For more than 80 years, the federal government has supported mortgage lending through a variety of policies, programs, and institutions. This support has helped enable millions of middle-class and aspiring middle-class families to buy homes.1 Despite this success, some conservatives continue to question the relevance and effectiveness of long-standing government housing policies.2

Over the past several years, conservatives who argue that some aspects of federal housing policy caused the financial crisis have pushed for legislation to eliminate or restrict government programs that make homeownership more affordable for Americans. These critics have proposed dramatically narrowing the footprint of the Federal Housing Administration, or FHA; eliminating the Community Reinvestment Act, or CRA; and scrapping the government-sponsored enterprises, or GSEs, Fannie Mae and Freddie Mac, which help provide liquidity to mortgage markets and ensure availability of the 30-year, fixed-rate mortgage.3 At the same time, some members of Congress also have supported legislation that would reopen the doors to the predatory lending and lack of oversight that caused the housing and financial crisis.4 Legislation on some of these issues can be expected in the current congressional session as part of a broad conservative attack on long-standing federal housing policies.5

These conservative arguments should be treated with skepticism. The evidence shows that the usual targets of the conservative attack did not play a significant role in the housing and financial crisis. Government policies that make it more affordable to buy a home were not responsible for the crisis. In fact, consumers who already had mortgages and who had built up equity in their homes were more likely to be targeted for predatory subprime loans than first-time homebuyers.6

Instead of too much government, it was the lack of sufficient government oversight in key areas—including consumer protection, private label mortgage securitization, bank capitalization, and financial markets—that transformed a housing bubble into a global financial crisis.

Background: Federal policies to support homeownership

The federal government enacted policies after the Great Depression that have, over the decades, helped establish homeownership as a key pillar of the American middle class. After the mortgage market froze in the 1930s and banks were unwilling or unable to continue lending, the federal government intervened to bring stability to the national housing market.7

In 1934, Congress established the FHA, which offers government insurance on mortgages. The FHA protects banks against losses on qualifying FHA-insured loans, which makes banks more willing to offer mortgages to the public, particularly during tough economic times when they might otherwise close their doors.8

The same law that established the FHA also required the creation of national mortgage associations, and in 1938, Fannie Mae was established with government backing. Fannie Mae was publicly chartered to promote the broad goals of providing greater liquidity and stability in mortgage markets. During its early years, Fannie Mae had a monopoly on the nation’s secondary mortgage market, purchasing FHA- and Veterans Administration, or VA-insured mortgages.9

After World War II, the GI Bill empowered the VA to insure mortgage loans to returning servicemen, providing government backing for millions of affordable mortgages that stimulated the country’s economic growth after the war. In the 1950s, Fannie Mae’s role expanded beyond purchasing FHA and VA mortgages into conventional loans, bringing costs down further for consumers. In the 1970s, the Federal Home Loan Mortgage Corporation, known as Freddie Mac, was created to purchase and securitize conventional mortgages.10 Freddie Mac, Fannie Mae, the FHA, and the mortgage tax deduction form the core of contemporary federal housing policy.

Government support of the mortgage market helped increase rates of homeownership significantly. Between 1940 and 1960, the nation’s homeownership rate increased from 44 percent to 62 percent—owing both to robust government support of housing markets through the FHA and the VA through the GI Bill, as well as the strong demographic, productivity, and economic growth that characterized the postwar boom.11 Since the 1960s, government policy helped maintain this higher rate of ownership, with the homeownership rate consistently remaining above 60 percent, peaking at 69 percent in 2005. It stands at 64 percent today.12 Before the creation of these federal entities, banks were unlikely to make mortgage loans unless the borrower made a very large down payment, often as high as 50 percent, and promised to repay the loan or refinance it within three to five years. When the economy crashed, banks were not willing to lend at all.13 Federal support for the mortgage market has meant that borrowers can choose from better loan products; the popular 30-year, fixed-rate mortgage, for instance, is unique globally, and it is the result of strong federal support from American mortgage markets.14 These federal mortgage entities also make sure mortgage loans are available during tough economic times when the private market shuts its doors completely to consumers.

For generations, homeownership has represented the greatest source of wealth for most U.S. households.15 Homeowners can draw on their housing wealth to invest in other activities—including supporting their children’s education, getting financing for small businesses, or handling a financial emergency. Homeownership also allows households greater financial predictability and stability and has been linked with social benefits, including higher rates of life satisfaction, political participation, and voluntarism.16

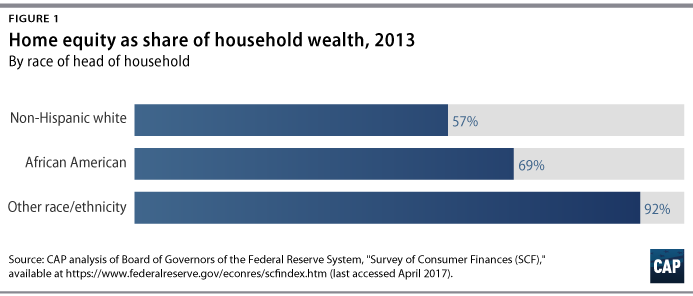

While these federal investments in homeownership have helped white families build wealth, families of color have often been excluded. The FHA, the VA, and GSEs facilitated policies such as redlining and discriminatory lending that increased segregation and prevented people of color from attaining homeownership in desirable areas.17 Research has shown that this discriminatory policy contributed significantly to modern racial household wealth gaps—and significantly undermined the economic and social mobility of African Americans and Latinos.18

This harmful set of policies began to be reversed in the 1960s and 1970s with the passage of civil rights legislation, including the establishment of the U.S. Department of Housing and Urban Development in 1965; the passage of the Fair Housing Act in 1968; the passage of the Community Reinvestment Act in 1977; and changes to the FHA’s lending practices.19 Federal policy slowly began to promote historically discriminated and underserved communities’ access to housing through securitization and insurance on mortgage loans, as well as incentives for lending that later developed into the GSE affordable housing goals in the 1990s. However, the process of correcting these errors has been slow, with significant backsliding, and much of the damage of these shameful policies persists to this day.20

Roots of the 2008 housing crisis

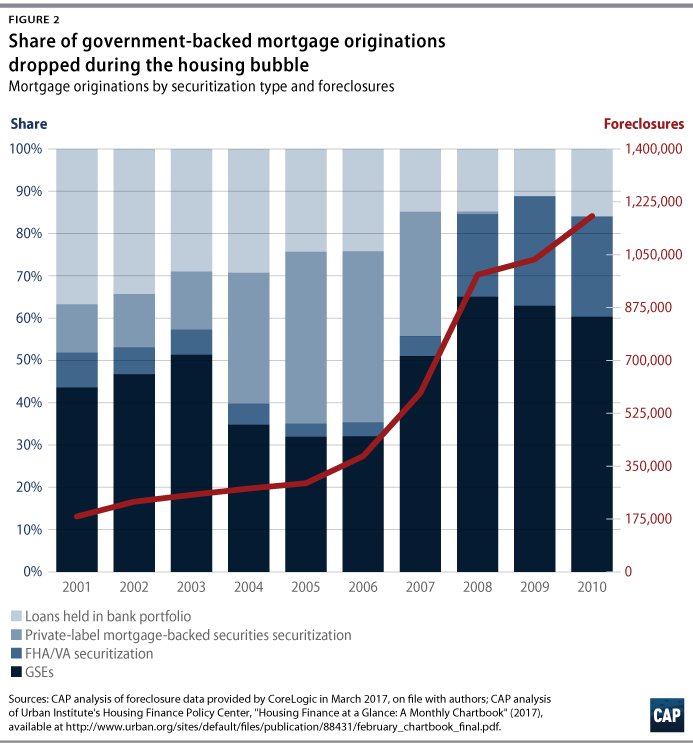

In the early 2000s, the government and GSE share of the mortgage market began to decline as the purely private securitization market, called the private label securities market, or PLS, expanded. During this period, there was a dramatic expansion of mortgage lending, a large portion of which was in subprime loans with predatory features.21 The majority of this mortgage lending was existing homeowners refinancing, with many believing that they were taking advantage of lower interest rates to extract home equity. Instead, they often were exposed to complex and risky products that quickly became unaffordable when economic conditions changed.22 Linked with the expansion of predatory lending and the growth of the PLS market was the repackaging of these risky loans into complicated products through which the same assets were sold multiple times throughout the financial system.

This spread the danger of risky mortgage loans, systematizing the housing market’s risks throughout the global financial system.23 These developments occurred in an environment characterized by minimal government oversight and regulation and depended on a perpetually low interest rate environment where housing prices continued to rise and refinancing remained a viable option to continue borrowing. When the housing market stalled and interest rates began to rise in the mid-2000s, the wheels came off, leading to the 2008 financial crisis.

There is near consensus among experts that the housing crisis was caused primarily by the rise of predatory lending and products with exotic features marketed to consumers without adequate information or preparation and sometimes using fraudulent information, as well as the failure of the PLS market.24 But some conservatives have continued to question the basic tenets of federal housing policy and have placed the blame for the crisis on government support for mortgage lending. This attack is focused on mortgage lending by the FHA, Fannie Mae and Freddie Mac’s support of mortgage markets, and the CRA’s lending incentives for underserviced communities. These claims directed at federal housing policy are at odds with the evidence.

Mortgages insured by the Federal Housing Administration did not cause the crisis

Since its creation in 1934, the FHA has provided insurance on 34 million mortgages, helping to lower down payments and establish better terms for qualified borrowers looking to purchase homes or refinance.25 When a mortgage lender is FHA-approved and the mortgage is within FHA limits, the FHA provides insurance that protects the lender in the event of default. While this role does expand access to mortgage credit, and played a key role in kick-starting the growth of American homeownership following the Great Depression, FHA-insured mortgages have never dominated the American housing market.

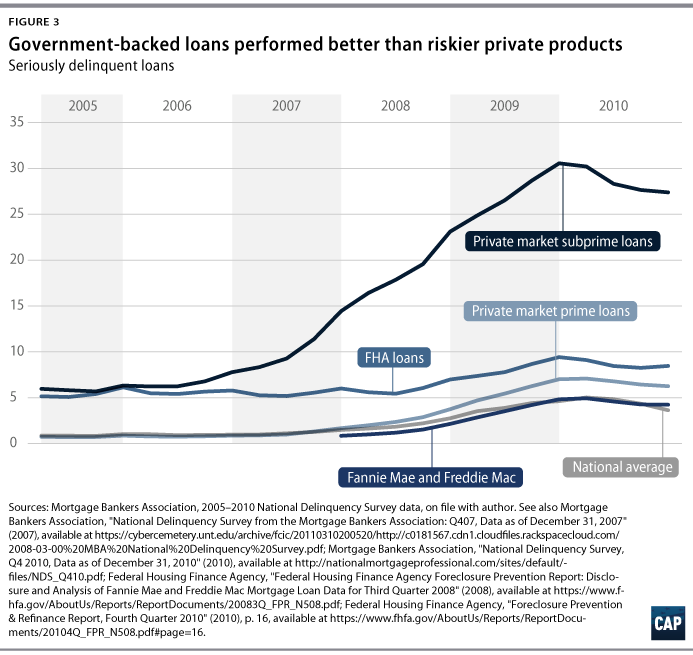

Critics have attacked the FHA for providing unsustainable and excessively cheap mortgage loans that fed into the housing bubble. In fact, far from contributing to the housing bubble, the FHA saw a significant reduction in its market share of originations in the lead-up to the housing crisis.26 This was because standard FHA loans could not compete with the lower upfront costs, looser underwriting, and reduced processing requirements of private label subprime loans.27 In many cases, brokers pushed borrowers toward higher-risk subprime products, even when they qualified for safer FHA-backed mortgages. The reduction in FHA market share was significant: In 2001, the FHA insured approximately 14 percent of home-purchase loans; by the height of the bubble in 2007, it insured only 3 percent.28 Moreover, at the height of the foreclosure crisis, serious delinquency rates on FHA loans were lower than the national average and far lower than those of private loans made to nonprime borrowers.29

Post-crisis, the FHA’s share of the market rebounded significantly, surging to a peak of 25 percent in 2011, as it filled the gap in the market left when private mortgage insurers began to fail or retreat.30 This is in keeping with the stabilizing role of the FHA in the government’s support of mortgage markets. Analysts have observed that if the FHA had not been available to fill this liquidity gap, the housing crisis would have been far worse, potentially leading to a double-dip recession.31 This intervention, which likely saved homeowners millions of dollars in home equity, was not without cost to the FHA.32 The FHA’s financial health suffered as homebuyers who purchased loans during the Great Recession began to default in larger numbers. The FHA has largely recovered from this period by modifying its loan conditions and requirements, and it is once again on strong financial footing.33 Default rates for FHA-insured loans are the lowest they have been in a decade.34

The real causes of the housing and financial crisis were predatory private mortgage lending and unregulated markets

The mortgage market changed significantly during the early 2000s with the growth of subprime mortgage credit, a significant amount of which found its way into excessively risky and predatory products. While predatory loans fed the bubble, the primary driver of this lending was demand from Wall Street investors for mortgages, regardless of their quality, which created a dangerous excess of unregulated mortgage lending.

At the time, borrowers’ protections largely consisted of traditional limited disclosure rules, which were insufficient checks on predatory broker practices and borrower illiteracy on complex mortgage products, while traditional banking regulatory agencies—such as the Federal Reserve, the Office of Thrift Supervision, and the Office of the Comptroller of the Currency—were primarily focused on structural bank safety and soundness rather than on consumer protection.35

In many of these cases, brokers offered loans with terms not suitable or appropriate for borrowers. Brokers maximized their transaction fees through the aggressive marketing of predatory loans that they often knew would fail.36

In the lead-up to the crisis, the majority of nonprime borrowers were sold hybrid adjustable-rate mortgages, or ARMs, which had low initial “teaser” rates that lasted for the first two or three years and then increased afterward.37 Many of these products were not properly explained to borrowers who were then on the hook for unaffordable mortgage obligations. Many of these mortgages were structured to require borrowers to refinance or take out another loan in the future in order to service their debt, thus trapping them.38 Without perpetual home price appreciation and low interest rates, refinancing was practically impossible for many borrowers, and a high number of these subprime mortgages were effectively guaranteed to default.39

The rise of subprime lending was fueled in large part by seemingly inexhaustible Wall Street demand for these higher yielding assets for securitizations. Especially in a long-term, low interest rate environment, these loans, with their higher rates, were in tremendous demand with investors—a demand that Wall Street was eager to meet. The private label securities market, or PLS, Wall Street’s alternative to the government-backed secondary mortgage markets, grew significantly in the lead-up to the crisis. The expansion of an unregulated PLS market and the development of the ever more complicated financial instruments tied to it are what transformed a housing bubble into the largest financial crisis since the Great Depression. PLS volumes increased from $148 billion in 1999 to $1.2 trillion by 2006, increasing the PLS market’s share of total mortgage securitizations from 18 percent to 56 percent.40

The rapid growth of the PLS market relied on brokers systematically lowering, and in many cases ignoring, their underwriting standards while also peddling ever riskier products to consumers. Parties securitizing the mortgages, private credit rating agencies, and the banks failed to closely examine or understand these products—or looked the other way as they profited from the bubble—while investment banks developed ever more complex products that traded based on the value of these mortgage-backed securities.41

The whole process was complex, interconnected, and vast—and it was all underpinned by appreciating home prices. Once prices dropped, the securities that originated with little equity, poor broker underwriting practices, and poorly regulated securitization markets were worth far less than their sticker prices.42 Derivatives and other financial instruments tied to mortgage-backed securities—often designed to help institutions hedge against risk—ended up concentrating risk once the underlying assets depreciated rapidly. Banks had significant exposure to questionable mortgage-backed securities on their balance sheets, but they set aside too little capital to absorb losses. The fact that so many financial products, banks, and other investors were exposed to the mortgage market led to rapidly declining investor confidence.43

Globally, fear spread in financial markets, causing what amounted to a run on financial institutions in the United States, Europe, and elsewhere.44 Global banks did not necessarily need to have significant positions in American mortgage markets to be exposed to the fallout.45 Given the interconnectedness of modern finance; the opacity and complexity of bank balance sheets; and financial institutions’ dependence on short-term funding, investors were not sure who was exposed to risky PLS, and financial markets around the world faced a panic.

Fannie Mae and Freddie Mac did not cause the crisis

As explained above, Fannie Mae and Freddie Mac provide liquidity to support the nation’s mortgage market by purchasing loans from lenders and packaging them into mortgage-backed securities. They then sell these securities to investors, guaranteeing the monthly payments on the securities. This system allows banks to offer affordable products to homebuyers such as the 30-year, fixed-rate mortgage: Fannie Mae and Freddie Mac purchase these loans from lenders, allowing lenders to get repaid quickly instead of waiting up to 30 years to replenish their funds. By extending their guarantee to these securities, the two GSEs enable interest rate investors to buy securities backed by home mortgages while the GSEs retain and manage their credit risk.

Critics have attacked the GSEs and blamed them for supporting dangerous lending and securitization that led to the housing crisis. In the years prior to the crisis, however, private securitizers increasingly took market share from the GSEs with the development of a massive PLS market backed by big Wall Street banks.46 Fannie Mae and Freddie Mac played less of a market role in the lead-up to the crisis than they had for most of the postwar era. Wall Street financial institutions did not abide by the same standards that Fannie Mae and Freddie Mac established, encouraging risky lending to meet investors’ appetite for PLS mortgage-backed securities; this lending fueled a significant expansion of subprime mortgage lending.

This shift led to a rapid decline in the quality of mortgage lending. A lender no longer had to make a good loan in order to sell it in the secondary mortgage market—any loan would do. The Financial Crisis Inquiry Commission found that in 2008, GSE loans had a delinquency rate of 6.2 percent, due to their traditional underwriting and qualification requirements, compared with 28.3 percent for non-GSE or private label loans, which do not have these requirements.47

Moreover, it is unlikely that the GSEs’ long-standing affordable housing goals encouraged lenders to increase subprime lending.48 Since 1992, Fannie Mae and Freddie Mac have been subject to affordable housing goals designed to help target their support of single-family and multifamily mortgages lending in order to increase homeownership in economically marginalized communities.49 The goals originated in the Housing and Community Development Act of 1992, which passed with overwhelming bipartisan support.50

Despite the fairly broad mandate of the affordable housing goals, there is little evidence that directing credit toward borrowers from underserved communities caused the housing crisis. The program did not significantly change broad patterns of mortgage lending in underserviced communities, and it functioned quite well for more than a decade before the private market began to heavily market riskier mortgage products.51

To be sure, the GSEs made costly errors that contributed to the housing bubble and ultimately landed them under government conservatorship. As Wall Street’s share of the securitization market grew in the mid-2000s, Fannie Mae and Freddie Mac’s income dropped significantly.52 Determined to keep shareholders from panicking, they filled their own investment portfolios with risky mortgage-backed securities purchased from Wall Street, which generated greater returns for their shareholders.53

In the years preceding the crisis, they also began to lower credit quality standards for the loans they purchased and guaranteed, as they tried to compete for market share with other private market participants. They guaranteed loans known as Alt-A mortgages, which defaulted at high rates.54 These loans were typically originated with large down payments but with little documentation.55 While these Alt-A mortgages represented a small share of GSE-backed mortgages—about 12 percent—they were responsible for between 40 percent and 50 percent of GSE credit losses during 2008 and 2009.56

These errors combined to drive the GSEs to near bankruptcy and landed them in conservatorship, where they remain today—nearly a decade later.57 However, they were late to the game and did not drive the predatory lending that led to the housing crisis, which was instead primarily financed by Wall Street banks and securitizers.58 And, as described above, overall, GSE backed loans performed better than non-GSE loans during the crisis.

The Community Reinvestment Act did not cause the crisis

The Community Reinvestment Act, or CRA, is designed to address the long history of discriminatory lending and encourage banks to help meet the needs of all borrowers in all segments of their communities, especially low- and moderate-income populations.59 Congress passed the CRA in 1977 to provide lending incentives to support civil rights anti-discrimination legislation and in response to local bank closures and unjustifiably low levels of lending in certain communities that shut out entire populations from the benefits of homeownership. The central idea of the CRA is to incentivize and support viable private lending to underserved communities in order to promote homeownership and other community investments. The law has been amended a number of times since its initial passage and has become a cornerstone of federal community development policy.60 The CRA has facilitated more than $1.5 trillion in private lending to underserved communities, greatly assisting the development of affordable housing for low- and moderate-income groups as well as broader community economic development.61

Conservative critics have argued that the need to meet CRA requirements pushed lenders to loosen their lending standards leading up to the housing crisis, effectively incentivizing the extension of credit to undeserved borrowers and fueling an unsustainable housing bubble.62 Yet, the evidence does not support this narrative.

From 2004 to 2007, banks covered by the CRA originated less than 36 percent of all subprime mortgages, as nonbank lenders were doing most subprime lending.63 Out of this minority share, only 10 percent of all loans made by CRA-covered banks and their affiliates to lower-income individuals even qualified for CRA lending credits.64 In total, the Financial Crisis Inquiry Commission determined that just 6 percent of high-cost loans, a proxy for subprime loans to low-income borrowers, had any connection with the CRA at all, far below a threshold that would imply significant causation in the housing crisis.65 This is because non-CRA, nonbank lenders were often the culprits in some of the most dangerous subprime lending in the lead-up to the crisis.

Loans made by CRA banking institutions were only half as likely to default compared with similar loans made in the same neighborhoods by private nonbank mortgage originators not subject to the law—400 of which went bankrupt nationwide during the housing crisis.66 This is in keeping with the act’s relatively limited scope and its core function of promoting access to credit for qualifying, traditionally underserved borrowers. Gutting or eliminating the CRA for its supposed role in the crisis would not only pursue the wrong target but also set back efforts to reduce discriminatory mortgage lending.

Defending a record of success

While nobody can argue that federal housing policy has been perfect, government support of mortgage lending and liquidity in mortgage markets has provided real benefits to consumers and the economy. Federal housing policy promoting affordability, liquidity, and access is not some ill-advised experiment but rather a response to market failures that shattered the housing market in the 1930s, and it has sustained high rates of homeownership ever since. With federal support, far greater numbers of Americans have enjoyed the benefits of homeownership than did under the free market environment before the Great Depression.

Placing blame for the housing crisis on the government is misguided and will lead to bad solutions for housing policy issues related to GSE reform, the FHA, and affordable lending legislation. Rather than focusing on the danger of government support for mortgage markets, policymakers would be better served examining what most experts have determined were causes of the crisis—predatory lending and poor regulation of the financial sector. Placing the blame on housing policy does not speak to the facts and risks turning back the clock to a time when most Americans could not even dream of owning a home.

Colin McArthur is a former Legal Fellow at the Center for American Progress. Sarah Edelman is the Director of Housing Policy at the Center.

The authors would like to thank Julia Gordon and Barry Zigas for their helpful comments. Any errors in this brief are the sole responsibility of the authors.