

Similar to prerecession years, African American borrowers still predominantly buy homes in neighborhoods with large populations of people of color. (see Table 1) On average, 51 percent of the population in the neighborhoods where African Americans typically buy their homes consists of people of color, compared with only 22 percent of the population in neighborhoods where white homebuyers predominate. These differences hold even after taking borrowers’ and census tracts’ income levels into consideration.76 Across all borrowers’ income levels, the presence of people of color in the neighborhoods where African American borrowers are concentrated is much larger compared with the areas where their white counterparts purchase their homes. Across the United States, for example, 44 percent of the population in neighborhoods where high-income black borrowers concentrate consist of people of color, compared with 22 percent of the population in neighborhoods sought by high-income white homebuyers.

Seventy-five percent of black borrowers and 88 percent of white borrowers, respectively, buy their homes in moderate- and high-income neighborhoods. The racial composition of these neighborhoods, however, differs significantly, even after controlling for borrowers’ income. Forty-one percent of the population in moderate- and high-income neighborhoods where high-income black homebuyers purchase a home consists of people of color, compared with just 21 percent in moderate- and high-income neighborhoods where white high-income borrowers reside. Furthermore, 16 percent of the population in high-income census tracts where high-income black borrowers purchase their homes is black, compared with only 5 percent of the population in high-income census tracts attracting high-income white homebuyers. (see Figure 1)

Homes in neighborhoods where black homebuyers are concentrated are worth less

African American home mortgage borrowers continue buying homes in neighborhoods where homes have depreciated or have appreciated at a slower pace compared with those in neighborhoods where white homebuyers live.

Table 1 shows that, on average, the neighborhoods where African American borrowers bought their homes during the housing boom from 2003 to 2007 feature prices that are still lower than those before the financial crisis. In 2017, home prices in these neighborhoods were 7 percent lower than in 2006. In contrast, home prices in neighborhoods where average white homebuyers purchased their homes during the same period have recovered; they increased by 2 percent between 2006 and 2017.

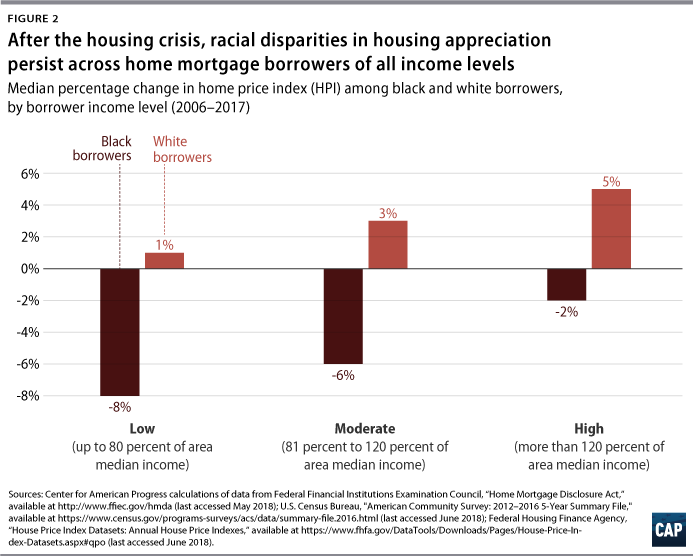

Most broadly, racial disparities in home appreciation have persisted nationally even in the aftermath of the Great Recession, despite a general increase in home prices.77 In 2017, home prices in neighborhoods where black borrowers have concentrated since 2013 were 6 percent lower than in 2006. Home prices in census tracts attracting white homeowners, in contrast, have increased by 3 percent. Figure 2 illustrates that racial disparities in housing appreciation hold even after controlling for borrowers’ income level.

Racial disparities in the largest markets where black homebuyers concentrate

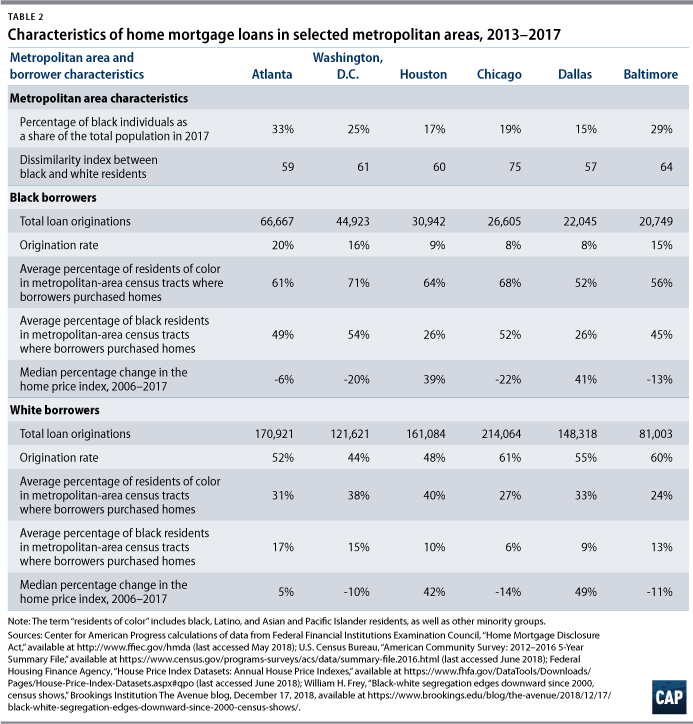

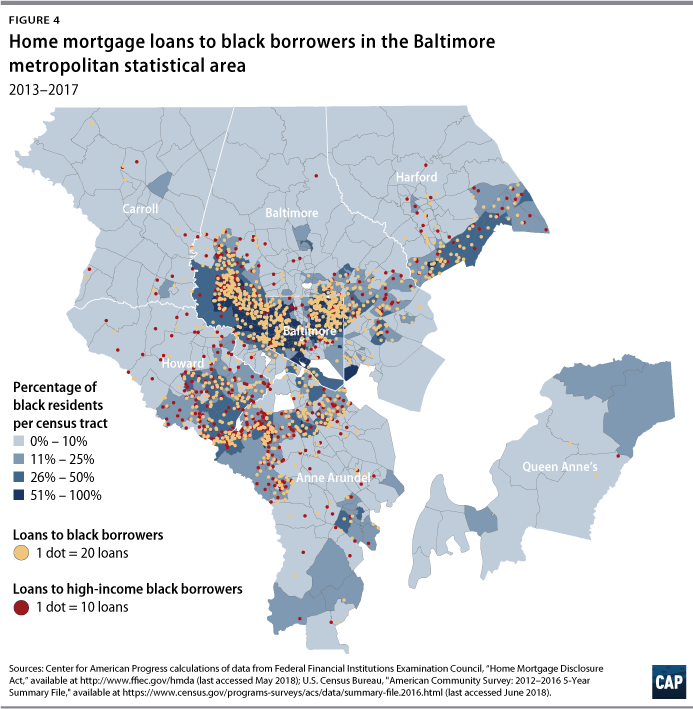

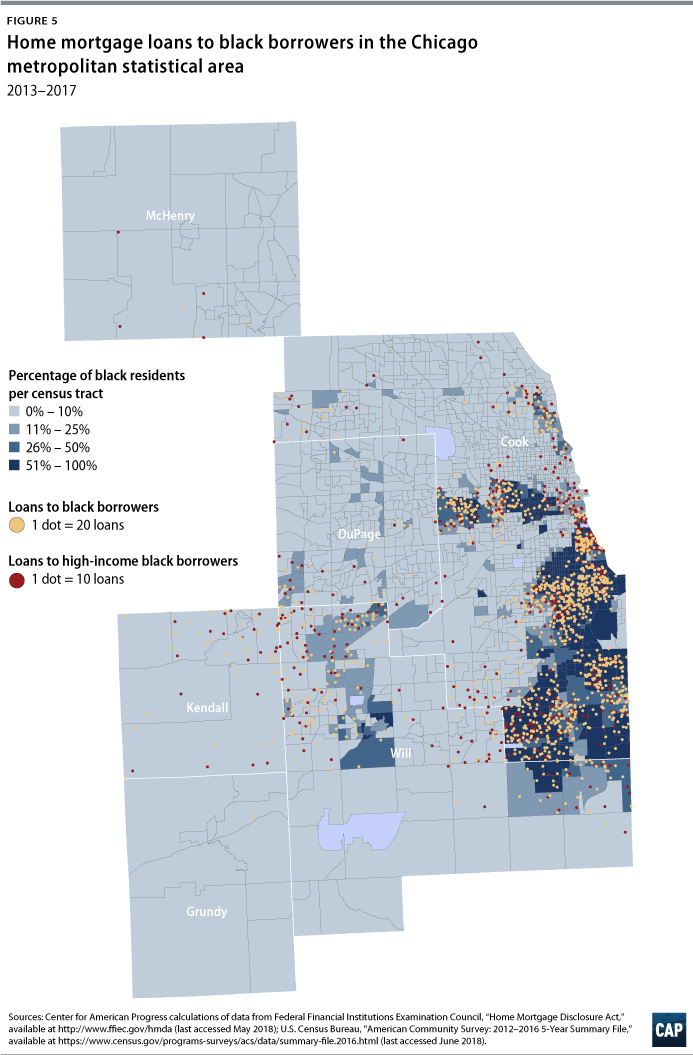

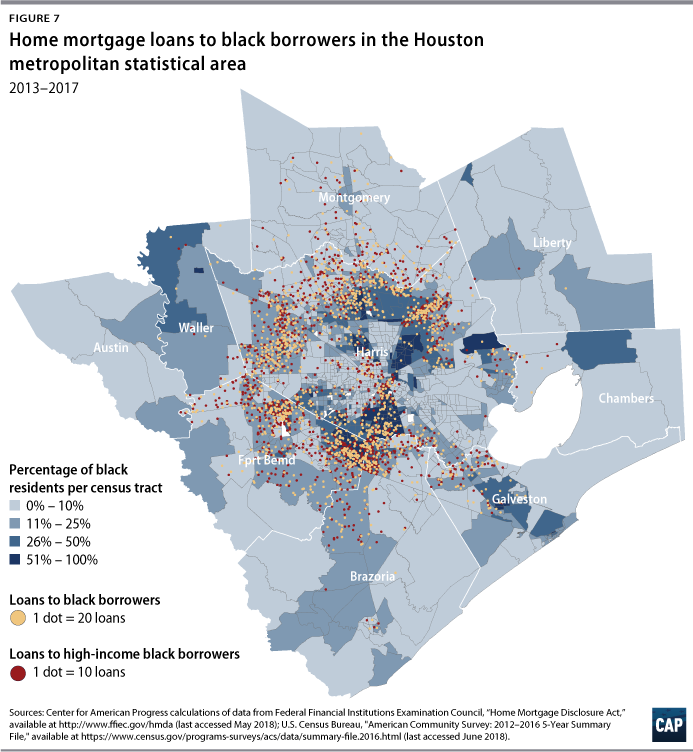

This section considers the six metropolitan areas with the largest volume of home mortgage loans to African American borrowers: Atlanta, Baltimore, Chicago, Dallas, Houston, and Washington, D.C. These areas feature a larger black population compared with the national average of 13 percent. In Atlanta, Baltimore, and Washington, D.C., African Americans represent one-third of the metropolitan area population. Despite the large presence of African Americans and the large volume of loans going to this group, black home mortgage borrowers are underrepresented in these metropolitan areas and, consistent with national trends, they obtain proportionally fewer loans than white applicants do, even when borrower’s income is accounted for.78 In Baltimore, for example, African Americans represent 29 percent of the metropolitan area population. Only 15 percent of all home mortgage loans, however, have gone to black borrowers in the years after the Great Recession, in contrast to the 60 percent of total loans that have gone to white borrowers. (see Table 2)

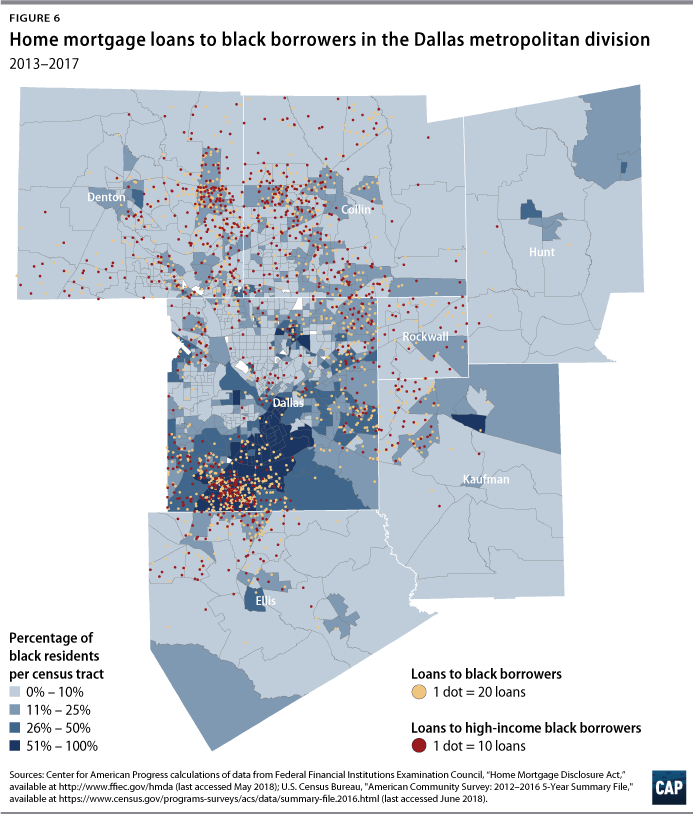

Despite a decrease in segregation levels during the past three decades,79 African Americans in these metropolitan areas are still highly segregated from non-Hispanic whites. Standard measures of residential segregation80 show that well more than half of the African American population in these metropolitan areas—from 57 percent in Dallas to 75 percent in Chicago—would have to live in a different neighborhood in their metropolitan areas in order to achieve a more dispersed geographic distribution and less separation from white residents. (see dissimilarity indexes in Table 2)

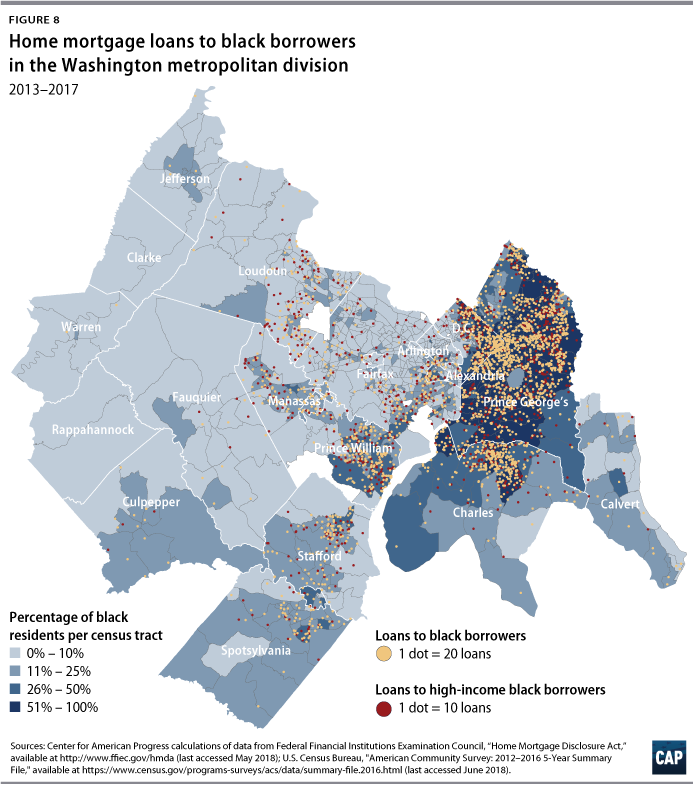

Racially segregative patterns are evident in the homebuying outcomes of African Americans and white homebuyers across the six metropolitan areas, particularly in Washington, D.C., Chicago, Atlanta, and Baltimore. Here, African Americans of all income levels purchase homes in neighborhoods where black residents make up a very large share of the total population. (see Table 2) In Washington and Chicago, for instance, African American homebuyers concentrate in neighborhoods where African American residents represent the majority of the population. In contrast, white borrowers purchase homes in neighborhoods where African Americans represent, on average, a very small share of the total population; in Chicago, this share is only 6 percent.

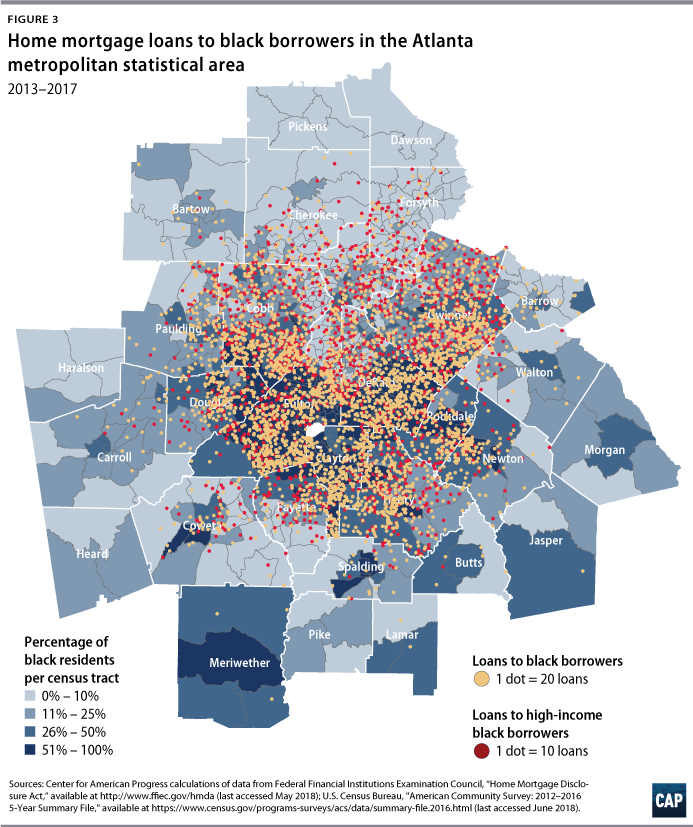

Figures 3 through 8 illustrate the distribution of black homebuyers in these six metropolitan areas in relation to the geographic distribution of the black population. As the maps indicate, the density of black homebuyers tends to be higher in census tracts where the black population is mostly concentrated compared with predominantly nonblack neighborhoods. This is particularly clear in areas such as Washington, D.C., Baltimore, and Chicago, which feature very high levels of segregation. (see Table 2) The geographic distribution of black homebuyers is more dispersed in Dallas.81 The figures also show that the distribution of high-income black homebuyers generally mirrors that of all black homebuyers across the selected metropolitan areas.

Consistent with existing research,82 a geographic information systems (GIS) analysis of trends in the home price index across census tracts in the selected metropolitan areas pinpoints a general overlap between depreciating neighborhoods and neighborhoods that are characterized by a large concentration of African Americans. 83 Echoing national trends, the six metropolitan areas feature racial disparities in home appreciation in the neighborhoods where black and white borrowers purchase their homes. (see Table 2) In general, neighborhoods where black homebuyers are concentrated have appreciated less than neighborhoods where white mortgage borrowers purchase a primary dwelling, even in areas such as Dallas and Houston, where for both racial groups, homes in 2017 were valued more than in 2006.84 In Washington and Chicago, homes in neighborhoods where black homebuyers predominantly purchase feature prices that are still 20 percent and 22 percent, respectively, below 2006 levels. In Atlanta, while home prices in neighborhoods attracting white homebuyers have experienced a 5 percent increase since 2006, home prices in census tracts where black homebuyers are concentrated are still 6 percent below 2006 levels.

It is time to strengthen fair housing enforcement

Because of the complex interrelation between persisting residential segregation and other social and economic dynamics that constrain African Americans’ economic mobility, eliminating segregation may require tools that are beyond the scope of federal fair housing policy; CAP set out a broad analysis and a number of recommendations in its 2018 report, “Systematic Inequality: How America’s Structural Racism Helped Create the Black-White Wealth Gap.”85 However, fair housing policy represents today, as it did in the past, a critical starting point for preventing and eliminating the various forms of discrimination in the housing market that perpetuate segregation and its consequences. Fair housing policy needs to be strengthened rather than rolled back, contrary to what the Trump administration has been attempting to do. Under Secretary Ben Carson, in particular, HUD has proposed to significantly scale down fair housing enforcement and integration remedies.86 Secretary Carson has attacked federal efforts toward integration as a form of “failed socialism.”87 CAP therefore recommends taking the following actions.

Make local jurisdictions once again responsible for planning to achieve fair housing

In particular, the 2015 Affirmative Furthering Fair Housing (AFFH) rule should be fully reinstated. In 2018, HUD suspended the obligation of local jurisdictions to file plans under the AFFH rule, despite evidence that the rule has been effective in propelling HUD funding recipients to meaningfully commit to fair housing.88 The implementation of the AFFH rule should be resumed and expanded, as it provides a critical tool to combat discriminatory practices and persisting residential segregation patterns while promoting more equitable investment in communities of color across the United States that continue to be devalued and feature a low housing demand.

Empower federal, state, and local governments and nonprofits to fully enforce the Fair Housing Act

More funding should be appropriated for the Fair Housing Initiatives Program (FHIP) and for staffing in HUD’s Office of Fair Housing and Equal Opportunity (FHEO). Introduced in 1987 and administered by the FHEO, the FHIP is a federal program that specifically funds public and private fair housing organizations engaged in education, outreach, preliminary fair housing investigations, and testing.89 The FHIP program is underfunded, resulting in many fair housing and fair lending violations remaining undetected, underreported, and unresolved.90 An increase in appropriations devoted to this program would enable fair housing organizations and state and local government agencies to address fair housing and fair lending violation backlogs and engage in preventative investigations. Too often, discrimination is less overt than in the past and is difficult to detect. In addition, the burden of enforcement is often put on the victims of discrimination.91

While it is important that the FHIP program supports investigations of complaints filed by potential victims, it is also critical that this program supports proactive investigations that are independent of individual complaints in order to uncover systemic discriminatory practices that are difficult for victims to detect; expand scrutiny on actors that are not well covered by existing fair housing laws; monitor discriminatory practices in communities at risk; and explore strategies that are effective in deterring discriminatory practices and reversing segregation patterns. In addition, funding for FHEO staffing should be increased in order to more adequately support the office’s ability to perform investigations and to manage the FHIP and other fair housing programs.

Catch and stop systematic discrimination, rather than perpetuating it

Specifically, it is essential that HUD firmly enforce, rather than reconsider and dilute, the Fair Housing Act’s disparate impact rule. In June 2018, HUD published a notice92 announcing its intention to reconsider the 2013 final rule implementing the Fair Housing Act’s disparate impact standard. The disparate impact standard is a very critical tool for detecting and addressing discriminatory housing practices that systematically affect communities of color but are difficult to prove. Even when there is no intention to discriminate, it is very important to hold housing agencies and players accountable for the discriminatory consequences of their actions that ultimately lead to and reinforce systemic racial disparities in the housing market.

Unfortunately, the racial disparities illustrated in this report signal that segregation in the homebuying market is still a reality, with negative implications for equity building and wealth accumulation for African American homebuyers. Further investigation is required to identify and monitor specific entities and practices that perpetuate this destructive process.

Conclusion

The analysis of home mortgage data presented in this report shows that African American homebuyers continue to be concentrated in nonwhite neighborhoods—even when they have the financial resources to afford homes in any neighborhood of their choice, where the opportunities for equity building are similar to those of white homebuyers of comparable socioeconomic status. These patterns are concerning because they reflect and contribute to persisting racial segregation in the residential landscape.

The Fair Housing Act aimed at eliminating overt discrimination and disparities in the housing market and ultimately ending residential segregation. Although the Fair Housing Act has succeeded in eliminating the most blatant forms of discrimination that were common 50 years ago, the U.S. housing market is still highly segmented along racial lines. The legacy of federal redlining and discriminatory housing policies and private practices is still visible today, as housing discrimination has taken different forms and African American neighborhoods continue to be devalued compared with white neighborhoods.

The findings presented in this report provide support for existing evidence on the persistent disenfranchisement of black homeowners in the United States. Not only are African American homebuyers still buying homes in predominantly nonwhite neighborhoods, but home prices in segregated neighborhoods where black homebuyers concentrate are also continuing a trend of slow appreciation compared with those in neighborhoods where white homebuyers purchase their homes. This has persisted even at a time when national home prices have continued recovering after the recent financial collapse. To begin to solve these issues, policymakers should seriously consider the recommendations provided in this report.

About the author

Michela Zonta is a senior policy analyst for Housing Policy at the Center for American Progress. She has extensive research, teaching, and consulting experience in housing and community development. She has published work on the government-sponsored enterprises; mortgage lending practices of ethnic-owned banks in immigrant communities; jobs-housing imbalance in minority communities; residential segregation; and poverty and housing affordability. Zonta holds a bachelor’s degree in political science from the University of Milan, as well as a master’s degree and a doctorate in urban planning, both from the University of California, Los Angeles.

Acknowledgments

The author thanks Gbenga Ajilore, Dedrick Asante-Muhammad, Debby Goldberg, Andy Green, Marc Jarsulic, Jason Richardson, Danyelle Solomon, and Christian Weller for their invaluable input.

Appendix

The statistical and GIS analyses discussed in this report were performed with the following data:

- Home mortgage data coming from the Home Mortgage Disclosure Act (HDMA) data series. Specifically, the analysis employs data coming from the 2003–2007 and 2013–2017 datasets. While the 2017 data are provided by the Consumer Financial Protection Bureau, data for prior years are available through the Federal Financial Institutions Examination Council and the National Archives. The analysis of mortgage loans focuses on two periods: the prerecession years and the postrecession years. For the prerecession years, the analysis pools HMDA data from 2003 to 2007. HMDA data from 2013 to 2017 are pooled for the analysis of mortgage lending in the postrecession period. The analysis focuses on home purchase first-lien loans for one- to four-family, owner-occupied homes. Data are for the United States, excluding Puerto Rico. HMDA data provide census tract identifiers through which it is possible to merge census tract characteristics coming from the U.S. Census Bureau and the Federal Housing Finance Agency (FHFA) to mortgage lending data.

- Annual house price index (HPI) data coming from the FHFA for census tracts from 2006 to 2017. The annual HPI represents a broad measure of single-family house price trends.

- The 2012–2016 American Community Survey, which provides detailed census-tract-level information on racial composition.93