In 2012, more than 100,000 big U.S. businesses managed to shelter billions of dollars of income in a single tax haven and pay no corporate income tax on it.

This tax haven is not Panama, Switzerland, or the Cayman Islands. In fact, it cannot even be found on a map—rather, it exists in the pages of the U.S. tax code. These businesses—with revenue of more than $10 million each—managed to pay no U.S. corporate income tax by pretending to be small businesses and thus saved their wealthy owners billions of dollars.

Most people think of big businesses as traditional corporations, which are organized under Subchapter C of the tax code and are supposed to pay the corporate income tax on their profits. But today many big businesses are organized as partnerships or S corporations, which are business forms that were originally designed for simpler or smaller businesses. The vast majority of partnerships and S corporations do not pay the corporate income tax. Instead, all of their income is passed through to their individual owners, who pay taxes on their individual income tax returns, thus avoiding the corporate income tax altogether.

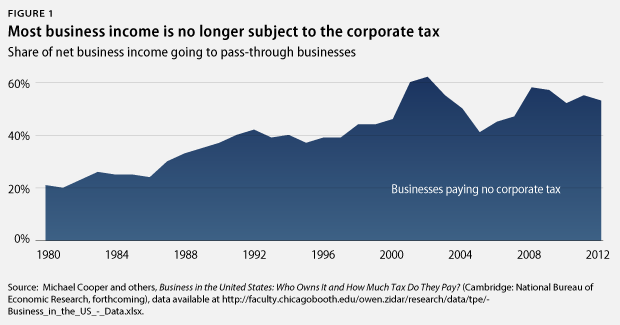

The share of income going to businesses that use the pass-through form of organization—and therefore pay no corporate income tax—has exploded over the last 30 years, growing from less than 25 percent of net business income in 1980 to more than half in 2012. In fact, the United States is unique in this regard: No other country comes close to having such a large portion of business income that is not subject to the corporate income tax.

A recent groundbreaking study by economists at the U.S. Treasury Department, the University of Chicago, and University of California, Berkeley, reveals serious effects of the rise of pass-throughs on tax revenue and inequality. In principle, income from pass-through businesses could be taxed at the same rate as income from C corporations. But it is not—when one combines the corporate income tax and taxes on dividends, income from C corporations in 2011 was taxed at an effective rate of 32 percent, while income of the three general types of passthrough businesses was taxed between 14 percent and 25 percent.

The study—which was based on detailed review of administrative tax data— implies that the growth of these lightly taxed pass-through businesses cost the federal government $100 billion in 2011. The long-term budget impact of this revenue loss is enormous: The $100 billion revenue loss in 2011 implies as much as $790 billion in lost tax revenue from 2003 to 2012, based on nominal business income growth during that period. That is $790 billion that could have been spent repairing schools, cutting taxes for everyday Americans, or reducing the national debt. It is more than the $700 billion Congress allocated to bail out the financial industry in 2008 as part of the Troubled Asset Relief Program, or TARP.

What the big pass-through tax loophole and TARP have in common is that both heavily benefit the financial industry: 70 percent of partnership income—the primary business form that big businesses use to avoid corporate taxes—goes to the financial industry and holding companies.

The major differences between the big pass-through loophole and TARP, however, are that TARP ended up only costing $28 billion and helped prevent the next Great Depression. The tax revenue lost from hedge funds, private equity firms, other financial firms, and holding companies pretending to be small businesses, on the other hand, is gone forever from federal revenues and only benefitted the mostly wealthy owners of private businesses.

The lower tax rates on income from pass-throughs are often defended based on the assumptions that all small businesses are pass-throughs and that all passthroughs are small businesses. Both assumptions are wrong. In fact, the growing number of pass-through entities has very little to do with small business. Indeed, several of the largest U.S. hedge funds are taxed as partnerships. In part because increasing numbers of businesses are adopting pass-through forms, the corporate income tax today contributes only about one-tenth of total tax revenues compared to one-third 60 years ago.

The ability of big businesses to avoid paying the corporate income tax through organizing as pass-through entities represents an enormous loophole in the country’s business taxation regime that the original designers of the corporate income tax probably never foresaw. Three facts underscore just how thoroughly big business, the financial industry, and the wealthy have exploited tax rules that were originally designed for smaller, simpler businesses:

- Seventy percent of partnership and S corporation revenue goes to big businesses.

- Seventy percent of partnership income comes from the financial industry and holding companies.

- Seventy percent of partnership and S corporation income goes to the top 1 percent of U.S. households by income.

Until recently most analyses of income inequality, such as that by Thomas Piketty in Capital in the 21st Century, have ignored the role of pass-through income in the U.S. tax system by allocating it according to a standard economic formula. But, as this report will highlight, it is impossible to understand the growth of income inequality without a deeper look at pass-through income: about 40 percent of the increased share of income going to the top 1 percent of households is explained by pass-through income—twice the contribution of other forms of capital, such as corporate stocks and bonds.

Policymakers and the media have shined a bright light on how U.S. multinational corporations’ use of foreign tax havens has caused corporate tax revenue to decline. Yet the problem of the growing number of large U.S. businesses that are not required to pay the corporate income tax at all has received far less attention. The U.S. Congressional Budget Office, or CBO, recently estimated that about half of the projected decline in corporate income tax revenue in recent years is a result of C corporations transforming to pass-through entities and thereby no longer paying any corporate income tax at all.

This report explains the reasons for the rise of pass-through businesses, especially partnerships, showing how this form of business organization facilitates tax avoidance and opaque business practices. It also highlights new data, referenced above, showing the role of pass-throughs in the growth of income inequality and the likely cost to American taxpayers. Finally, the report identifies options to address these concerns as part of corporate tax reform and highlights three actions policymakers can take to prevent big business from hiding in the pass-through tax haven.

- Make large pass-through entities pay an entity-level tax like C corporations do. This could take many forms including taxing the relatively small number of pass-through firms that meet certain size thresholds based on level of profits, gross receipts, or assets. This would target less than 2 percent of pass-through firms—but a large share of pass-through income—while not affecting truly small and moderate-sized businesses.

-

Make sure wealthy taxpayers pay their fair share of tax on pass-through income at the individual level. This income should be subject either to employment taxes or the net investment income tax, whichever is appropriate, but should not escape both.

-

Help truly small businesses. If business tax breaks are eliminated as part of a future corporate tax reform effort, more targeted relief could be provided to actual small businesses which would not benefit from a reduction in the corporate tax rate.

Policymakers must enact reforms to curb the extent to which very large companies can use pass-through forms of organization. Businesses should be able to organize however they want in order to run their operations as efficiently as possible. But the arguments in favor of pass-through taxation for some types of businesses, especially partnerships, become very weak when these entities are huge businesses that use this organizational form to avoid paying billions of dollars in taxes—businesses that would be taxed as corporations if not for the big pass-through loophole.

Alexandra Thornton is the Senior Director of Tax Policy on the Economic Policy team at the Center for American Progress. Brendan V. Duke is the Associate Director for Economic Policy at the Center for American Progress.